Global| Nov 26 2014

Global| Nov 26 2014Italian Consumer Confidence in an Era of Radioactivity

Summary

Italy's consumer confidence indicator from ISAE fell in November to reach a nine-month low. In the guts of this survey, we see evidence many of the conditions that are continuing to plague consumers around the world. For example, [...]

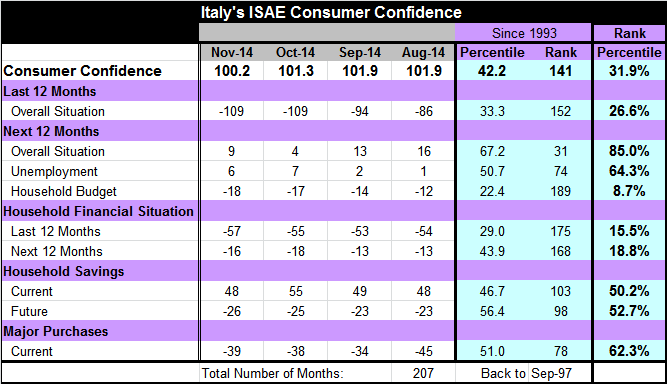

Italy's consumer confidence indicator from ISAE fell in November to reach a nine-month low. In the guts of this survey, we see evidence many of the conditions that are continuing to plague consumers around the world. For example, Italians are `confident' about the future as their expectation for the overall situation 12 months from now stands in the top 15% of its historic queue of responses.. But this `optimism' is undone by the evaluation of the financial situation which is assessed to have been in the bottom 15% of its historic queue over the last 12 months and is only improving to the bottom 18% of its queue over the next 12 months. In addition, the household budget is rated as a bottom 8.7% standing over the next 12 months- stronger about 91% of the time. rarely worse.

Italy's consumer confidence indicator from ISAE fell in November to reach a nine-month low. In the guts of this survey, we see evidence many of the conditions that are continuing to plague consumers around the world. For example, Italians are `confident' about the future as their expectation for the overall situation 12 months from now stands in the top 15% of its historic queue of responses.. But this `optimism' is undone by the evaluation of the financial situation which is assessed to have been in the bottom 15% of its historic queue over the last 12 months and is only improving to the bottom 18% of its queue over the next 12 months. In addition, the household budget is rated as a bottom 8.7% standing over the next 12 months- stronger about 91% of the time. rarely worse.

There is cognitive dissonance here. Consumers -households- want to believe that things will improve. But when they look at the cold hard facts, the nuts and bolts of the situation are really grim. In the consumer confidence report released in the U.S. yesterday, Conference Board survey respondents put their expectations for income in the bottom 25% of its historic queue of responses. Consumers everywhere are wary and worried about their financial conditions in the future.

The Italian overall confidence assessment stands in its 31.9 percentile. That means it has been better historically about 68% of the time (worse only 32% of the time). This is not a good reading. And the trend is falling. The overall situation is placed in its 26.6 percentile, nearly in the bottom quarter of its range.

The expectation for unemployment in Italy among households is in its 64th percentile, near the top third of the historic `fear of unemployment' range. That fear has been steadily growing in recent months. Italy is on a deteriorating trend, not an improving trend. Conditions are poor and they are worsening.

Italy and France apparently are going to be cut some slack on their budget proposals and the EU Commission is not going to force strict compliance on this in this round. But Italy is flirting with a debt-to-GDP ratio that could soon put it on a path for automatic austerity.

We see little evidence that Germany is trying to help its fellow EMU members. While everyone in EMU is under the yoke of austerity, and Germany is surging ahead as the beneficiary of export-led growth, Germany is also putting the screws down on its own already well-contained budget instead of letting out some slack to stimulate domestic demand and help EMU-wide growth.

Not only is there no EMU-wide fiscal approach, there is also no EMU-wide vision or willingness to compromise by individual members. There is still an underlying struggle to control policy and establish what the EMU-wide culture will be. This `One Musketeer' approach (one for one, and one for one!) is a destructive spirt in a currency union where members' interests are tied together. Germany can't help but expect that union members are going to twist and stretch the ECB's mandate to close to the breaking point as long as Germany itself is so unhelpful on fiscal matters.

The European Monetary Union still has not come to grips with the kinds of responsibilities and sacrifices that member countries need to make for each other as well as for the sake of union stability under the single currency umbrella. Instead there is this invisible tug-of-war to redirect Europe to a more Germanic or more Southern European set of beliefs. So far members have engaged in a very isolationist approach in which the strong hang on to their advantage and wait for a disaster to befall the weak, then deal with it. It is exactly this mentality that makes me wonder about the half-life of this union that seems to be radioactive, radioactive.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief