Global| Feb 22 2016

Global| Feb 22 2016Is EMU Weakness a True Drop or Part of Sideways Volatility?

Summary

The Markit private sector readings for manufacturing and services backed off in the EMU as well as in Germany and France in February. EMU-wide both manufacturing and services weakened. Both sectors weakened in Germany. France's [...]

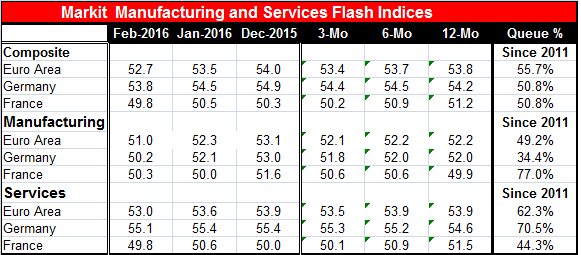

The Markit private sector readings for manufacturing and services backed off in the EMU as well as in Germany and France in February. EMU-wide both manufacturing and services weakened. Both sectors weakened in Germany. France's manufacturing improved, staying close to the value of 50; however, the French services sector fell slightly below 50, indicating contraction. The slippage and weakness in February is real and widespread, and in a few cases, pronounced.

The Markit private sector readings for manufacturing and services backed off in the EMU as well as in Germany and France in February. EMU-wide both manufacturing and services weakened. Both sectors weakened in Germany. France's manufacturing improved, staying close to the value of 50; however, the French services sector fell slightly below 50, indicating contraction. The slippage and weakness in February is real and widespread, and in a few cases, pronounced.

Stability or Tipping Point?

The German composite index does not change much over its three-month, six-month and 12-month averages. However, for the EMU, the private sector averages are slipping steadily. The EMU slippage is most recent coming in the three-month average and in February. Slippage is slow for the most part and may simply be part of a broader sideways movement. While both EMU-sector series have fallen off recently, both could also still be construed to be in a longer uptrend. This distinction will become more apparent as we move forward and see if the indices return to trend and move up or break down and decline. We may be on the cusp of a tipping point. For the moment, global forces still appear to be weakening although markets may be gaining some footing late in February.

There is not much afoot in terms of additional helpful monetary stimulus (how could there be you may ask.) and virtually nothing in terms of fiscal stimulus- apart from somewhat greater spending to house migrants in Europe, especially in Germany. But with Macedonia closing its borders, there appears to be a move to stopper the migration. Trapping them in Greece hardly seems like a plan to deal with them. Also it pushes all of the responsibility onto the Greeks who are ill able to deal with it.

EMU Trends

The EMU-wide manufacturing reading is stable across its average and really quite steady at a very weak level until February when it falls from 52.3 in January to 51.0 in February. It is now last weaker in January 2015. And the manufacturing sector reading for the EMU sits in the 49th percentile of its historic queue of data since 2011, below its median for this period. The EMU services reading slipped, falling more moderately but for the third consecutive month. The services weakness only really began over the last three months or so as you can see from the moving averages. The standing of the sector is at its 62nd percentile, a very moderate standing and hardly a counterweight to its weak manufacturing counterpart.

German Trends

Germany shows a weaker composite index for three months running, with manufacturing weaker for two months running. Germany's moving averages for manufacturing have been quite stable, if low, but manufacturing weakened relatively sharply in February. Manufacturing has an extremely weak 34th percentile standing against a 70th percentile standing for services- sharp divergence. Germany's services sector also fell off unexpectedly in February after showing moving averages that had been slightly gaining momentum up until that point.

French Trends

France shows a drop in its composite below 50 with manufacturing gaining a bit and services driving the move weaker with a diffusion reading below 50 showing contraction in February. The French composite trend has been eroding. Manufacturing's trend has been firming ever so slightly and services have been driving the ongoing slippage. Like Germany, France shows sector contrariness in its standings. Manufacturing is in its 77th percentile while French services are in their 44th percentile.

Trend Assessment

The monthly drop offs in manufacturing in February for Germany and for EMU are some of the steepest we have seen since early 2011. While the drop offs in services are generally larger than average, they are not as severe. But all this raises questions about the future.

Broader Issues

Europe is still fighting over migrant issues with Macedonia taking steps that could choke off the flow of migrants inland and strand them in Greece. This effectively pushes the problem onto Athens- as if it needed any further challenges. In the U.S., the Federal Reserve is finding ways to diminish the threat of weakness from abroad as well as its encroaching impact on U.S. statistics. Over the last two weeks, the average U.S. economic indicator showed a level or growth rate that stood them only in the 25th percentile of their respective historic ranges making recent general U.S. economic indicators weaker than those posted above for the EMU.

Data Show Change; Policy Shows Stasis

Make no mistake about it. Change is afoot. Policymakers are making choices and there are ramifications. For today much of the market focus is on oil and some recent IEA statements. But the IEA is only talking about general trends not really giving any news while the economic reports bring news. In any event, the IEA's commentary has boosted the oil price near-term even though its own conclusion is that there is not good case for any substantial boost in price and on its own assessment that into 2017 U.S. production will be rising. In the meanwhile, market forces may be leaving the frackers out to dry. But the fracking capability will remain even if on the sidelines and will always be ready to press back into service if oil prices were to rise, thereby acting as a limiting force to future gains. There is not credible news of any further production cutback or freeze deals. Markets are jumping from hither to yon to find some good news for price - that is not price discovery by the way. That sort of selective analysis can be dangerous. But it is being practiced in markets, at the Fed in the U.S. and in Europe. Where has all the objectivity gone? Beware of market priced for perfection or fantasy.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief