Global| Mar 30 2010

Global| Mar 30 2010Is Japan Completing Its Transition To Growth From Recession?

Summary

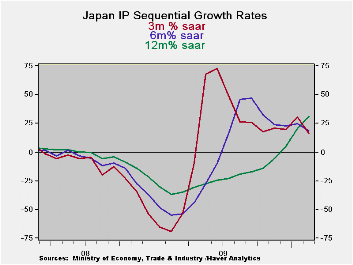

Despite the month’s sharp drop in output, the chart of Japan’s sequential growth rates is a very encouraging picture of an economy in transition. Still it offers no iron-clad promise for the future. The chart shows the drop of IP into [...]

Despite the month’s sharp drop in output, the chart of Japan’s sequential growth rates is a very encouraging picture of an economy in transition. Still it offers no iron-clad promise for the future. The chart shows the drop of IP into recession. Of course the various lines on the chart drop sequentially with the shortest growth rate going down first (3-Mo) then the six-month rate and finally the Yr/Yr rate. Of course the shortest period growth rate makes the largest swings as well and we see that carried into recovery, there is a nice symmetry between the lows and thighs of the 3-month and six mo growth rates. The Yr/Yr rate is still rising.

After the clear recession gyration to new growth rate lows and new growth rate highs, the various growth rate series have settled down to a steady growth path at 25%- still too strong to be sustainable. In the current month we see that path ratcheting a bit lower. Still the six- and three-month growth rates are fairly steady and the Yr/Yr pace is still rising.

As I said at the start there is nothing in this a pattern that assures a soft landing ahead. But the behavior in the indices is just what you would want and expect from a sold recovery that develops after a downturn. Japan still needs to slow its year-over-year advance to something that is more sustainable. And, beyond the numbers, Japan needs to spread the recovery beyond its export sector.

The table shows us that for all the gyrations in IP overall IP is still just 82.9% of its cycle peak. Its transportation output is about 25% below its cycle peak. Investment goods lag the most at only 73.7% of their cycle peak while electric and gas output is closest to full recovery at nearly 95% of its peak level of output in this cycle.

In the current quarter, despite the sharp drop in output in February, IP is still growing in excess of 20 percent annual rates for the headline series. Consumer goods, textiles and mining are the weak sectors in the unfolding quarter-to-date. Auto output has been strong but we may see a shift there due to the problems at Toyota. Still Japan is putting up a very good profile despite the drop in IP in February.

| Japan Industrial Production Trends | |||||||||

|---|---|---|---|---|---|---|---|---|---|

| m/m % | Saar % | Yr/Yr | Qtr-2-Date % AR |

%of Cycle Peak |

|||||

| Seas Adjusted | Feb-10 | Jan-10 | Dec-09 | 3-mo | 6-mo | 12-mo | Yr-Ago | ||

| Mining & MFG | -0.9% | 2.7% | 1.9% | 15.9% | 18.4% | 31.4% | -36.9% | 22.3% | 82.9% |

| Total Industry | -1.1% | 3.1% | 1.7% | 15.8% | 18.0% | 29.8% | -35.7% | 23.2% | 83.5% |

| MFG | -0.9% | 2.6% | 1.9% | 15.4% | 18.2% | 31.2% | -36.9% | 21.7% | 82.8% |

| Textiles | -4.1% | 1.9% | -0.9% | -11.9% | -1.5% | -4.9% | -20.8% | -4.2% | 70.6% |

| T-port | -2.0% | 5.9% | -2.9% | 3.0% | 41.3% | 91.0% | -60.0% | 26.9% | 76.2% |

| Product Group | |||||||||

| Consumer Gds | -2.7% | 2.7% | -0.7% | -3.3% | 2.6% | 22.9% | -30.5% | 6.6% | 85.3% |

| Intermediate Gds | -0.7% | 3.2% | 1.3% | 16.2% | 20.3% | 46.3% | -41.9% | 24.0% | 84.5% |

| Investment Gds | 2.0% | 2.3% | 1.2% | 24.2% | 30.9% | 11.8% | -32.5% | 28.8% | 73.7% |

| Mining | 1.5% | 1.3% | 2.6% | 23.7% | -3.1% | -1.6% | -6.5% | 9.5% | 87.3% |

| Electric&Gas | 0.9% | 1.6% | 0.5% | 12.4% | 21.6% | 8.1% | -12.2% | 16.3% | 94.9% |

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief