Global| Jul 15 2019

Global| Jul 15 2019Ireland Posts a Larger Trade Surplus

Summary

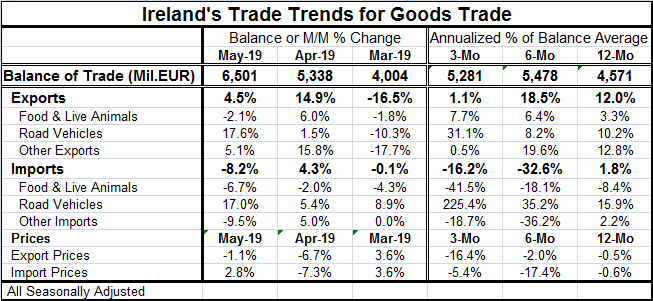

Irish exports and imports both have decelerated sharply from their respective paces of early-2018. Both have posted relatively recent year-on-year growth rates that have dipped below zero. However, as of May, it is exports where [...]

Irish exports and imports both have decelerated sharply from their respective paces of early-2018. Both have posted relatively recent year-on-year growth rates that have dipped below zero. However, as of May, it is exports where growth is holding on better with a 12% growth rate year-on-year compared to a thin 1.8% pace for imports. In the short span since 2014 in the chart shows Irish trade has been through several ‘boom-bust' cycles. The current phase is a deceleration following a boom.

Irish exports and imports both have decelerated sharply from their respective paces of early-2018. Both have posted relatively recent year-on-year growth rates that have dipped below zero. However, as of May, it is exports where growth is holding on better with a 12% growth rate year-on-year compared to a thin 1.8% pace for imports. In the short span since 2014 in the chart shows Irish trade has been through several ‘boom-bust' cycles. The current phase is a deceleration following a boom.

The trade flows are volatile and not the least of it because of prices. Oil prices have been gyrating globally and global trade flows have been impacted by trade wars and other posturing as well as economic sanctions. It is much harder to look at trade flows these days and to solidly know what they are telling you.

Both exports and imports show road vehicle trade flows to have accelerated from 12-months to six-months to three-months. Food and live animal imports have been contracting while exports have slightly increased. Other exports show a clear step down in growth over three months compared to their six-month pace and 12-month pace. Other imports are contracting over three months but not as fast as they do over six months.

Ireland is importing and exporting deflation. Both export and import prices are falling on all horizons. Export prices demonstrate an accelerating tendency to decline while import trends are not as linear but even they show weaker prices over three months than over 12 months.

Smoothed real export and import flows echo the nominal picture on trade showing a slowdown. But the smoothed real data show more slowing in exports and slightly less in imports, the opposite from the nominal trend. Exports when smoothed slow to a 5.1% pace while imports slow to 8.6%.

Of course, Ireland's trade flows are impacted by all the real world trends, including whatever Brexit uncertainty is doing to trade flows in the region. Globally, trade flows are slowing. China just issued its weakest GDP growth since 1992.

Irish trade flows actually look pretty good given the economic forces playing out in Ireland and globally. Irish industrial production in manufacturing has been showing regular gains, but that can be a very volatile series. In fact, the Irish manufacturing PMI gauge for June continues to sag and to record a level near to 50, indicating a very weak expansion. Irish consumer confidence is still relatively robust, but it has been sliding in 2019. Amid these trends, the strength in imports is somewhat surprising. The weakness in export and import prices, however, is borne out by still tepid CPI prices. Although the CPI and its core have been accelerating, the acceleration is still very mild and the inflation rate is still short of 2%. PPI prices in Ireland are weak and demonstrate sagging momentum. Through all of that, the services sector continues to be relatively firm but still in the context of an extended slowing that has been in slow progress since early-2016.

On balance, Ireland's trade is performing relatively well in what is still a difficult global environment. Domestic demand is holding up although there are indicators of mixed to slowing trends there. Ireland manufacturing is in the same slowdown-to-slump mode as the rest of the global economy. But exports and imports continue to grow in real terms and Irish domestic as well as export and import prices continue to tell a story of repressed inflation.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief