Global| Apr 14 2020

Global| Apr 14 2020Inflation Continues Tame in EMU; Finland's Prices Drop in March

Summary

I feature a chart of Finland's price index against Brent. It shows how the headline for Finland is very much on the same cycle as oil prices. However, despite a heralded oil price deal, oil prices today are falling again and the oil [...]

I feature a chart of Finland's price index against Brent. It shows how the headline for Finland is very much on the same cycle as oil prices.

I feature a chart of Finland's price index against Brent. It shows how the headline for Finland is very much on the same cycle as oil prices.

However, despite a heralded oil price deal, oil prices today are falling again and the oil market is in a state of substantial excess. It will take OPEC-plus some time to deal with the excesses oil in the market especially since the coronavirus reaction seems destined to keep growth on its heels for some time.

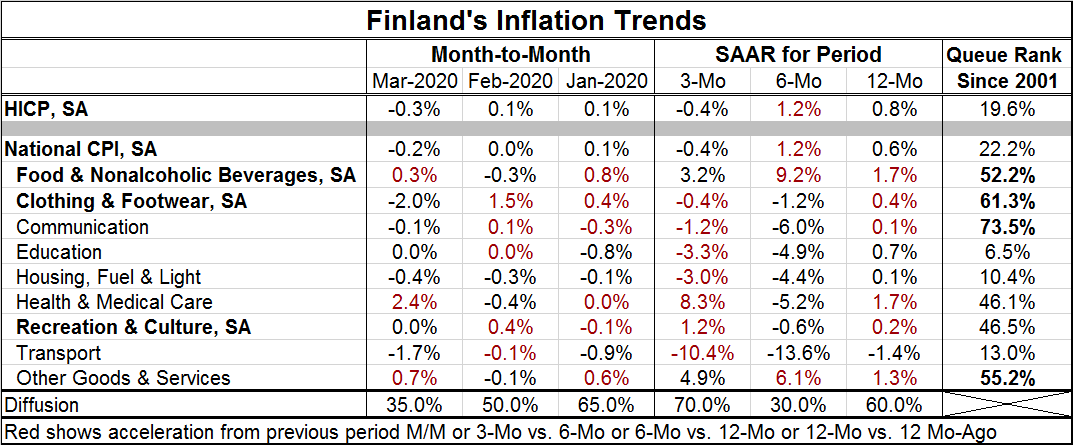

Finland shows some interesting price trend patterns. Inflation diffusion is very low in March, falling to a diffusion reading of 35%. Prices fell in March compared to February; the pace of price increases picked up in only three of nine sectors (plus the headline that is included the inflation diffusion calculation).

However, over three months, inflation diffusion is at 70% and rising sharply. But not all accelerations are created equal. Five categories plus the headline show prices falling on balance over three months. The acceleration reading comes from the fact that there were seven price declines on balance over six months and those declines were mostly deeper declines than the annual rates posted over three months. For example, transportation prices fell at a 10.4% annual rate over three months as of March, but that massive rate of decline is a deceleration compared to the 13.6% annual rate drop over six months.

The diffusion readings are useful and show the breadth of inflation and occasionally they will flag an odd result like that. But what we see is that inflation is modest across the recent months and also on a sequential basis from 12-months to six-months to three-months. The highest reading on sequential inflation is the 1.2% pace over six months. Monthly inflation is at +0.1% in each of the two prior months.

Lastly, we have inflation rankings for Finland that show the overall pace back to 2001 in the bottom 20% of its queue of monthly annualized rates of inflation- that is quite low. Food, clothing & footwear, communication, and other goods & services have above median readings on this timeline back to 2001. An above-median reading is one with a ranking above the 50% mark.

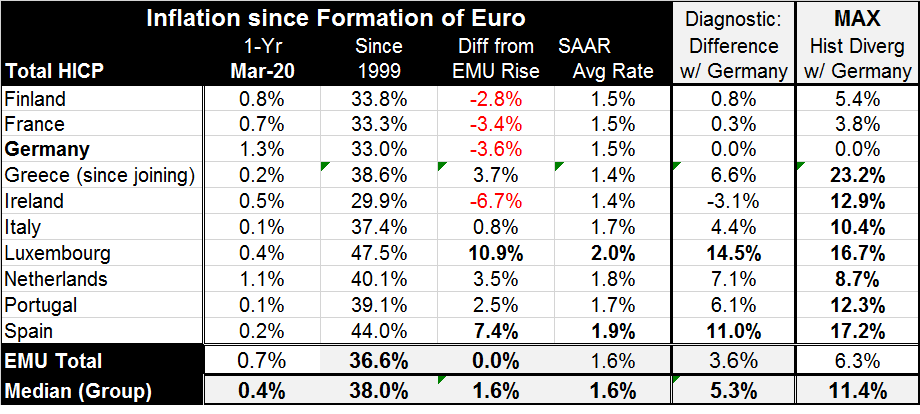

Inflation in the EMU echoes this good news with all early reporting members in the table showing inflation well below the ECB limit of 2%. In fact, only Germany and the Netherlands have inflation at or about the 2% pace.

Since the EMU was formed, only Ireland, Germany, France and Finland have kept their respective inflation rates consistently below that for the EMU as a whole. Finland is part of a special group of low-inflation EMU members.

However, the usual high inflation countries have really been keeping inflation in check. Spain, Portugal, Italy, and Greece on the month are the low inflation countries this month. Over five years, the lowest inflation countries are Greece, Ireland, Finland, and Italy. Over five years, the high inflation counties are Germany, the Netherlands, Luxembourg, and France. These are unusual groupings from an historic perspective. On balance, inflation is also tame in the EMU and holding well below the ECB's mandate to keep it below 2%.

Inflation in EMU

Inflation is low partly because of the oil glut and the oil glut stems substantially from the slow, induced pace that comes from trying to contain the coronavirus. The IMF has just cut its outlook for global growth to -3%. The finger on the pulse of trade measure known as the Baltic Dry goods Index remains low and flat. Markets today were trying to rally on China's export and import numbers that were not as bad as expected. But that is thin gruel for good news. At the same time, corporations' earnings reports are coming out and they are only the beginning of some bad news depending on the company and the industry and when a particular firm got caught up in the shutdown.

Between weak growth and the ongoing nature of weak growth, because fighting the virus requires that temperance be extended, a difficult picture of the oil market emerges as well as for all commodities. Countries are trying and planning to restart something more like normalcy, but how that is done, how fast it is done and how thoroughly it is done remains a contentious issue.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief