Global| Dec 20 2019

Global| Dec 20 2019Italian Confidence Rebounds Against a Declining Trend and Changing Global Environment

Summary

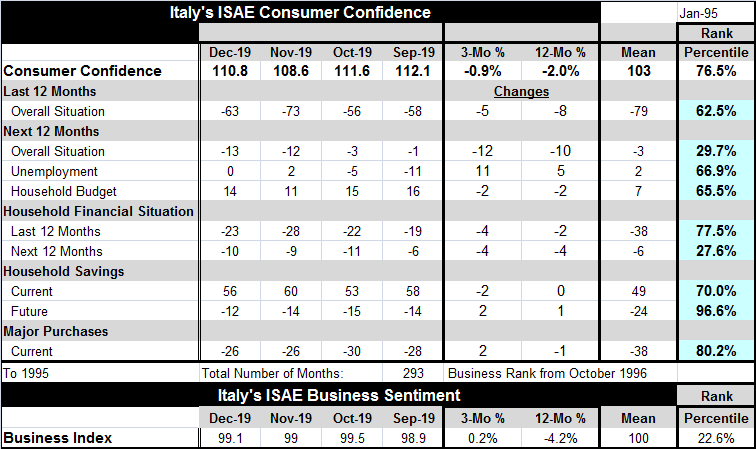

Both business and consumer confidence made moves higher in Italy in December to send the year out on a more hopeful note. Both series are embroiled in declining phases going back to late-2017 or early-2018. Business confidence has [...]

Both business and consumer confidence made moves higher in Italy in December to send the year out on a more hopeful note. Both series are embroiled in declining phases going back to late-2017 or early-2018. Business confidence has made the smallest possible move higher in December, rising by one tick. Consumer confidence has made a more substantial rebound, rising to 110.8 in December from 108.6 in November. Still, it’s only one month.

Both business and consumer confidence made moves higher in Italy in December to send the year out on a more hopeful note. Both series are embroiled in declining phases going back to late-2017 or early-2018. Business confidence has made the smallest possible move higher in December, rising by one tick. Consumer confidence has made a more substantial rebound, rising to 110.8 in December from 108.6 in November. Still, it’s only one month.

Both business and consumer confidence are lower on balance over 12 months and by sizable amounts. Over three months, consumer confidence is also slipping, but business confidence mounts a small gain compared to September. Still, the bottom line is that momentum is lower and this month is a countertrend move.

Short-lived countertrend or new trend?

The rebound this month raises the question of whether this month is a countertrend blip or the beginning of a rebound with staying power. This question does not arise out of the power of the ‘rebound’ in either series, but in their moves coupled with a number of other changes apparent in Italy in Europe and across the global economy rise new questions and hopes.

What has changed/is changing?

Several ‘big picture’ changes are in the offing. Two disrupters are going to stop making mischief and start making policy. Here I refer to Donald Trump (who may never really stop making mischief…) and Boris Johnson in the U.K. The U.S. has a phase-one trade deal with China. That deal does not end its trade dispute but puts it in a different framework and on a positive path. The U.S. also has concluded (is concluding) its revised NAFTA trade deal (USMCA) with its North American trade partners. Boris Johnson now has the political power to consummate Brexit and that will (eventually) remove more uncertainty but still may be disruptive. Sweden has exited wild and wacky world of NIRP. With a new head in place at the ECB, its own NIRP is being reexamined. So there is change, significant change, afoot in the global economy. The prognostication of the ZEW financial experts for a group of mostly G7 countries that includes all of the EMU region has taken a great deal of its pessimism off the table. It is still the case that the ZEW assessments for Italy, the EMU and the U.S., to name a few specific countries and regions, are negative and the outlook is still decidedly negative, but conditions have been seen as less negative than they were previously. And the easing in U.S. monetary policy has contributed to this view in addition to the trade policy events.

But removing the weight of pessimism is only part of what the global economy needs. Monetary policy in the U.S. ‘thinks’ it is done being stimulative. Maybe it is, maybe it isn’t. Fiscal policies are largely being kept in check (the U.S. was an exception, but it may not be going forward). Italy continues to push the EU (EU Commission) for more fiscal flexibility, but with Italian debt so high, there is little taste for giving Italy more fiscal freedom here. Italy, like Japan, is left with few policy options hoping that the rising tide from new U.S.-China trade deal and, hopefully, from improved global conditions will raise its boat along with all the others.

However, there is little in the way of new stimulus in train. Monetary policy is done, or set to be done, or in the process of reversing. For the most part the pick-up people expect will be spawned by the removal of uncertainty and the reinvigoration of global trading. But is that going to be enough? There is still global aging in gear. Countries have relied on debt to spur growth in the wake of the great global recession. Of course, Italy is an exception as it was under the yoke of austerity; as a result, official estimates of Italian GDP are still below its pre-recession level of more than ten years ago.

Going forward the modern economy is far more likely to be wracked with political discord, a factor that will make domestic policy making and international coordination more difficult. Italy’s political process is in turmoil. In France, Macron is all but under siege because of his plan for pension reforms. The U.K. has just finished a major national election to sort things out and to focus on Brexit, but this path has brought it into conflict with Scotland and Northern Ireland. Scotland is pressing for another referendum on its union with Britain because it is not eager to leave the EU. German politics are in turmoil and the steady hand of Angela Merkel is being replaced on the tiller. China has slowing growth and a real problem in Hong Kong. It is battling counter claims to its rogue grab of the South China Sea. The Middle East is as always in flux and in turmoil. Israel cannot form a government and Turkey is acting rogue after buying Russian missiles and joining Russia in a pipeline deal that the U.S. opposes. North Korea has a big deadline coming up and it could lead to the return of rocket man instead of a move toward peace. And of course there is still much more including the ongoing impeachment of U.S. President Donald Trump and a terrible partisan split beyond that.

In short, there is a great deal of domestic and international flux. We have exited the Post War era and not old war-time alliances are not enough to keep countries on the same policy page. Once countries sort out their more modern differences we could emerge from this stronger than before with new shared values of a more modern sort. But until or unless that happens, there is a great deal of discord and much of it is over trade and making trade fair (fairer). That could offer new and better prospects for all or it could mire down in endless disputes about trade fairness and trade access and exchange rate policy.

As things stand, I think there is too much optimism over the U.S.-China trade phase-one accord. Even with more certainty, Brexit is going to be disruptive. And the emerging and developing problems from climate change could become an even larger impediment to cooperation in the future. There is progress and reason for hope but also reason to keep both feet on the ground.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief