Global| May 15 2017

Global| May 15 2017Italian Core Inflation Plays Catch-Up With Germany

Summary

Italian inflation is accelerating. It is up at a strong pace over three months and six months after lagging the pack in this cycle. In March, Italy had the second slowest pace of core inflation over three months, six months and 12 [...]

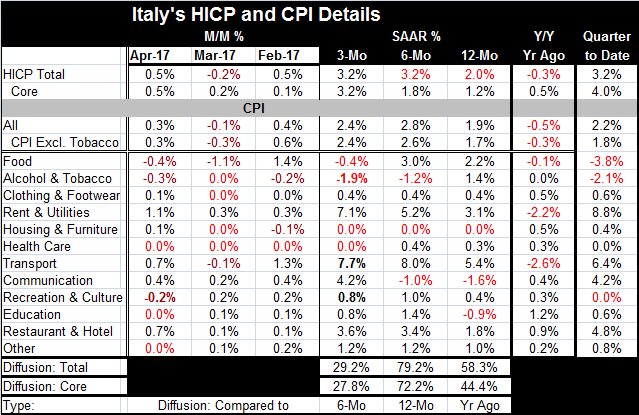

Italian inflation is accelerating. It is up at a strong pace over three months and six months after lagging the pack in this cycle. In March, Italy had the second slowest pace of core inflation over three months, six months and 12 months among the four largest EMU economies. Now as the earliest core inflation-reporter of this group for the month, Italy has announced a core rate that is up sharply at a 3.2% annualized rate over three months, boosting its year-on-year rate to a still-weak 1.2% gain. The 1.2% gain is still modest as last month a 1.2% core still would have ranked as the third fastest among the core rates of the four largest EMU economies, behind Spain and Germany. Last month Italy's 1.5% headline gain also ranked third over 12 months, but it had the strongest headline gain over three months. At 3.2% in April, Italy's HICP three-month gain is softer than its 3.6% rise in March, but its year-on-year gain is up to 2% which is the ECB's speed limit for all of the EMU.

Italian inflation is accelerating. It is up at a strong pace over three months and six months after lagging the pack in this cycle. In March, Italy had the second slowest pace of core inflation over three months, six months and 12 months among the four largest EMU economies. Now as the earliest core inflation-reporter of this group for the month, Italy has announced a core rate that is up sharply at a 3.2% annualized rate over three months, boosting its year-on-year rate to a still-weak 1.2% gain. The 1.2% gain is still modest as last month a 1.2% core still would have ranked as the third fastest among the core rates of the four largest EMU economies, behind Spain and Germany. Last month Italy's 1.5% headline gain also ranked third over 12 months, but it had the strongest headline gain over three months. At 3.2% in April, Italy's HICP three-month gain is softer than its 3.6% rise in March, but its year-on-year gain is up to 2% which is the ECB's speed limit for all of the EMU.

Italy, Germany and oil

Until the rest of the Big Four economies report, we cannot compare where Italy stands this month. But its core shows acceleration even as the headline has simmered down a bit. Due largely to imposed austerity, Italy's core inflation has been running below the core in Germany since 2013. But from 2007 through 2012, Italian core inflation had run substantially higher than Germany's pace as it had for most of Italy's tenure in the euro area. The question now is whether Italy's days of discipline are over or whether this strong move from inflation is temporary and - even though it is the core- possibly oil-related since these costs do have to be passed on even if indirectly.

Some trends are still mixed

In April, only three of the 12 price categories in Italy's domestic CPI show declines with three more essentially unchanged. In March, two categories were lower with four essentially unchanged and the drops were large enough to drive the headline and the core rates lower as well. In February, prices fell in only two CPI categories and were essentially unchanged on one other. Despite the widespread price weakness over three months, there were substantial gains logged in prices in the transportation sector and in rent and utilities, reflecting sharply rising energy costs.

Diffusion does not exactly line up with inflation pressures

The diffusion story is interesting. Diffusion is a measure of the 'the breath of price gains' so we gauge and apply this metric on compounded rates of inflation over various horizons. Here we compare inflation from 12 months ago to now, over 12-month to six-month, and over six-month to three-month. We look for sequential trends. For overall prices diffusion shows inflation is widely decelerating from six-month to three-month, a period when the overall HICP inflation rate has been flat at a 3.2% pace. Diffusion tells us that, despite the unchanged pace, inflation has declined in more categories than it increased. Weakness is widespread. The core diffusion reading echoes that theme even though the core HICP rate itself moves up to 3.2% from 1.8%. However, from 12-month to six-month, both headline and core inflation rates accelerate sharply by 1.2 percentage points for the headline and by 0.6 percentage points for the core. And both show that the acceleration was widespread on diffusion readings in the 70 percentile decile that confirm a greater breadth of prices accelerating up and down the line among components. Over 12 months, both core and headline inflation rates moved sharply higher, compared to the period of 12 months earlier. Headline inflation accelerated by 1.7 percentage points while core inflation accelerated by 0.7 percentage points. Yet, headline diffusion logged a reading of 58%, which does show moderate inflation breadth. Core inflation's diffusion reading was actually lower (44%) even though the core rate itself accelerated noticeably (but in a month with huge gains in noncore items like food (2.2%), rent and utilities (3.1%) and transportation (5.4%).

Inflation path and gradient are muddied

All of this muddies the waters a bit on inflation pressure. Core inflation accelerates on all these horizons. Headline inflation accelerates then holds flat at an elevated pace. Diffusion gives some mixed signals. Here we have calculated diffusion from the domestic CPI components and they show inflation has picked up relative to a year ago as do the HICP headline and core, but domestic inflation trends are flatter and more mixed. On the question of how broad-based is inflation, we get the odd result that the rise over the past year is not so strong and the recent three months gains are not either. Moreover, inflation diffusion actually is weaker for year-on-year changes among core items.

Draghi's views and Italy's trends

The lack of a clear, consistent inflation threats is exactly what Mario Draghi has been fixated on as he has argued that there is little evidence of inflation beyond that caused by oil and its knock on effects. Italy's details seem to continue to bear that out.

And oil moves up again

However, in oil market developments today, Russia has finally joined in with the Saudis on the notion of a stretch out of these current production quotas and has more aggressively suggested that the extension should stretch through early-2018. Of course, these are words and it is deeds that will matter. But for now, words are carrying the day and carrying oil prices higher, ending the recent period of price lethargy.

Growth: a question of punctuation: Growth! Or Growth?

The policy environment is continually up for re-inspection. While OPEC and Russia may now be on the same, more austere, oil output page, some of the recent global data have turned less upbeat. We still see an optimistic bent to markets and economists who want to portray a weak U.S. retail sales report as better. And better it was...still, 'better' may not be 'good' or even good enough. Today we see a sharp weakening in the U.S. indicator the Empire State manufacturing index, a Northeastern measure of manufacturing activity from the Fed's second district (NY). China's data on the day also showed some modest slowdowns in play. While there is an expectation of a rebound in the global economy, there has also been some untracking of that trend recently. Growth remains in gear, but the degree of acceleration and the prospect for any growth acceleration to have staying power is very much up in the air. The global economy growth outlook still has many more question marks than exclamation marks. As determined as policymakers may sound in some of their proclamations, they continue to make policy on a skim of thin ice.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief