Global| Sep 08 2005

Global| Sep 08 2005Initial Claims for Unemployment Insurance Dipped

by:Tom Moeller

|in:Economy in Brief

Summary

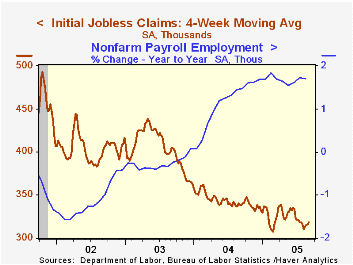

Initial claims for unemployment insurance dipped 1,000 last week to 319,000 from the prior week's unrevised level. Consensus expectations had been for a decline to 315,000. The figure included about 10,000 disaster-related [...]

Initial claims for unemployment insurance dipped 1,000 last week to 319,000 from the prior week's unrevised level. Consensus expectations had been for a decline to 315,000.

The figure included about 10,000 disaster-related applications from hurricane-battered Alabama, Louisiana and Mississippi, a number likely to surge in coming weeks.

The four-week moving average of initial claims rose to 318,500 (-6.0% y/y).

Continuing claims for unemployment insurance fell 5,000 in the latest week following a downwardly revised 27,000 increase the week prior.

The insured unemployment rate remained at its four-year low of 2.0% for the eighth consecutive week.

Analysis of the Economic & Budgetary Effects of Hurricane Katrina from the US Congressional Budget Office can be found here.

Consumption Taxes: Macroeconomic Effects and Policy Issues from the Federal Reserve Bank of Kansas City can be found here.

| Unemployment Insurance (000s) | 09/03/05 | 08/27/05 | Y/Y | 2004 | 2003 | 2002 |

|---|---|---|---|---|---|---|

| Initial Claims | 319 | 320 | -2.1% | 343 | 402 | 404 |

| Continuing Claims | -- | 2,593 | -9.6% | 2,926 | 3,531 | 3,570 |

by Tom Moeller September 8, 2005

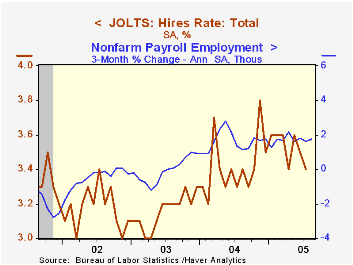

The Bureau of Labor Statistics reported that the job openings rate, from the Job Openings & Labor Turnover Survey (JOLTS), dipped in July to 2.6% from an upwardly revised June. The job openings rate is the number of job openings on the last business day of the month as a percent of total employment plus job openings. A 102,000 decline in the total number of job openings reversed about half of the prior month's rise but openings remained up 9.7% y/y.

The hires rate dipped slightly to 3.4% for the second consecutive monthly decline. The hires rate is the number of hires during the month divided by employment.

The job separations rate fell sharply to 3.1%, the lowest level since January 2004. Total separations include quits, layoffs, discharges, and other separations as well as retirements. The total separations, or turnover, rate is the total number of separations during the month divided by employment.

The survey dates only to December 2000 but has since followed the movement in nonfarm payrolls.

A description of the Jolts survey and the latest release from the U.S. Department of Labor is available here.

| JOLTS (Job Openings & Labor Turnover Survey) | July | June | July '04 | 2004 | 2003 | 2002 |

|---|---|---|---|---|---|---|

| Job Openings Rate: Total | 2.6% | 2.7% | 2.4% | 2.4% | 2.1% | 2.2% |

| Hires Rate: Total | 3.4% | 3.5% | 3.3% | 3.4% | 3.2% | 3.2% |

by Carol Stone September 8, 2005

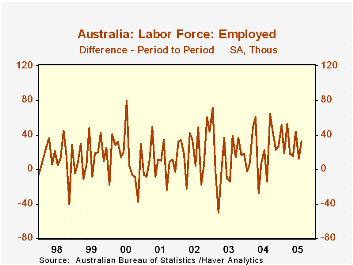

The Australian economy remains strong, as labor markets show favorable trends and GDP growth in Q2 was the best since late 2003. August's labor force survey included a gain in employment of 32,600, following July's 12,100. One forecast survey had expected the number of people employed to be flat in August. Indeed, a quick glance at the graph showing the monthly changes suggests that this would be a logical supposition: this current string of monthly increases is a long one, 12 months. Employment in Australia is characterized by a quite erratic monthly pattern, rather than the currently persisting increases. In fact, the length of this 12-month stretch has not been surpassed since 1980.

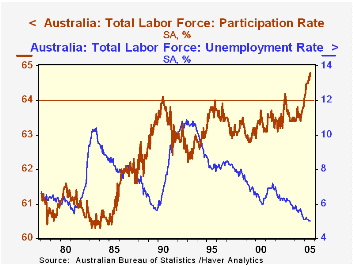

Other aspects of the data describe general strength in the labor market. Two months ago, we first saw the unemployment rate at 5%, a low for at least 28 years, and that has been maintained now for a third successive month. Further, the participation rate has hit another new high, 64.8%. Sometimes, a low unemployment rate only signals that people have withdrawn from the labor force, that they see few opportunities to work, so they reduce their participation. This is clearly not the case presently in Australia, with record participation, now also sustaining its current historic range for a third month; before this year, the proportion of the population working or wanting to work had only been more than 64% in five individual months since the inception of these data in February 1978.

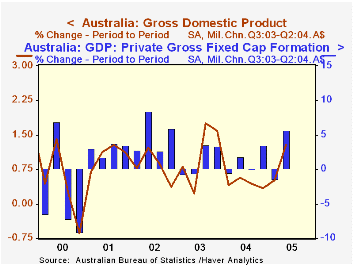

Australian GDP, reported yesterday (September 7) also showed this strength in Q2. At a 1.3% quarterly increase, it was marginally higher than forecasts, which called for 1.2%. Business investment rebounded after a Q1 decline, with both construction and machinery experiencing large increases. Exports accelerated after slowing somewhat in Q1, while import growth eased, so that the net export deficit was a much smaller drag on growth than it had been in Q1. Consumer spending expanded at about the same 0.8% pace as in Q1. The nation's economy continues to benefit from the growth in China and from the worldwide increases in commodity prices; the mining sector in particular is seeing vigorous growth, along with petroleum refining and processing of nonmetallic minerals. Finance and parts of the transportation sector are joining in the gains.

| Seasonally Adjusted | Aug 2005 | July 2005 | Aug 2004 | 2004 | 2003 | 2002 |

|---|---|---|---|---|---|---|

| Employed (thous) | 10067.5 | 10034.9 | 9664.3 | 9682.2 | 9481.4 | 9270.5 |

| Change (thous/%) | +32.6 | +12.1 | 4.2 | 2.1 | 2.3 | 2.0 |

| Unemployed (thous) | 529.9 | 524.8 | 527.0 | 566.9 | 610.9 | 636.1 |

| Unemployment Rate (%) | 5.0 | 5.0 | 5.7 | 5.5 | 6.1 | 6.4 |

| Participation Rate (%) | 64.8 | 64.6 | 63.4 | 63.6 | 63.6 | 63.4 |

Tom Moeller

AuthorMore in Author Profile »Prior to joining Haver Analytics in 2000, Mr. Moeller worked as the Economist at Chancellor Capital Management from 1985 to 1999. There, he developed comprehensive economic forecasts and interpreted economic data for equity and fixed income portfolio managers. Also at Chancellor, Mr. Moeller worked as an equity analyst and was responsible for researching and rating companies in the economically sensitive automobile and housing industries for investment in Chancellor’s equity portfolio. Prior to joining Chancellor, Mr. Moeller was an Economist at Citibank from 1979 to 1984. He also analyzed pricing behavior in the metals industry for the Council on Wage and Price Stability in Washington, D.C. In 1999, Mr. Moeller received the award for most accurate forecast from the Forecasters' Club of New York. From 1990 to 1992 he was President of the New York Association for Business Economists. Mr. Moeller earned an M.B.A. in Finance from Fordham University, where he graduated in 1987. He holds a Bachelor of Arts in Economics from George Washington University.

More Economy in Brief