Global| May 22 2017

Global| May 22 2017Japan Nurtures Small Trade Surplus: What's Next?

Summary

Japan's trade surplus backtracked slightly in April and did not expand as expected. While the pattern of surpluses has hinted of a trade turnaround, it now appears that Japan has had a period of an expanding surplus and no longer [...]

Japan's trade surplus backtracked slightly in April and did not expand as expected. While the pattern of surpluses has hinted of a trade turnaround, it now appears that Japan has had a period of an expanding surplus and no longer demonstrates that pattern. Of course, the bulge in February is still a difficult event to factor in and to amortize in order to reveal the true trend.

Japan's trade surplus backtracked slightly in April and did not expand as expected. While the pattern of surpluses has hinted of a trade turnaround, it now appears that Japan has had a period of an expanding surplus and no longer demonstrates that pattern. Of course, the bulge in February is still a difficult event to factor in and to amortize in order to reveal the true trend.

Driving Japan's trade imbalance

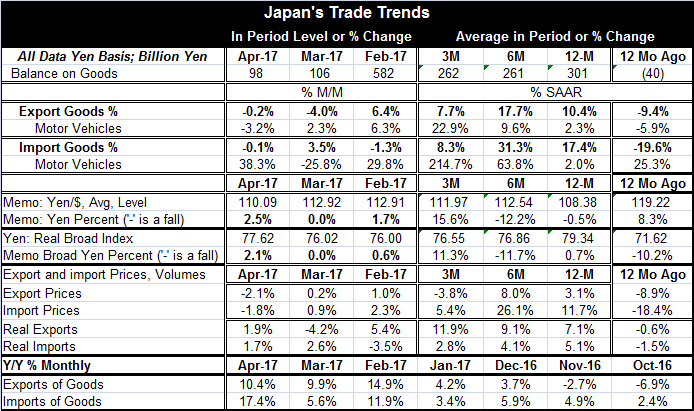

In trying to understand Japan's surplus issue, let's divide into the four pieces that rightfully drive it. First and foremost, the deficit is not an organic thing. It is the legacy of export and import trends. Exports and imports each have two important components: one is price and the other volume. We will understand where Japan's deficit or surplus is headed by understanding the interplay beyond nominal exports and imports which we can best understand by looking at the underlying price and volume trends for exports and imports separately and then as a comparative interaction.

The chart above shows nominal export and import trends seem to be spelling the end of the move to surplus as import growth has recently moved up to exceed export growth. But is that a trend that will last? To answer that, let's look at export and import price and volume trends as well as the determinants of those trends.

Export and import dynamics

The sequential growth rates show that from 12-month to six-month to three-month, import prices are growing faster than export prices. That is going to make nominal import inflation faster than export inflation- all other things equal- and that will mean import values will growth faster than export values and erode the move toward surplus. But all other things are never equal are they? In the first place, the yen's value affects export and import price developments. A stronger yen will tend to depress both export and import prices in yen terms. A stronger yen will cause Japan's exporters to have to reduce yen prices as a stronger yen will ratchet up foreign currency prices to Japan's overseas buyers. A stronger yen will also reduce import prices as yen purchasing power rises. However, the effect on the volume of trade would see a stronger yen resulting in less export growth due to the competitiveness effect and more import growth for the same reason, although it would take longer for that aspect to play out. So the direction of the yen will impact yen-based export and yen-based import prices as well as trade values. And because of differing price and volume effects, an exchange rate move may push the deficit in one direction in the short run before moving it in the other in the long run.

Exchange rates vs. growth

There is some controversy about where the yen is headed next, but over the last year and the last three months the real trade weighted yen has fallen while the bilateral exchange rate with the dollar has seen the yen slightly weaker over the past year. Since Japan trades even more with China than with the U.S., the dollar-yen-yuan exchange rate configuration can create a lot of issues and complications in markets and for policymakers. Apart from price movements related to exchange rates or inflation, it is the impact of domestic growth on imports and of foreign growth on exports that really sets the tone for trade flows. So when assessing the direction of the trade balance, there are a lot of factors to weigh and balance. And because price effects show up first and the volume effects show up later, changes induced by prices need to be carefully disentangled from apparent trends.

Export and import prices

Actual export and import price trends show that both Japan's export and import prices are up over 12 months with imports up by much more. Over three months, import prices are lower and export prices are higher. Obviously, something other than exchange rates is moving prices. The biggest factor, of course, is oil; Japan is importing oil. Oil throws a new dimension into all these calculations since it is priced in dollars. With the yen rising, there should be extra pressure apart from domestic cost pressures to push export and import prices lower. However, export prices are up but only by 3.1% over 12 months and import prices are up by 11.7% as oil prices have surged. Exchange rate effects are swimming against the tide of rising oil prices. There is some addition room for export/import price disparity here since the yen is also net lower over six months, implying that there are exchange rate cross currents flowing through the price channels in addition to any lagged effects; the impact on prices from the exchange rate is not instantaneous; thus, making it hard to isolate them when exchange rates are not moving in a straight line.

Export and import volumes

When we use export and import prices to deflate export- and import-value, we derive export and import volumes. Doing this, we find that real exports now are consistently growing faster than real imports in Japan. This is what we expect when import prices rise fast since that makes imports less competitive with domestic goods. Over the last year, the trade-weighted impact from the real broad yen was small as it rose by only 0.7% over 12 months. Over the same period, the nominal yen fell slightly vs. the dollar. Exchange rates have not been a dominant force. Over this period oil prices had the most to do with pricing differences between exports and imports as oil prices surged. As a result of this, real export trends are gaining momentum while real import trends are losing momentum. Over time, we expect that that volume effects, stemming from price changes, will exceed the price effects. That means that if import prices rise in the short run, that might make the trade deficit larger, but in the long run, we expect the volume of trade to react by even more and for the volume of imports to fall by more than prices rose. Most studies show that export and import price elasticities are greater than unity for export and import volumes. That is the condition that is required for volumes to dominate price trends in the long run. Elasticities measure the percentage change in volumes relative to the percentage change in price. If price elasticities are larger than unity (in absolute value), then price changes cause volume changes that are larger than the initial price changes. The timing asymmetry will push the trade balance in the wrong direction before pushing it in the right direction when price changes are at work in the trade account. That just adds to the complication of untangling shifting deficit trends.

Oil prices

Even as oil prices have risen, Japan has seen real import growth rise more than real exports for about two years. But conservation effects spurred by higher prices are not instantaneous and can be quite different depending on the product whose price is being affected. At last, there has been a shift and strength has passed onto real exports as imports have become expensive and less competitive. While the nominal trade balance seems to have shifted from a situation of showing rising surpluses to one in which surpluses have flattened, that does not reveal the correct fundamentals for Japan's trade. Fundamentally, Japan's export volumes are building momentum while import volumes are more moderate. And these trends have been masked by short-term price trends as import prices grew faster, especially oil prices.

Summing up

All of this suggests that Japan's surpluses are not about to wither but are about to grow larger. Of course, a sharp appreciation of the yen could untrack this move. And ongoing oil market price developments will also temper any conclusion made about the path of the nominal deficit. More important than that will be Japan's ability to restart its nuclear reactors and to cut its domestic oil consumption and therefore cut oil imports. In short, the path of the surplus or deficit has many influences. Foreign and domestic economic growth rates remain the most important drivers. And Japan has recently put in a better quarter of growth which by itself will raise demand for imports. If foreign growth is picking up, there will be more demand for Japanese exports as an offset. Away from those aspects, there will be the impact of export and import prices on trade which will also be affected by how exchange rates move. While U.S. President Donald Trump has been on a war-path about free and fair trade, he so far has kept any naming of Japan out of the mix of his criticism. However, there is no telling how long that will last.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief