Global| May 18 2015

Global| May 18 2015Japan's IP Deflates on Revision

Summary

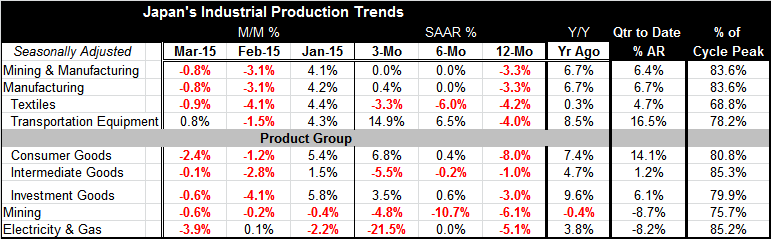

Japan's industrial production had a very good start to the quarter; since then it has been all downhill. After rising by 4.1% in January, IP fell by 3.1% in February and fell by 0.8% in March. Still, because of the jackrabbit start of [...]

Japan's industrial production had a very good start to the quarter; since then it has been all downhill.

Japan's industrial production had a very good start to the quarter; since then it has been all downhill.

After rising by 4.1% in January, IP fell by 3.1% in February and fell by 0.8% in March. Still, because of the jackrabbit start of IP at the outset of the quarter, output will grow at a 6.4% annual rate in Q1. Yet, that is a distortion of performance since output in March is already 1.6% below the Q1 average. This is clearly setting up Q2 for some real weakness, not for strength.

Output of all the major categories is lower in most for two months running. Only the manufacturing sector, transportation equipment has an increase of 0.8% in March after a 1.5% decline in February. The same is true for monthly output at the product level. Of the five groups in the table, there are two month declines in each sector except for electricity and gas; that sector posted a 3.9% drop in March with a thin 0.1% increase in February.

Because of strength in most categories in January, the three-month changes in output are still showing growth in some sectors. Overall mining and manufacturing output is flat over three months; for manufacturing it is up by 0.4%. Textiles output is falling at a 3.3% annual rate over three months, but transportation equipment output is up at a roaring 14.9% annual rate.

The monthly pattern of output makes some of the usual calculations of sequential growth rates a less meaningful way to pin down trends. As we showed, for mining and manufacturing, overall output is lower in March than its Q1 average, yet the sequential growth rates show growth stabilizing with zero growth over three months and six months compared with IP lower by 3.3% year-over-year. Sequential growth rates by sector show a number of sectors where output appears to be gaining momentum but where the intra-quarterly patterns shows the reverse result.

Japan clearly continues to be in a difficult period. The consumption tax hike once again was implemented too soon and it has cost the economy all the momentum it had built up. Just today Japan's tertiary sector (services sector) reading for March saw an unusual drop, its first in 11 months. Industrial output shows a lot of variability and not much trend. Only the year-over-year pattern for IP shows a clear trend and that one is still eroding. We have seen recent weakness in Japan's consumer confidence and retail spending. The Industrial output report shows yet another aspect of Japan's economy that is struggling to post growth against a trend of declines.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief