Global| Sep 19 2016

Global| Sep 19 2016Italian Trade and Current Account Surpluses Slip

Summary

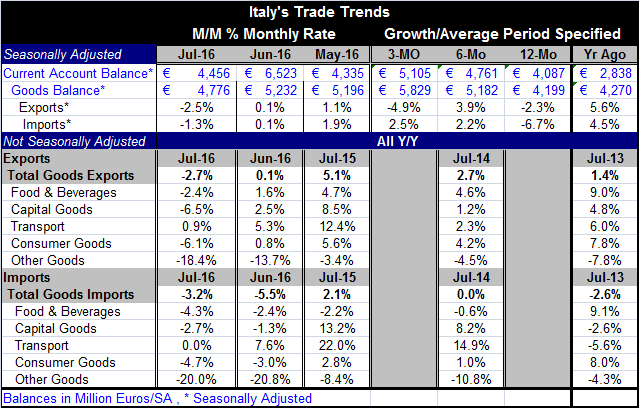

Italy's trade and current account surpluses are shrinking in July. The shrink is based on a drop in exports on the month that is larger than the drop in imports, a sort of economic race to the bottom. A smaller surplus will subtract [...]

Italy's trade and current account surpluses are shrinking in July. The shrink is based on a drop in exports on the month that is larger than the drop in imports, a sort of economic race to the bottom.

Italy's trade and current account surpluses are shrinking in July. The shrink is based on a drop in exports on the month that is larger than the drop in imports, a sort of economic race to the bottom.

A smaller surplus will subtract from Italian GDP growth, in an economy that already is weak. The weakness is apparent from the decline in imports, not just in July, but ongoing declines over the last four years back to 2013 -years running. Only part of that decline reflects weak oil prices. Italy is weak and has been struggling with competitiveness issues both inside and outside the euro area. Demand has been weak both inside Italy and from foreign sources.

Over the past year Italian imports are off by 3.2% and up by a thin 2.1% for the 12-months ended July 2015 and after being flat in 2014 (all percentages are over for 12-month periods ending in July). Of the five major import categories (foods & beverages, capital goods, transportation equipment, consumer goods, and other goods), imports declined in four over the past year and were flat in the other category (transportation equipment). Imports fell in only two categories over the previous 12-months, and showed no real life in the 12-months ended in 2014. In 2015, there was strength only for capital goods and transportation equipment. There is quite a legacy of import weakness and it is broad-based.

Italy shows a decline in exports over 12-months, but a more substantial rise in exports of 5% over the previous 12-months. Exports are lower in four of five categories over 12-months (like imports, the exception is transportation equipment). Over the previous 12-months to that, exports showed more life with declines in only one category, other goods. In 2014 and 2013, exports grew at a nominal pace of less than 3% in each year.

Italy shares a trend with Germany for weakness in capital goods. Euro area growth has been driven by mostly its consumer goods sector in this recovery. With exports being hit hard, there is now concern that exports could become more of a problem for overall growth as demand conditions outside the EMU remain weak and are eroding EMU-area growth itself through the export channel. With global capacity slack for such a protracted period of time, we are seeing weakness in Italian capital goods exports and imports that parallels the weakness we have seen in the German capital goods sector. This is not a competiveness issue as the euro exchange rate is still very weak (low-valued). But it is evidence of weak demand for capital goods and potentially a more substantial loss in demand and in overall economic stimulus for the EMU, Germany and Italy.

Euro Area Trends

The euro area as whole is not benefiting from trade as it once did. Exports and imports of manufactured goods are falling at annualized growth rates in excess of 20% over three-months. There are clear 12-months drops for exports and imports as well; the weakness in both flows is accelerating. On new data released today, we see the EMU-wide current account surplus contracted sharply in July to 21 billion euros from 29.5 billion euros. This eight and one-half billion euro monthly contraction is driven by trade which saw its surplus contract by 5.9 billion euros. But there is also an increased outflow of current transfers of 3.6 billion euros more than in June; June already had deteriorated by 1.2 billion euros from its July total. An increased migrant presence in the EMU is likely leading to more monies being remitted back to those who were not able to gain the sanctuary of Europe. This is turn weighs on the current account, reducing GDP growth in the EMU and may set in motion countervailing forces to try to re-stimulate exports to cover the erosion in the current account surplus.

In economics, most markets are connected in one way or another. Connections can be direct and strong or obtuse, indirect and weak. What we see in Europe is evidence that the global weakness is weighing on the EMU. Weakness in exports and imports is pervasive. The knock-on impact to a weaker capital goods sector is evidence and that weakness will create more knock on effects to the purely domestic portion of the economy that also will reverberate.

International risk is not on the decline as much as it is biding its time

In a seemingly unrelated event, the Bank for International Settlements (BIS) reported today that China's bank stress gauge is at level that is more than three times above the BIS danger level. China's credit-to-GDP-gap is at a ratio of 30:1 in Q1 2016. The BIS believes that risk is indicated when that ratio hits a value of ten to one. A year ago the BIS put China's ratio at 25:1. I mention this because as stated above all markets are linked in some way. We know how important China is to the global economy. If China were to have a banking crisis, it would be foolish to assume that there would not be fallout for external markets. The BIS warning on China is just another example of policymakers kicking the same can down the road and ignoring danger signals as they arise - even if those danger signals are getting worse. In the U.S., we keep hearing that the international risks are stabilizing making the way safe for a Fed rate hike. On what planet is that happening? China is a risk; so is its banking sector. So is Italy's banking sector. That the U.K. is at risk to Brexit is clear even if the exact nature of the risk remains undefined - and that will remain so until detailed talks get under way. Clearly the U.K. will get an adverse growth shock from its actual EU exit when that comes. But now there can be no reaction to it since the nature of the shock, its magnitude and timing all are too uncertain to pin down. But that does not make them any less real.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief