Global| Feb 09 2017

Global| Feb 09 2017Japan's Core Orders Surge As Total Orders Dive

Summary

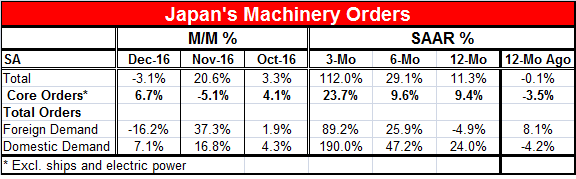

Japan's machinery orders fell by 3.1% in December while core orders rose by 6.7%. November has the growth rate 'signs' reversed with total orders up by 20.6% and core orders down by 5.1%. The monthly series is volatile. However, from [...]

Japan's machinery orders fell by 3.1% in December while core orders rose by 6.7%. November has the growth rate 'signs' reversed with total orders up by 20.6% and core orders down by 5.1%. The monthly series is volatile. However, from three-month to six-month to 12-month, both overall and core orders are accelerating.

Japan's machinery orders fell by 3.1% in December while core orders rose by 6.7%. November has the growth rate 'signs' reversed with total orders up by 20.6% and core orders down by 5.1%. The monthly series is volatile. However, from three-month to six-month to 12-month, both overall and core orders are accelerating.

In addition, total orders are accelerating on the same timeline for both foreign-sourced orders and for domestic orders. Both series - in fact all series in the table- show substantial strength over the last three months.

However, all series are volatile. The chart shows the growth rate of core orders year-over-year. Core orders have a standard deviation in their year-over-year growth rate since 2011 of 8.9%. On that same timeline, the standard deviation for foreign orders is 27% and for domestic orders it is 11.4%. Over 12 months, domestic orders are up at a pace that is twice its standard deviation and so those orders are likely really rising and not simply volatile. Foreign orders, down by 4.9%; they post too small a change to have any confidence in them given their huge 27% standard deviation. Core orders have risen over 12 months slightly greater than their standard deviation while total orders are up by a few percentage points less than their standard deviation. Despite what are large growth rates, neither of them dependably tells us anything.

The only news on the month that really has any signaling value is the increase in total domestic orders. But that is good news for the Japanese economy where we would like to see it. Global conditions remain touch-and-go and the economic situation in China, Japan's largest trading partner, is also somewhat at loose ends. Although growth is reported officially by China to be stable after having slowed, many believe it to be still cooling down.

Other Japanese reports such as its Markit manufacturing PMI show manufacturing is picking up through December. The METI Industrial index (plotted in the chart) is rising and shows reasonably strong growth. In the Teikoku survey, the services industries are expanding and even construction is advancing. All of these activities should support some orders growth. Japan's LEI was up strongly in December to its highest value since June 2015.

Japan seems to have growth in place in general, but it still does not show much sign of acceleration. The order data are too volatile to be of much use on their own. But in combination with other reports, there seems to be a story of ongoing economic advance.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief