Global| Jul 26 2017

Global| Jul 26 2017INSEE Industrial and Services Climate Readings Flat-Line

Summary

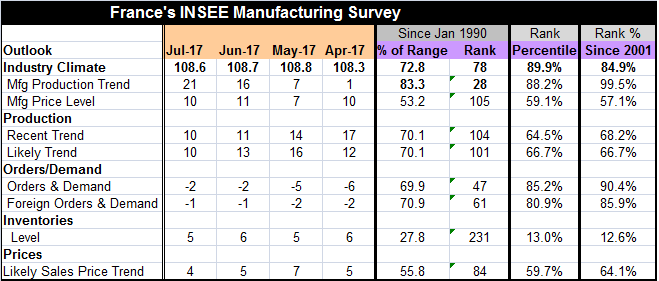

The French industrial climate gauge has barely moved over the last four months. The gauge sits at a relatively elevated level at the 84th percentile of its ranked queue of data since 2001 (or 89th percentile since 1990). The [...]

The French industrial climate gauge has barely moved over the last four months. The gauge sits at a relatively elevated level at the 84th percentile of its ranked queue of data since 2001 (or 89th percentile since 1990).

The French industrial climate gauge has barely moved over the last four months. The gauge sits at a relatively elevated level at the 84th percentile of its ranked queue of data since 2001 (or 89th percentile since 1990).

The production trend in manufacturing is at its highest point since 2001 and it has been zooming higher over the last three months, in the wake of the conclusion of the French elections. However, in marked contrast, the past is not prologue. The recent production trend sits only at its 68th percentile and its diffusion reading has withered over the last four months from a peak of 17 in April to 10 in July. The likely trend also is lacking. While it did perk up from April to May, it is back lower on balance in July and at a 66th percentile standing only on the border of the top third of all observations since 2001.

Total and foreign orders and demand have net negative diffusion scores, but that is misleading since they usually log negative scores. Total orders and demand have improved from a -16 reading in August of last year to a -2 reading in July and post a 90th percentile queue standing. This series is stronger only 10% of the time. Similarly, foreign orders and demand that were logging a -11 reading in September of last year are at a barely negative minus-one in July to register a strong 85th percentile queue standing. The inventory reading has been steady and remains at a low ranking and the likely price trend is also stable at a moderate reading with a 64th percentile standing historically. On balance, the French manufacturing sector appears to have had a hot run and is now marking time.

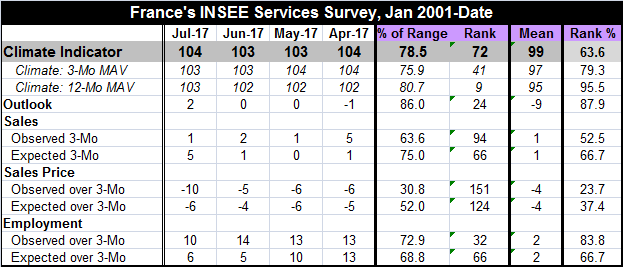

On the services side of the economy, the climate ranking is low, the three-month indicator is somewhat stronger and the 12-month moving average indicator is also stronger. This tells us that like the industrial sector the services sector had been hot and has since cooled off. But both the climate indicators and their three-month average are relatively stable. The outlook has improved from a range of flat to a -1 in the April-June period, to 2 in July and that reading logs an 87th percentile standing.

The observed three-month sales trend has been withering from 5 in April to 1 in July but the expected path is on the reverse upswing from a +1 rise in April to a +5 reading in July. Both series have middling standings with the observed path at a 52nd percentile standing and the expected path at a stronger 66th percentile standing.

Observed and expected sales prices both carry negative values and the two series are flat to weak with the observed trend weaker in a 23rd percentile rank and with the expected series at a still-weak 37th percentile standing.

Observed and expected employment trends have weakened over the past four months. The observed path has an 83rd percentile standing and the expected path is at a weaker 66th percentile standing.

The Markit PMI data on the manufacturing and services sectors in France have been signaling an uptrend for over the past year. Recently, the French PMI signals have stopped rising and moved more or less sideways confirming the signals in today's reports from INSEE.

The PMI data show a much stronger services sector than does the INSEE survey. Still, there is a lot in the PMI and the INSEE frameworks that seem the same. France has undergone a substantial improvement in its economy over the past year. It is now on an inflection point and we must wait to see if the progress will continue, be maintained or back track. Today's report is unclear in that regard. But there is some clear softness in the recent services and manufacturing surveys.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief