Global| Jun 09 2005

Global| Jun 09 2005Initial Unemployment Insurance Claims Back Down

by:Tom Moeller

|in:Economy in Brief

Summary

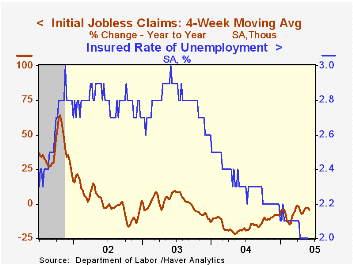

Initial claims for unemployment insurance fell 21,000 to 330,000 last week and reversed most of the prior period's slightly revised jump. Consensus expectations had been for 335,000 claims. During the last ten years there has been a [...]

Initial claims for unemployment insurance fell 21,000 to 330,000 last week and reversed most of the prior period's slightly revised jump. Consensus expectations had been for 335,000 claims.

During the last ten years there has been a (negative) 75% correlation between the level of initial claims for unemployment insurance and the monthly change in payroll employment. There has been a (negative) 65% correlation with the level of continuing claims.

The four week moving average of initial claims fell to 331,750 (-4.2% y/y).

Continuing claims for unemployment insurance fell 4,000 following a downwardly revised gain the prior week.

The insured unemployment rate remained stable at 2.0% for the seventh consecutive week.

Equilibrium Models of Personal Bankruptcy: A Survey from the Federal Reserve Bank of Richmond can be found here.

| Unemployment Insurance (000s) | 06/04/05 | 05/28/05 | Y/Y | 2004 | 2003 | 2002 |

|---|---|---|---|---|---|---|

| Initial Claims | 330 | 351 | -4.9% | 343 | 402 | 404 |

| Continuing Claims | -- | 2,588 | -10.3% | 2,926 | 3,531 | 3,570 |

by Carol Stone June 9, 2005

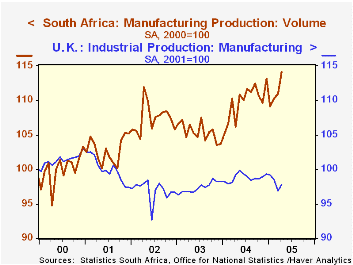

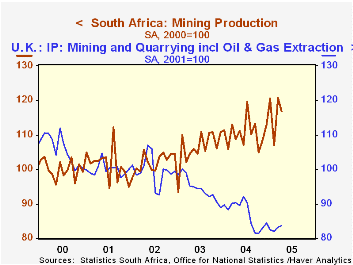

Industrial production picked up in the UK in April, rising 0.8%, the first increase since December. Metals, machinery, wood and paper products and electrical machinery were among the main movers in April's upturn. Beneficial to UK industry as this was, it still left production down 2.7% from a year ago. The manufacturing sector is also off by that amount and the mining sector, even more. Notably, among mining divisions, the energy sector has been lagging, while non-energy mining output is climbing. Year-on-year declines in the manufacturing sector are widespread, with output of textiles, paper, and electrical machinery all down at least 7%; thus, gains for all of these in April are gratifying, although that in textiles is quite small at 0.4%, month-on-month. Overall, the UK industrial sector appears hesitant, and with sluggishness in the industrial sector mirrored in employment and also most recent in a decline in new home construction starts.

South Africa also reported April production data today. That nation's industrial activity looks much healthier, with widespread uptrends in both factory and mining sectors. Output of manufactures is up vigorously, with a 2.8% month-on-month rise in April, capping a 7.1% yearly gain. The largest increases are in food, glass, motor vehicles and furniture. South Africa's mining sector saw a monthly decrease, but trends there are generally strong, with output of nearly every major mineral well above a year ago. Copper, for instance, has seen year-to-year increases the last two months, apparently ending a long decline. "Other" metals have risen 27% and diamonds, 33.5%. Only nickel and gold show year-over-year declines. Mining represents nearly a quarter of total industry in South Africa, compared with 14% in the UK.

| Industrial Production | Apr 2005 | Mar 2005 | Year Ago | 2004 | 2003 | 2002 |

|---|---|---|---|---|---|---|

| UK Total | 0.8 | -1.0 | -2.7 | 0.5 | -0.1 | -2.5 |

| Manufacturing | 0.9 | -1.6 | -2.7 | 1.4 | 0.5 | -3.1 |

| Mining | 0.6 | 1.3 | -5.8 | -7.8 | -5.3 | -0.3 |

| South Africa | -- | -- | -- | -- | -- | -- |

| Manufacturing | 2.8 | 0.7 | 7.1 | 4.3 | -1.9 | 4.5 |

| Mining | -3.2 | 12.9 | 7.1 | 3.9 | 4.0 | 0.8 |

| Mining ex Gold | -2.0 | 15.0 | 12.6 | 7.3 | 7.2 | 0.8 |

Tom Moeller

AuthorMore in Author Profile »Prior to joining Haver Analytics in 2000, Mr. Moeller worked as the Economist at Chancellor Capital Management from 1985 to 1999. There, he developed comprehensive economic forecasts and interpreted economic data for equity and fixed income portfolio managers. Also at Chancellor, Mr. Moeller worked as an equity analyst and was responsible for researching and rating companies in the economically sensitive automobile and housing industries for investment in Chancellor’s equity portfolio. Prior to joining Chancellor, Mr. Moeller was an Economist at Citibank from 1979 to 1984. He also analyzed pricing behavior in the metals industry for the Council on Wage and Price Stability in Washington, D.C. In 1999, Mr. Moeller received the award for most accurate forecast from the Forecasters' Club of New York. From 1990 to 1992 he was President of the New York Association for Business Economists. Mr. Moeller earned an M.B.A. in Finance from Fordham University, where he graduated in 1987. He holds a Bachelor of Arts in Economics from George Washington University.

More Economy in Brief