Global| Aug 14 2013

Global| Aug 14 2013It's Official (If Preliminary) as EMU Recession Ends

Summary

Well, it's a semi-official conclusion, if preliminary, but it nonetheless seems to be true that recession in the European Monetary Union is over. The GDP release is only at its 'flash value' which gives us the preliminary headline [...]

Well, it's a semi-official conclusion, if preliminary, but it nonetheless seems to be true that recession in the European Monetary Union is over.

Well, it's a semi-official conclusion, if preliminary, but it nonetheless seems to be true that recession in the European Monetary Union is over.

The GDP release is only at its 'flash value' which gives us the preliminary headline without the detail. Still, it's pretty clear that this 1.1% annual rate increase in the first quarter will remain a positive growth reading and send a signal that the recession for the monetary union has ended. Good riddance - I hope...

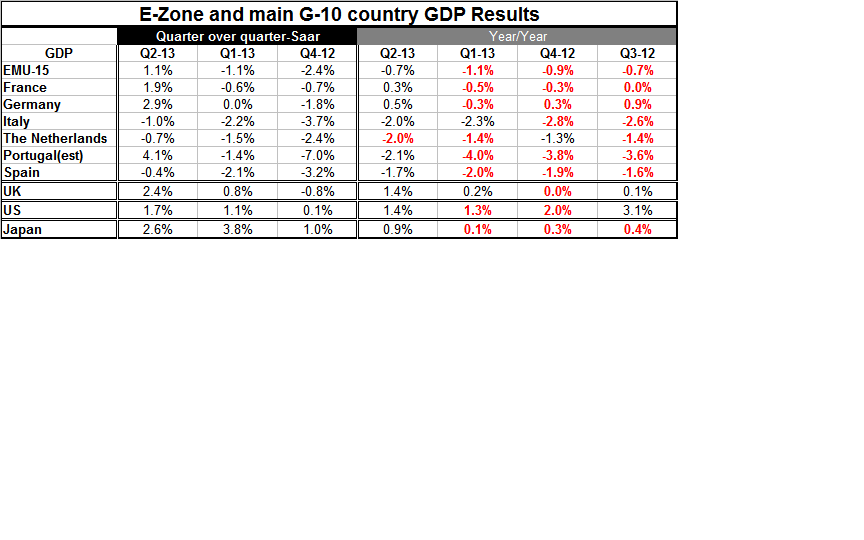

We list in the table six countries that are early reporters of their GDP statistics, of these six, three show GDP increases and three show declines. We list Portugal as an 'estimate' because we have cobbled together the quantitative estimate for the quarter from reports on the newswires although its official data are not yet in the database. If there is any revisions to the historic data for Portugal, the Portuguese numbers will have a slight error but we think that the main signal is the Portugal has posted a positive GDP number and recession has ended there as well. We prefer to include it in the table despite any minor flaws that might embody.

As you can see, there is a complication in calling EMU recessions and recoveries because the European Monetary Union countries are together in the Monetary Union. We will cite the Monetary Union itself as being in recession or out of recession, yet there may be countries in the Monetary Union after the Union has exited recession that will still remain in recession. Italy, Spain and the Netherlands appear to be three of those countries.

The chart at the top plots year-over-year growth rates and in that chart we can see that the UK right now is showing the most vigorous Q2 growth and momentum (year-over-year) of the three regions: EMU, the US and the UK. The Monetary Union appears to have put in a bottom while year-over-year GDP is still contracting. GDP growth on the quarter has turned up and some positive momentum is in gear. We can compare the GDP growth path of the Monetary Union to that of the United States whose growth is plotted on the same chart. During the interval that the Monetary Union slipped back into recession, the United States economy actually accelerated. Now, when the Monetary Union is stabilizing and accelerating, the US economy has decelerated. Yet the growth rate differences between the US and the Monetary Union currently are not as extreme as is the divergent positions they occupy in their respective business cycles.

Going back to Q1 1996 the current US-EMU annual growth rate difference (of 2.1%) only ranks as the 17th largest year-over-year growth-gap --a discrepancy that has been larger about 75% of the time. Yet, just four short quarters ago the growth gap between GDP growth rates in the US and EMU was the largest in the past 69 quarters. Still, It's not clear if the US and Europe are having a growth rate convergence of if yet another divergence is brewing.

While much of the policy focus remains on central banks and while the central banks in each of these regions has adopted some form of forward guidance and has either employed some variant of quantitative easing or, in the case of the ECB, other special lending that it could conduct consistent with its mandate, the path of the economy remains all-important. Monetary policy is not the tail that wags the dog as some would have you believe.

Monetary policy has acted as an additional crutch at a time that growth has been disappointing. The US is still leaning heavily on forward guidance while it's trying desperately to interpret its economic data as consistent with its thinly suppressed desire to cut back on -- instead of extend- its quantitative easing stimulus. The UK has just adopted forward guidance and that is done so with some opposition and internal dissent at the BOE. The announcement of a plan to use forward guidance by the ECB which had been made by Mario Draghi, was almost immediately undermined by the Bundesbank's Jens Weidmann who pointed out, I think quite correctly, that interest rates would not remain low under a policy of forward guidance if monetary policy required them to go up.

The statement by Weidmann most clearly and succinctly exposes the sham that is forward guidance.

If forward guidance is a pledge, then a central bank is sticking its neck out since none of them forecast well enough to give you a real pledge. In that case the bank's credibility is at stake. But, if forward guidance is a conditional statement, then it's not much in the way of guidance. Is it? For how long have economists been the butt of jokes for saying on one hand...but then again on the other? How could this tactic now become a respected policy option for central banks and be regarded as a new tool? In the real world central banks have fouled up their ability to communicate because they want us to see their forward guidance as something that they can use and that 'we' can 'rely upon,' while, at the same time, preserving their flexibility to change the policy that they have announced for the future- the very same policy from which they want us to take guidance! No wonder central bank communication has run amok.

I don't recall the chapter in monetary theory about central banks having their cake and eating it too, but perhaps I missed something when I was in graduate school.

The revival of GDP growth for EMU is certainly a positive development. But as the early returns from the Monetary Union demonstrate, the weighted average application to the local growth rates may provide a positive thrust to Monetary Union growth in the quarter but there are still countries that are lagging behind -- and these are the countries that are the flies in the ointment for lasting recovery. In addition, we can wonder if France is going to have the staying power to continue to grow given that it has a badly neglected its fiscal situation to date.

The PMI measures have been signaling that a turning point is on its way for GDP. The emergence of growth has been well heralded. But the future of, and the continuation of, positive GDP growth rates still has issues.

Policymakers in the US may conclude that the time is ripe to cut back on quantitative easing stimulus because there is a pickup in Europe, judging that the potential for European unraveling has lessened. While that conclusion about Europe may be true for the moment (nanosecond), it is not clear to me (at least) how much staying power EMU has.

Nor is it clear to me that the world economy has, in any broad sense, picked up or improved. Globally export and import growth rates are still pretty weak. The Baltic dry index is barely stirring. And in a very topical July export-import price report, US nonagricultural export prices have taken on more downward momentum as have US nonpetroleum import prices. Neither of those developments would be expected if the demand for US exports or imports were picking up.

While I don't view the emergence of European growth as a wholly a technical matter born by the application of an idiosyncratic weighting system applied to various national GDP growth rates, the variability of growth that still exists within the Monetary Union is a factor not to be ignored. One of the factors that was responsible for tearing apart the Monetary Union in the first place was that the various members of the Union for long periods of time ran persistently different inflation rates, leading to huge gaps in competitiveness among fellow union members. Similarly, these differences in growth rates - which are still pretty large - need to fall into line. It still is a question as to whether or not the German or French economies which are growing faster will provide any positive impact to the Monetary Union apart from the weighted average applied to their individual national growth rates. Germany tends to post export led growth. That's not going to help the rest of the Union grow. France has delayed its fiscal adjustment. So while we see the European Union's two largest economies leading the parade we have yet to conclude that the rest of the parade is going to follow their lead since neither has much in the way of coat-tails. And if the rest of EMU doesn't follow that could be quite embarrassing.

To that point: Using just the six countries in the table, the average gap of each with the EMU area growth rate has been persistently large in this period --especially after Q4-2010. During this period the average gap between the annual growth rates of each of these six countries and the EMU pace has ranked in the top one fifth of all such growth gaps for this group back to 1996. With the emergence of growth in 2013-Q2 the average growth gap rank worsened, rising to the top 25th percentile from the top 32nd percentile in Q1. It is the persistence of a growth gap that is worrisome and that suggests that whatever EMU is reporting as growth might not be a representative number for the union as a whole. And such persisting internal divergences could be quite problematic from the standpoint of reaching a lasting recovery.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief