Global| Sep 05 2019

Global| Sep 05 2019Is Germany Set to Take a Tumble?

Summary

The German condition German orders have been declining long enough and the decline has been substantial enough that talk of a German recession has emerged. This month's report will not put a stop to it. The government has spoken of a [...]

The German condition

The German condition

German orders have been declining long enough and the decline has been substantial enough that talk of a German recession has emerged. This month's report will not put a stop to it. The government has spoken of a willingness to engage in fiscal stimulus were that to happen, but no one is expecting all that much from Germany where fiscal probity and budget surpluses have been the focus of policy. Germany has even fought against demands for it to spend 2% of GDP on its own defense as NATO has been demanding by saying that it can't afford it. This is from a country running a budget surplus. Any deviation from the budget surplus path even to try to soften the blow of recession will be modest. Moreover, Germany depends importantly on demand conditions abroad for its stimulus because its export sector is so large. Reigniting German growth using domestic stimulus, if the real problem is slack demand from overseas, simply is not going to be very fruitful.

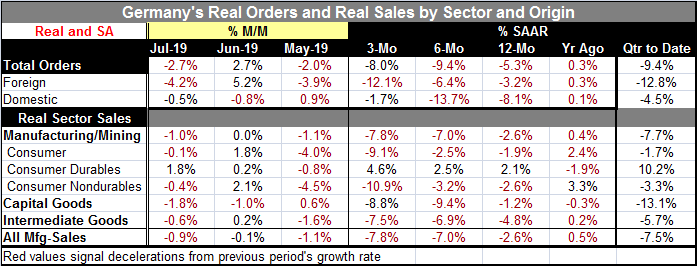

German orders fell by 2.7% in July, wiping out the whole of the gain made in June. Overall orders are lower by 5.3% over 12 months, led by an 8.1% year-on-year drop in domestic orders. For now the chief source of weakness is domestic orders. But foreign orders are down by 3.2% over 12 months and falling faster than domestic orders over three months. Foreign orders show ongoing secular deterioration in their growth rates. Domestic order weakness has taken a ‘breather' with orders falling only at a -1.7% pace over three months compared to a -12.1% pace of decline for foreign orders.

Quarter-to-date

In the quarter to date, orders are falling sharply overall. Domestic-sourced orders are falling with the lead weakness coming from the external sector early in Q3.

Real sales by sector

Real sector sales show sequential deterioration more or less across the board but with two notable exceptions. Overall sales fall at a 2.6% annual rate over 12 months, at a 7% pace over six months and at a 7.8% pace over three months- a clear deteriorating progression of contraction. Yet, spending on consumer durables is contrarily showing secular acceleration with the pace of sales rising from 2.1% over 12 months to 2.5% over six months and to 4.6% over three months! That is quite an island of strength in a sea of order futility. Capital goods show a minor exception to progressive deterioration as the three-month growth rate at -8.8% is technically less weak than the six-month pace at -9.4% even though it is substantially weaker than its -1.2% 12-month pace. And even though the -8.8% drop is severe, it does technically break the pattern of progressive deterioration…but not the spirt of it.

Germany and the ECB

The weakness in German real sector sales and real orders is clear. The trend is clear. The degree of weakness is undeniable and this is for Europe's largest economy. Oddly, it is also from the EMU country that is asking the least for any added ECB stimulus. Germany is willing to take its lumps and is not willing to sacrifice any monetary probity to lessen the impact of recession. While German and EMU-wide inflation continues to run at a pace under its target rate, Germans are uncomfortable with the ECB's negative rate policy. Incoming ECB president Christine Lagarde has pledged to look at the effectiveness of negative rates once she takes the reins of the ECB. Germany is a country that makes policy for the long run and does not like cyclical deviations.

The economy does not sink by weak orders alone

Yesterday Germany also reported the largest drop in retail sales in the last seven months. That weakness might suggest that manufacturing weakness is beginning to spread in the economy. The IFO survey shows that weakness has encroached across sectors. German construction activity has been surprisingly resilient in this process but today the IHS Markit German construction PMI fell to a five-year low as the diffusion reading fell sharply to 46.3 in August from 49.5 in July. Instead of showing a minor decline in output, it now signals a more substantial decline. The wheels seem to be coming off the German growth wagon and not just in the factory sector.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief