Global| Mar 12 2008

Global| Mar 12 2008Japan GDP is Revised Lower

Summary

Japan’s GDP was revised lower in Q4 on weaker capital spending. Japan's gross domestic product increased a real 0.9% in the quarter during the October-December period, or 3.5% in annualized terms. That was lower than the original [...]

Japan’s GDP was revised lower in Q4 on weaker capital

spending. Japan's gross domestic product increased a real 0.9% in the

quarter during the October-December period, or 3.5% in annualized

terms. That was lower than the original estimate made a month ago of an

annualized 3.7% growth. Capital spending was revised down to a 2.0%

on-quarter rise from preliminary 2.9% advance.

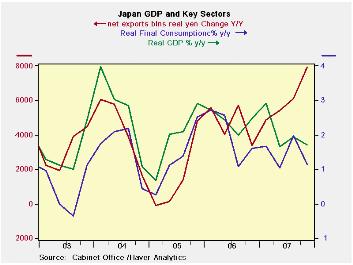

Japan’s GDP picture shows differing trends. The chart shows

that net exports are continuing to push GDP to stronger growth rates.

But real personal consumption trends are decelerating. Exports are

still growing strongly while real imports are being curtailed by

domestic weakness. Domestic demand in general is weakening with a Y/Y

growth rate of just 0.2% in Q4. Gross fixed capital formation is

negative and showing a sharp contraction. Housing is a leading negative

investment sector. Business plant and equipment expenditures have

steadied at a less than a 1% growth pace. In the recent quarter

government spending accelerated sharply hiking the yr/yr pace. Private

consumption did pick up in the quarter but the year/year pace

decelerated nonetheless. With the yen rising Japan will either have to

compete harder in overseas markets or supplement trade-led growth with

stronger domestic demand.

For Japan, several cyclical indicators have become more

positive already. Its own economy watchers index has stopped its

decline but is still weak. Machinery orders have picked up. And, the

OECD composite leading indicators show that Japan’s index is making a

turn for the better after experiencing the worst slump among OECD

member countries so far in this cycle. But the US leading indicator is

weakening and the US remains an important export market for Japan.

| Japan GDP | ||||||||||

|---|---|---|---|---|---|---|---|---|---|---|

| Consumption | Capital Formation |

Trade Domestic |

||||||||

| GDP | Private | Public | Gross Fixed Capital |

Plant& Eqpt |

Housing | Exp Imp |

Exports | Imports | Demand | |

| % change Q/Q at annual rates of change; X-M is Q/Q change in Bil of Real Yen | ||||||||||

| Q4-07 | 3.5% | 0.9% | 3.6% | -0.1% | 8.1% | -32.3% | 2.4 | 13.2% | 2.2% | 1.6% |

| Q3-07 | 1.2% | 0.6% | 0.6% | -3.9% | 3.7% | -29.4% | 2.6 | 12.2% | -0.5% | -0.9% |

| Q2-07 | -1.5% | 0.6% | 1.2% | -9.6% | -6.4% | -16.4% | 0.6 | 4.6% | 2.1% | -2.0% |

| Q1-07 | 3.8% | 2.5% | 0.8% | 1.5% | -1.8% | -5.0% | 2.3 | 14.8% | 4.1% | 2.1% |

| % change Yr/Yr; X-M is Yr/Yr change in Gap in Bil of Real Yen | ||||||||||

| Q4-07 | 1.7% | 1.1% | 1.6% | -3.1% | 0.8% | -21.5% | 7.9 | 11.1% | 2.0% | 0.2% |

| Q3-07 | 1.9% | 2.0% | 0.3% | -1.2% | 0.6% | -11.4% | 6.1 | 8.6% | 1.5% | 0.8% |

| Q2-07 | 1.7% | 1.0% | 0.6% | -0.6% | 0.3% | -3.0% | 5.4 | 7.9% | 1.4% | 0.6% |

| Q1-07 | 2.9% | 1.7% | 0.8% | 3.3% | 7.1% | -1.1% | 4.9 | 7.6% | 1.9% | 2.0% |

| 5-Yrs | 2.1% | 1.4% | 1.3% | 0.8% | 5.2% | -4.2% | n.a. | 9.6% | 4.2% | 1.3% |

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief