Global| Sep 15 2006

Global| Sep 15 2006Japan's Flow-of-Funds Data for Q2 Add to Questions about Economic Progress

Summary

Earlier this week, Louise Curley highlighted the fragility of recent gains in the Japanese economy. She described new weakness in manufacturing orders and some deterioration in consumer confidence. Today, data on flow of funds in the [...]

Earlier this week, Louise Curley highlighted the fragility of recent gains in the Japanese economy. She described new weakness in manufacturing orders and some deterioration in consumer confidence. Today, data on flow of funds in the financial system for Q2 2006 add more to the ambiguity about the outlook. For instance, the move by the Bank of Japan away from its zero-interest-rate monetary policy in mid-July was based partly on renewed growth in bank lending. This continues, but other liabilities in the domestic economy have started to weaken again.

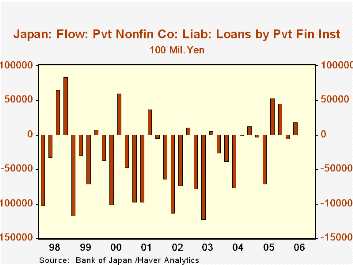

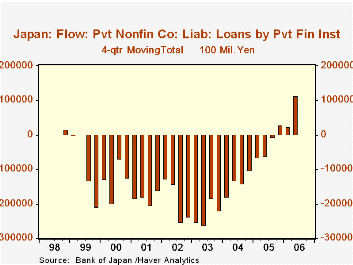

The Japanese flow of funds data are not seasonally adjusted, and Q2 is a generally a period of contraction in credit as an old fiscal year has just been closed out and a new one begun. So negative reports for this period are unremarkable in and of themselves. In fact, a striking aspect of these new flow-of-funds data is a quarterly increase in lending to private corporations; at +¥1.89 trillion, it's not large, but it's the first Q2 increase in the nine years history of this style of Flow of Funds accounts. Q3 and Q4 often see sizable increases in credit transactions. So a 4-quarter total might give us a good idea of the overall strength of lending; indeed, there has been a dramatic upturn in financial institution lending to business on this basis, which reached +¥11.35 trillion through Q2, compared to a contraction of ¥6.02 trillion in Q2 2005 and progressively larger declines going back to early 2003.

But other private-sector uses of credit remain sluggish or erratic. Total liabilities of the domestic nonfinancial sector excluding government fell ¥32.52 trillion in Q2, yielding a 4-quarter total of -¥35.82 trillion -- that is, net paydowns -- actually much worse than the -¥5.97 trillion of a year ago. Even total private corporation borrowing was weaker in Q2 2006, -¥21.81 trillion, than in Q2 2005, -¥18.05 trillion, although the 4-quarter total was positive.

Households have the same pattern, a drop in Q2 2006 that is larger than Q2 2005, but an outright increase in the more recent 4-quarter total contrasting with the liquidation in the year-ago period.

So credit data, as well as real-sector business and consumer indicators, suggest that the economic gains we were all so pleased about earlier this year in Japan are hardly on sure footing.

| Japan: Flow of Funds, Tril.¥ | 2Q 2006 | 1Q 2006 | 2Q 2005 | 2005 | 2004 | 2003 |

|---|---|---|---|---|---|---|

| Total Liabilities, Domestic Nonfin Sector ex Govt | -32.52 | +37.12 | -25.57 | -- | -- | -- |

| 4-Qtr Total | -35.82 | -28.87 | -5.97 | +46.83 | +53.10 | +25.59 |

| Private Nonfin Corporations | -21.81 | -1.17 | -18.05 | -- | -- | -- |

| 4-Qtr Total | +7.37 | +11.14 | -6.07 | +6.17 | +2.04 | -23.14 |

| Loans | +1.89 | -0.48 | -7.00 | -- | -- | -- |

| 4-Qtr Total | +11.35 | +2.45 | -6.02 | +2.70 | -10.14 | -21.84 |

| Households | -11.43 | +7.45 | -7.56 | -- | -- | -- |

| 4-Qtr Total | +4.09 | +7.96 | -1.30 | +4.74 | -4.36 | -1.24 |

Carol Stone, CBE

AuthorMore in Author Profile »Carol Stone, CBE came to Haver Analytics in 2003 following more than 35 years as a financial market economist at major Wall Street financial institutions, most especially Merrill Lynch and Nomura Securities. She had broad experience in analysis and forecasting of flow-of-funds accounts, the federal budget and Federal Reserve operations. At Nomura Securities, among other duties, she developed various indicator forecasting tools and edited a daily global publication produced in London and New York for readers in Tokyo. At Haver Analytics, Carol was a member of the Research Department, aiding database managers with research and documentation efforts, as well as posting commentary on select economic reports. In addition, she conducted Ways-of-the-World, a blog on economic issues for an Episcopal-Church-affiliated website, The Geranium Farm. During her career, Carol served as an officer of the Money Marketeers and the Downtown Economists Club. She had a PhD from NYU's Stern School of Business. She lived in Brooklyn, New York, and had a weekend home on Long Island.

More Economy in Brief