Global| Jul 10 2020

Global| Jul 10 2020Italian and French IP Make Strong But Incomplete Recoveries

Summary

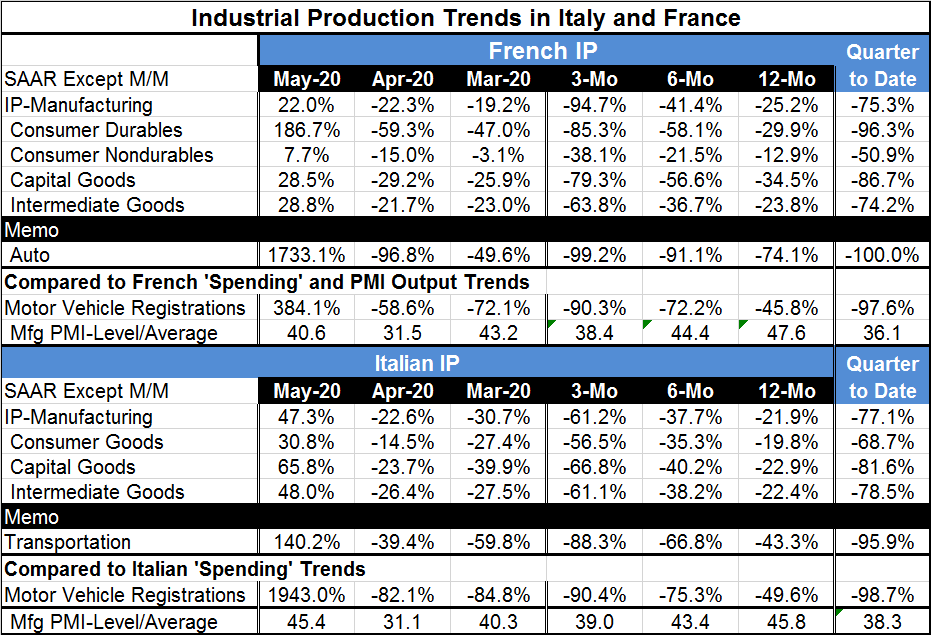

French IP rose by 22.0% in May while Italian IP gained 47.3% on the month. Both of those results, in isolation, are stunning numbers. But after the dust and smoke and mirrors of the rebound are carried away, IP in France is still [...]

French IP rose by 22.0% in May while Italian IP gained 47.3% on the month. Both of those results, in isolation, are stunning numbers. But after the dust and smoke and mirrors of the rebound are carried away, IP in France is still lower by 25.2% over 12 months and IP in Italy is still lower by 21.9% over 12 months. Both manufacturing series are showing sequential deceleration on annualized growth rates from 12-months to six-months to three-months. In short, the rebounds are (historically) strong and solid, but they fall well short of what will be needed. Each of these countries has suffered a series of severe output declines and while each now shows a strong one-month rebound, there is still a long slog ahead to restore the level of output to its pre-virus levels and to put growth back on a sold expansion path.

French IP rose by 22.0% in May while Italian IP gained 47.3% on the month. Both of those results, in isolation, are stunning numbers. But after the dust and smoke and mirrors of the rebound are carried away, IP in France is still lower by 25.2% over 12 months and IP in Italy is still lower by 21.9% over 12 months. Both manufacturing series are showing sequential deceleration on annualized growth rates from 12-months to six-months to three-months. In short, the rebounds are (historically) strong and solid, but they fall well short of what will be needed. Each of these countries has suffered a series of severe output declines and while each now shows a strong one-month rebound, there is still a long slog ahead to restore the level of output to its pre-virus levels and to put growth back on a sold expansion path.

For now the virus is still spreading and is still an issue that keeps the outlook walking on eggshells.

In addition, the negotiations in the EU about a stimulus plan drag on. While there is some optimism among European Union countries of the South that they will get the result they seek, both sides continue to bargain and there is no sense of agreement yet on whether financial help will be packaged as loans or as a grant. Southern Europe is adamant that it needs grants while the North has familiarly taken the positon that it does not want the union to turn into a welfare union. The beat goes on....

Meanwhile, vehicle output in both France and Italy as well as vehicle registrations, are up sharply in May, but both are still substantially lower over 12 months. Both France and Italy still show manufacturing PMI values below 50 (indicating a net contraction in the sector) as of May. PMI data are available through June, however, and as of June French manufacturing is expanding again (PMI 52.1) and Italy is doing a bit better but still contracting (PMI 47.5).

On a shorter timeline, the rebound in IP is still found wanting as output in the quarter-to-date is falling at a 75.3% annual rate in France and at a 77.1% annual rate in Italy. Both of these are huge contractions on the heels of an already weak quarter.

Rebounds are strong but incomplete

The outlook is more complicated than usual. The rebound of the economies both of output and demand are in train, but both are subject to the vagaries of the virus and it has proved an elusive foe. It may seem be contained and then it simply pops up again. Countries that have controlled the virus and then reopen, no matter how long they have waited or how successfully the first ‘control’ was, still experience a rise in infections when they open. That would not be a such a bad thing if countries were going for herd immunity and protecting their most at risk, but so far only Sweden has a real policy of allowing the virus to spread and using herd immunity as an eventual solution. There are talks and plans for vaccines, but as of yet there are no vaccines.

All of this leaves the outlook at risk. In the EU, conditions are further complicated by the unwillingness of the financially strong countries to help the weak countries that have gone through so much pain in the wake of the last recession and after Herculean efforts to tame inflation. Will they get nothing for all their efforts but more debt and more scorn from their neighbors in the North?

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief