Global| Sep 09 2019

Global| Sep 09 2019Japan's Economy Watchers' Assessment Has Collapsed

Summary

Japan has many surveys and economic indicators. It can be useful to look at the economy from many different angles and to get some reports that are very topical but not so detailed and others that are very detailed but not so topical. [...]

Japan has many surveys and economic indicators. It can be useful to look at the economy from many different angles and to get some reports that are very topical but not so detailed and others that are very detailed but not so topical. But there are risks inherent in such a process. It will also produce reports that are inconsistent with each other and create more work for analysts trying to figure out which report is wheat and which is chaff. Welcome to what wacky word of empirical economics where statistics are everything but judgment is vital.

Japan has many surveys and economic indicators. It can be useful to look at the economy from many different angles and to get some reports that are very topical but not so detailed and others that are very detailed but not so topical. But there are risks inherent in such a process. It will also produce reports that are inconsistent with each other and create more work for analysts trying to figure out which report is wheat and which is chaff. Welcome to what wacky word of empirical economics where statistics are everything but judgment is vital.

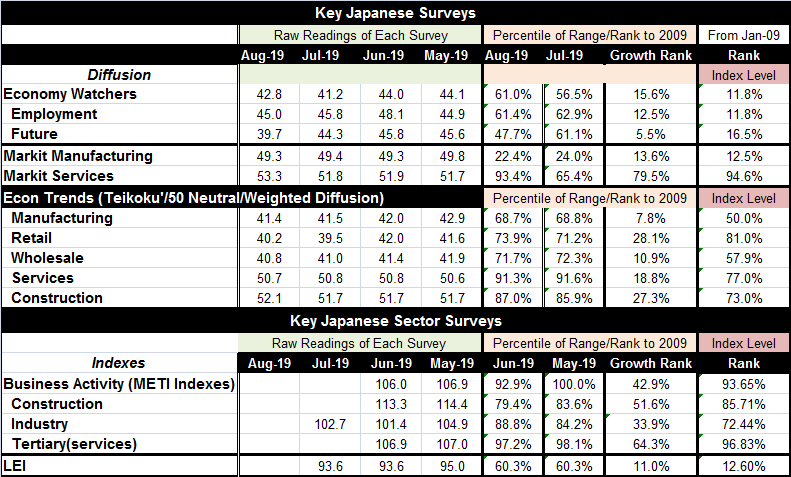

And so it is this month. While Japan's economy watchers index has fallen for three months in a row and this month has brought an increase it is still true that the index points to a sharp weakening in the economy. The future index from this survey is lower in six of the past seven months. When the level readings of this diffusion index are ranked on a period from January 2009, the headline ranks in its 11.8 percentile, the employment gauge ranks in its 11.8 percentile and the future index ranks in its 16.5 percentile. These are extremely weak readings and consistent with one another.

In diffusion terms, the three sector readings each are below 50; therefore, already pointing to contraction. But the ranking statistics tell how weak these readings really are in comparison with past tendencies.

A second set of rankings in the table assesses the diffusion metrics based on their year-over-year percentage changes. Ranked that way, the three indexes present nearly the same picture. The economy watchers index has a 15.6 percentile standing, employment has a 12.5 percentile standing and the future index has a very low 5.5 percentile standing. On balance, the levels of activity are low and momentum is very poor. That is a truly a bad combination of events, especially for an economy already running negative interest rates.

A second set of diffusion surveys from Teikoku also are available with sector detailing. These metrics show index level standings for manufacturing, retailing, wholesaling, services, and construction. The Teikoku sector indexes have queue rankings as low as 50% (for manufacturing) and rankings as high as 77% (for services). They are certainly not as weak as the economy watchers survey and therefore raise questions about the true state of the economy. And both the economy watchers and Teikoku surveys are evaluated on common ground from the current August observations back to January 2009. However, when the Teikoku data are ranked on their year-over-year growth rates, they suddenly get quite a bit weaker with no ranking as high as its 30% percentile and with two sectors (manufacturing and wholesaling) below their 11th percentile. Both the Teikoku and the economy watchers index, therefore, agree that momentum is quite poor although they disagree on the current state of the economy.

The last survey that is up-to-date through August is from IHS Markit. Markit data I have only back to January 2015 so they are not directly comparable in terms the rankings. Still, the Markit data give a mixed view on index levels ranking manufacturing as weaker only 12.5% of the time and services as weaker 94.6% of the time- a very strong service sector reading for Japan- at least when compared to the last 4.75 years. Momentum on those two sector grades out about the same with a 13.6 percentile standing for manufacturing and a somewhat less buoyant (but still quite firm) 79.5 percentile standing for services.

The consistency here is that all three of these surveys see some weak momentum. The economy watchers index sees weakness too and expected weakness without sector reference. Teikoku agrees with Markit on the service sector firmness/strength (although Markit is even stronger) and Teikoku has services momentum much weaker than Markit.

Last I present the METI sector indexes. As a set, they are up to date through June. Nearly all the other indexes mentioned above are weaker or much weaker in August than they were in June, making June a clearly behind-the-times reading. The METI industry gauge is available through July; despite rampant weakness in the other gauges, it managed to increase from its June level. That is simply odd.

We can perform the same ranking calculations on the LEI (leading economic index). Doing that gives us an LEI level ranking in its bottom 12% with momentum in its bottom 11 percentile. The LEI agrees with the economy watchers survey.

Do sector surveys speak with forked tongue or tell the truth?

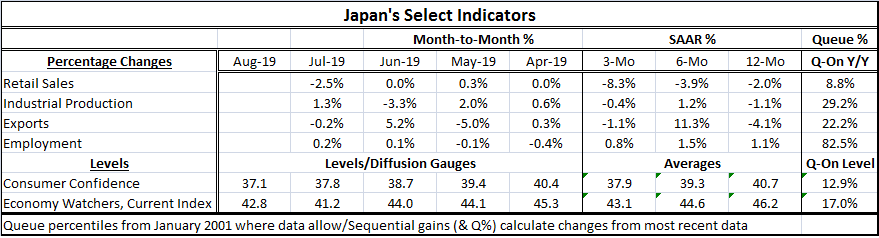

The table below presents rankings of some well-known traditional indicators in a slightly broader timeline (the economy watchers index is included in this longer time line as a control). The queue (or rank) standings applied to growth rates in the table are actually close to the economy watchers results. Employment has a relatively higher standing, but then that is normal since employment is a current to lagging variable. Retail sales, industrial production and exports have year-over-year growth rates that all rank in the lower one-quarter of their respective historic ranges. On balance, the METI indexes seem out of touch with reality. And Japan's economy looks like it might be headed for trouble. And even though a lot is being blamed on the global trade war, exports are not the weakest metric here. That dubious distinction goes to retail sales.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief