Global| Feb 22 2017

Global| Feb 22 2017Inflation Up, Up and Away or Just 'Away'?

Summary

Both the U.S. inflation target rate (PCE) and the EMU target rate (HICP) are showing strong moves higher. Clearly inflation is on the rise...or is it really that simple? My prevarication in the face this quite overwhelming chart has [...]

Both the U.S. inflation target rate (PCE) and the EMU target rate (HICP) are showing strong moves higher. Clearly inflation is on the rise...or is it really that simple?

Both the U.S. inflation target rate (PCE) and the EMU target rate (HICP) are showing strong moves higher. Clearly inflation is on the rise...or is it really that simple?

My prevarication in the face this quite overwhelming chart has to do with the definition of WHAT inflation really is. It is two things that give us pause in assessing true inflation at a time like this. First of all, inflation is about THE price level which means the total price level. Second, it is about a continuing rise in prices.

Reason for prevarication or not?

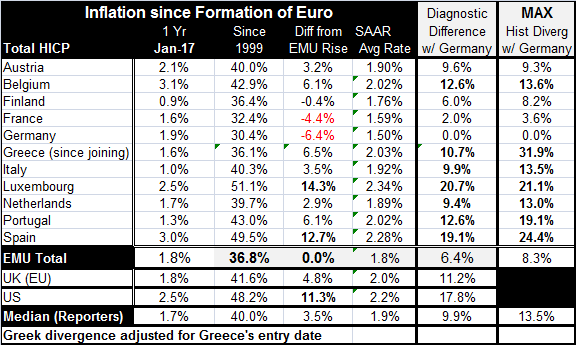

The problem that these aspects of inflation introduce is suggested by the table below that shows the progression of inflation as measured by the core HICP (HICP excluding select food and energy groups). Use of the core measure violates the notion of looking at the whole price level. But since the core shows little inflation acceleration, it raises the question about what in the headline represents price increases that are now and will continue to be 'ongoing.' What we have here is a debate about the issues of inflation being ongoing versus one of looking at the broadest price gauge or not.

The OPEC factor

Right now inflation is being boosted by ratcheting oil prices under the 'control' of an OPEC cartel (and friends) of suspect uniformity of purpose. While OPEC would like higher oil prices, each member must sacrifice some output to create scarcity to pressure prices higher. So there is a cost to this action. Moreover, as oil prices rise, that opens the door for the oil-shale and other 'higher-cost' producers especially in the U.S. to put their higher cost production oil back to market and that has been in progress as the (drilling) rig count in the U.S. has been steadily rising.

A policy that undermines itself: breaking bad

From this discussion, one thing to understand is that the more successful OPEC is in raising prices higher the more that a high price generates a countervailing flow of supply to undercut the OPEC objective of a higher price. That output, output that is piggybacking on OPEC austerity, may require further 'OPEC and friends' production cutbacks (since not all oil producers are 'friends'). In fact, as prices get higher, history shows that OPEC members have a habit of falling off the wagon of austerity to reap the dual joys of higher output and higher prices. That sort of thing is, of course, temporary as breaking ranks on output austerity (breaking bad we could call it) will eventually bring excessive oil flows to market and cause prices to soften or to crash.

The core rate as a diagnostic not as a target

The core inflation measure serves to remind us that rising oil prices are only transitory, lifting the price level once and shifting up the relative price of oil and not really creating inflation. For oil price increases to become inflation, other things have to happen. The central bank has to accommodate the rise in prices. Inflation expectations must embrace the notion that the rise in relative oil prices will alter inflation, then that rise could become a broader problem. The core rate is a kind of diagnostic for that. And for now, there is no reason to believe that oil is stoking inflation expectations. We do not see that in the core pace or in investor/consumer surveys.

OPEC's limited ambitions

As the oil pass-through to the price level is creating the appearance of inflation, the core shows little evidence of oil pass-through into other prices. On top of that, we have reason to be skeptical of OPEC's ultimate success and reason to see OPEC in any event with some limited ambition for what level it seeks as the right one for oil's price. OPEC does not want oil prices to rise indefinitely, at least not the Saudis who have long-term oil reserves. The Saudis are the ones making the largest sacrifice to get prices higher now. Saudi Arabia has oil for the long term and does not want energy prices so high that alternative fuels are too rapidly developed. But they have already stumbled over one such trip wire with oil-shale and tertiary production in the U.S. after letting prices soar to over $100 per barrel. That was a mistake. So we have every reason to look for OPEC ambitions to be limited and to view the headline inflation bulge as a temporary spike and not as lasting inflation in progress.

Oil stocks are still bloated

Global demand is still weak and our weekly anecdotal evidence tells us that oil stockpiles are still quite full. So far the cartel seems to have done little to make inroads to erode the oversupply as evidenced by oil stockpiles that are simply too high and much higher than what is normal.

The core evidence

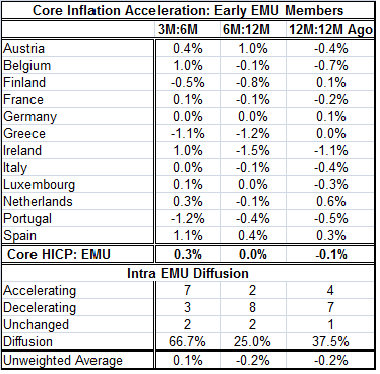

While the hike in oil prices and the impact on the headline inflation is relatively new, core inflation shows little sign of budging. In the EMU, the core HICP is seeing its seasonally adjusted annualized rate of inflation (SAAR) over three months as higher than its six-month rate by only 0.3% points. Its six-month rate (SAAR) is actually the same as its 12-month rate. And its 12-month rate (SAAR) is lower by 0.1% point than it was one year ago. This is not what inflation should look like. Clearly inflation is totally a reflection of the food and energy components of the HICP making it seem less likely that what we are seeing is real inflation (of the sort that will last). This diagnosis classifies the current price-push as relative price inflation, the kind that hits the headline and pushes up the price level 'once and for all' and then has little impact on other prices in the system.

ECB treatment

That is how the ECB is treating this surge in the headline. And for now, this approach seems to have strong merits. As a double check, we also look in the data in the second table the core inflation trends in the longest-standing EMU member countries. We find that over three months compared to six months, there is some inflation pick up. But that over six months compared to 12 months, inflation is mostly lower, not higher. And the 12-month pace compared to the 12-month pace of one year earlier finds that inflation is falling in more EMU member countries that it is rising.

Not inflation /no sustainable

This is not what true inflation should look like. If inflation is in gear, it should be manifest in most prices. But inflation is not in gear. And for all these reason we explained above, it is not likely to be sustained by the actions of the OPEC cartel. That is true for two reasons: (1) ever higher oil prices are not the cartels objective as well as, (2) because it is possible that the cartel will prove unstable and will be unable to achieve its more modest goal.

Policy

For now policy can treat this as a no-inflation situation. However, with the headline streaking, it is something that will have to be carefully watched. Some pick up in the core is still to be expected, however, and that is just to get inflation a bit closer to its 'a bit less than 2% goal.' As it is, EMU core inflation is still running at a pace below 1%. Among the 12 early EMU members in the table, the 12-month price rise is below 1% in seven of them. It is at or above 1.5% in only two of them (Belgium and Austria). Mario Draghi has his eye on these metrics as he chooses to bide his time and extend accommodative polices in the EMU. But other more critical eyes are also watching and just because core inflation is so well behaved do not expect all Europeans to finds that as the salve for their pinched inflation-wary nerves. The disagreements about how to act and how to deal with this rogue increase in headline inflation rate remains a contentious matter among ECB council members as well as among FOMC members an ocean's breadth away. Do not expect economists to agree on something as vital as this that gets to the very core of the doctrine of how to run monetary policy.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief