Global| Dec 28 2020

Global| Dec 28 2020Japan's IP Bounces Back...So Does the Virus

Summary

Japan's industrial production index gained 0.2% in November as the manufacturing gauge of IP was flat. Still, these results follow five strong months of output gains in mining and manufacturing. The graph shows that year-on-year [...]

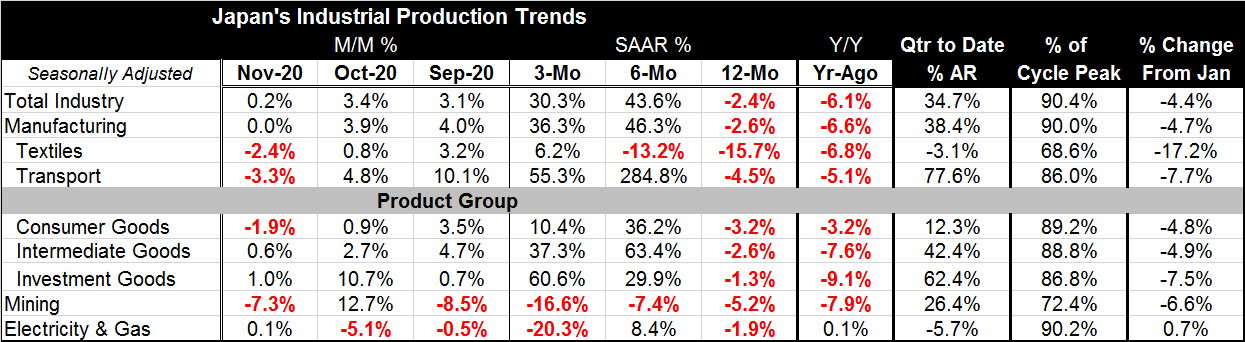

Japan's industrial production index gained 0.2% in November as the manufacturing gauge of IP was flat. Still, these results follow five strong months of output gains in mining and manufacturing.

Japan's industrial production index gained 0.2% in November as the manufacturing gauge of IP was flat. Still, these results follow five strong months of output gains in mining and manufacturing.

The graph shows that year-on-year changes in Japan IP have been declining since early-2019. Covid-19 has not been the only problem stalking Japan's economy. Manufacturing and total industry output trends show a 12-month decline in IP contrasted with a 40%-plus annualized gain over six months followed by a lesser 30%-plus annualized gain over three months – strong figures all...

This is a common pattern internationally. Covid-19 struck early in the year dragging things down then; there was recovery that was extremely rapid but incomplete and short lived. And as 2020 draws to a close, growth is losing most of its momentum leaving the next step unclear for many economics as the virus has welled up again.

Japan's quarter-to-date growth in Q4 is still impressive at a 34.7% annualized rate in Q4. But that clearly is built on past strength rather than on current developments as the November data are quite modest.

Although the year-on-year data show a nice recovery in progress, total industry output is at a ratio to January's level that is weaker by 4.4%. Manufacturing also is weaker by 4.7%. And both textiles and transportation industries have been hit harder than manufacturing overall.

By sector, consumer goods and intermediate goods follow the familiar patterns. But investment goods output is still building momentum over three months as its growth rate rises from an annual rate of 29.9% over six months to 60.6% over three months.

Mining takes its queue from oil and shows ongoing progressive weakness with output falling at a 16.6% annual rate over three months. Utilities output has an erratic patterns, but it is also falling and at a rapid 20.3% annualized rate over three months.

All industry or product growth measures are lower compared to their January level except electric and gas utilities.

Japan's virus situation continues to worsen. Daily new cases are making new highs at the end of December and Japan's deaths curve also has been rising and is hitting repeated new highs.

The virus is making the end of year miserable in a lot of places. The U.S. numbers are still high as the year ends, but there are hints of an easing. Europe is just starting its program of vaccinations as a new strain of the virus is loose there. It's a fitting way to end the year: here comes the good news-oops, more bad news first!

It seems that 2020 is not through with us yet. We all are eager for a new year and new challenges. But the coronavirus has a new variant in Europe. While the vaccines have begun distribution there, the virus continues to spread like wildfire. And while everyone is playing it down, we simply do not know much about this new strain. So 2020 is ending with some of the same threat that it brought us early in the year. This time, however, we are ahead of the game, experienced and armed with vaccines. Here's hoping for a better 2021 – everywhere and in every way. Actually as wishes go, it may seem daunting, but it's a low hurdle.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief