Global| Jul 27 2007

Global| Jul 27 2007Japan: CPI and Retail Sales Weaken--Discouragingly

Summary

It was looking promising in Japan: deflation was ending, finally, after almost 8 years. The most watched measure there, the core CPI excluding fresh food, had fallen from the middle of 1998 through April of 2006, according to the path [...]

It was looking promising in Japan: deflation was ending, finally, after almost 8 years. The most watched measure there, the core CPI excluding fresh food, had fallen from the middle of 1998 through April of 2006, according to the path of the year-over-year percent change. The overall amount of deflation wasn't all that bad: the index, seasonally adjusted, fell from a high of 103.4 in mid-1997 to a low of 99.9 in several months of 2005. But it was promising to see the index bottom out and begin to rise. The latter months of last year didn't see any big increase, but it really seemed that retailers were regaining some pricing power, necessary for the economy to sustain a self-reinforcing expansion.

But prices have not been able to sustain this new uptrend. This specific measure, the General CPI excluding fresh food has been down year-on-year since February, and today, the Ministry of Internal Affairs and Communications reported that June was a fifth consecutive month of decline, 0.1% from June 2006. This core index level is the blue line in the first graph.

The green line in that graph is a Western-style core index, the total less all food and energy. It highlights that the "recovery" we thought we saw in the other index was really concentrated in energy and that other prices continued down. The rate of decline eased in this index, but the year-on-year rate has never turned positive.

The June data show continuing weakness in housing, especially imputed rents, household furnishings, communications and reading & recreation. Clothing and vehicle prices and public transportation charges have been edging marginally higher. Medical care and the "miscellaneous" category are up somewhat, the latter due mainly to an administered increase in tobacco prices.

With consumer prices unable to increase, it doesn't really seem surprising that retail sales have not risen either. The Ministry of Economy, Trade and Industry (METI) today reported a monthly decline of 0.8% for June, and a year-on-year reduction of 0.4%. Stores did have rising sales from 2003 through the middle of last year, a period when prices were falling. So price behavior isn't the only determinant. Individual store categories are showing mixed performances, with general merchandise outlets having persistent gains. But clothing stores saw notable drops in June, and motor vehicle dealers more than reversed a good April increase in May and June. Household appliance stores, facing a downtrend in home furnishings prices, have also been experiencing declining sales.

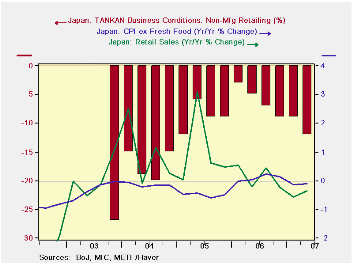

At the beginning of this month, the fabled TANKAN survey indicated that businesses were more optimistic in Q2. While this is generally true, the assessments of retailers have diminished. For "all enterprises" in retailing, the "actual conditions" measure turned weaker in Q2 2006 and has continued to deteriorate since, along with both prices and sales. Sigh.

| JAPAN | June 2007* | May 2007* | Apr 2007* | Year/ Year | 2006 | 2005 | 2004 |

|---|---|---|---|---|---|---|---|

| CPI, General | -0.1 | 0.2 | 0.2 | -0.2 | 0.2 | -0.3 | 0.0 |

| CPI ex Fresh Food | 0.0 | 0.1 | 0.1 | -0.1 | 0.1 | -0.1 | -0.1 |

| CPI ex Food & Energy | -0.1 | -0.1 | 0.1 | -0.4 | -0.4 | -0.4 | -0.6 |

| Retail Sales | -0.8 | 0.6 | 0.3 | -0.4 | 0.1 | 1.0 | 1.0 |

Carol Stone, CBE

AuthorMore in Author Profile »Carol Stone, CBE came to Haver Analytics in 2003 following more than 35 years as a financial market economist at major Wall Street financial institutions, most especially Merrill Lynch and Nomura Securities. She had broad experience in analysis and forecasting of flow-of-funds accounts, the federal budget and Federal Reserve operations. At Nomura Securities, among other duties, she developed various indicator forecasting tools and edited a daily global publication produced in London and New York for readers in Tokyo. At Haver Analytics, Carol was a member of the Research Department, aiding database managers with research and documentation efforts, as well as posting commentary on select economic reports. In addition, she conducted Ways-of-the-World, a blog on economic issues for an Episcopal-Church-affiliated website, The Geranium Farm. During her career, Carol served as an officer of the Money Marketeers and the Downtown Economists Club. She had a PhD from NYU's Stern School of Business. She lived in Brooklyn, New York, and had a weekend home on Long Island.

More Economy in Brief