Global| Aug 29 2016

Global| Aug 29 2016Italian Business and Consumer Confidence Both Erode

Summary

Italian business and consumer confidence both sank in August. The Consumer Consumer confidence has been falling rapidly after having spiked in October 2015 and peaked on-one month later. Confidence has fallen in three of the last four [...]

Italian business and consumer confidence both sank in August.

Italian business and consumer confidence both sank in August.

The Consumer

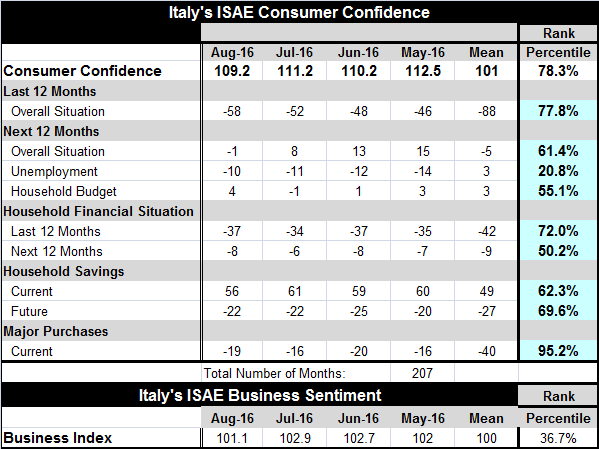

Consumer confidence has been falling rapidly after having spiked in October 2015 and peaked on-one month later. Confidence has fallen in three of the last four months with a small increase in July being the exception. The consumer confidence index is lower by over 9 points in a span of four months.

Businesses

Business confidence in Italy has been more steadily eroding. It has had several waves of ups and downs in recovery with the last peak occurring in October 2015. After peaking at a level of 10.5, that index has shed only 4.4 points over the ensuing 10-months.

Different paths then and now

The chart at the top of this report shows clearly that consumer confidence has made the greatest gains since bottoming in 2011 and 2012. The business index has had a number of mini-cycles in the recovery period, but none of them have brought the index back to its 2007 high. On the other hand, the consumer index has reached back to and exceeded its prerecession high reached of 2002. But after attaining that peak, consumer confidence has acted more like Icarus plunging to lower level while falling somewhat wildly.

Reality bites

It is not clear whether it is this month's decline in consumer confidence that should be called `unexpected' or if the past increases in confidence should be called unexpected as well as `unexplained.' Italy's economic performance has not been very good. The troubles of its banks are so much in the news that no literate Italian could be unaware of them. Moreover, the secessionist Five-Star Movement has been gaining ground in Italian politics- a clear sign of dissatisfaction. So it is strange that amid all these indicators of dissatisfaction and trouble that the Italian consumer had appeared to have been so satisfied. Suddenly reality bites.

Consumers feel better than businesses

Consumer euphoria has topped businesses perceptions of conditions. Ranked on data back to June 1999, the business index stands only in its 36th queue percentile, implying that it has been this low or lower only about 36% of the time. The consumer gauge despite its more rapid slippage carries a 78th percentile ranking among its historic observations. The consumer has felt better off only about 22% of the time (100% - 78%).

The source of consumer confidence

The strongest standing among the responses by the Italian consumer is the ranking on the state of conditions for making major purchases; that response `score' has been better only about 5% of the time since mid-1999. The prospect of unemployment has been lower only about 20% of the time although that response has been losing some ground over the last four months. Italians rate the overall situation over the last 12-months as better only about 22% of the time, but looking ahead they expect conditions to be such that they have been expected to be better historically only about 40% of the time. Italians rate their financial conditions as having been better only 28% of the time over the past 12-months, but over the critical `next 12-months' they except their financial conditions be to near what they are about on average with a 50th percentile standing of their response.

Will confidence continue to erode?

To some extent, it appears that Italian consumer confidence is better because Italians themselves have not fully come to terms with the deteriorating environment around them. The expected overall situation, for example, has slipped from a 15 reading in May to a minus-one reading in August. The 61st percentile standing for that component suggests that confidence still has a ways to slide to reconnect with the expected future and to disengage from the way-we-were past.

Business confidence is still underpinned by orders

Businesses find that domestic and foreign orders are holding up somewhat better than the overall confidence index in terms of how their responses for these categories rank. But for businesses too, there is erosion in train as the expectation for total orders has slipped from a -15 reading in May to a -18 reading as of August.

Pressures in EU/EMU

Italy remains as an economy under pressure and facing challenges. Right now it may be the economy to watch in Europe as tensions mount. Italy has its five-Star Movement gaining ground, ongoing migrant issues and a banking sector problem that will be hard to resolve. The EU is taking a hardline with Italy over helping its banks. Both Spain and Portugal have secessionist issues brewing on the political front. Spain can't seem to form a workable government. France and the U.K. have a border issue involving migrants, as migrants seeking entry to the U.K. are piling up in Calais giving the French headaches. Germany has its own migrant issues; while its economy is still performing well, the German trade association BGA has cut its projection for German export growth in 2016 to the 1.8% to 2% range from what has been a forecast of 4.5% growth previously. And as we have documented in an earlier report, money and credit growth in the EMU once adjusted for inflation show no stimulus in train what-so-ever. There are tensions and issues throughout the EMU region and there are still the upcoming negotiations between the U.K. and the EU over what their new relationship will look like. There is still a lot to stir the pot about in the EU/EMU. A Fed rate hike - if one of those is indeed now more likely - could be another ingredient capable of fomenting further chaos in Europe - as if it needs any more.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief