Global| Aug 06 2007

Global| Aug 06 2007Inflation Concerns are Forward Looking. Recent Trends Favorable

by:Tom Moeller

|in:Economy in Brief

Summary

For all of the concern about rising prices that recently has been expressed in Washington by the Federal Reserve Board, the most recent price trends are quite favorable. That's even excluding the recent decline in gasoline prices As [...]

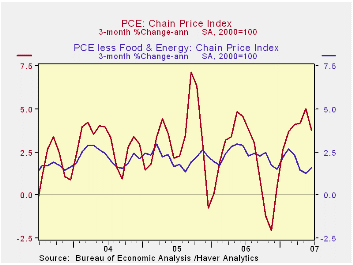

For all of the concern about rising prices that recently has been expressed in Washington by the Federal Reserve Board, the most recent price trends are quite favorable. That's even excluding the recent decline in gasoline prices

As on June, growth in the core (excluding food & energy) PCE chain price index has decelerated on a three month basis to 1.6% (1.9% y/y). Which is nearly half its growth rate a year ago.

Many attribute the good pricing news to the recently weak growth in GDP. Perhaps. But price inflation is first and foremost a monetary phenomenon, and the latest news comes at a time of strong growth in M2 (6.2% y/y) and MZM (8.4% y/y). Both those growth rates are roughly double the growth during last year which was up or double the growth during 2005.

Historically, the cash in one's pocket has mattered for pricing pressure as much as how fast the economy is growing. the Fed's vigilance of this is comforting.

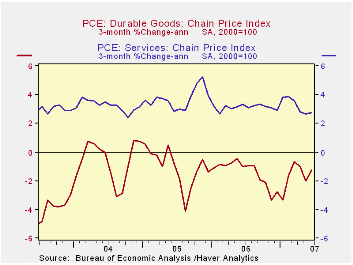

To follow is a review of recent pricing patterns. To the upside has of course been the recent pressure on prices for food & beverages (4.0% y/y), communication (-0.8% y/y) and personal care (3.1% y/y) led by faster growth in legal fees (5.1% y/y).

Easing price pressure is perhaps more pervasive. Growth in prices for durable goods are under downward pressure such as seen for prices of new vehicles (-1.0% y/y), household furniture (-0.8% y/y) and appliances (2.45 y/y).

Nondurables prices are showing easing price pressure as well in the apparel (-1.3% y/y) and shelter (3.7% y/y) areas.

To wrap up the areas where price pressure is easing are the medical care services (5.0% y/y), public transportation (-0.4% y/y), tenants & household insurance (0.6 y/y), and education (5.7% y/y), notably tuition.

The U.S. economy always has been one where some areas experiencing rising pressure are offset by areas of slack. That suggests that one is always at risk to focus on one and not the other. The cries of "depression" in the economy several years ago ignored the strength that was then being seen in housing and personal income, although these latter areas were growing at slower rates. It's never easy.

When Did Inflation Persistence Change? from the Federal Reserve Bank of Cleveland is available here.

Tom Moeller

AuthorMore in Author Profile »Prior to joining Haver Analytics in 2000, Mr. Moeller worked as the Economist at Chancellor Capital Management from 1985 to 1999. There, he developed comprehensive economic forecasts and interpreted economic data for equity and fixed income portfolio managers. Also at Chancellor, Mr. Moeller worked as an equity analyst and was responsible for researching and rating companies in the economically sensitive automobile and housing industries for investment in Chancellor’s equity portfolio. Prior to joining Chancellor, Mr. Moeller was an Economist at Citibank from 1979 to 1984. He also analyzed pricing behavior in the metals industry for the Council on Wage and Price Stability in Washington, D.C. In 1999, Mr. Moeller received the award for most accurate forecast from the Forecasters' Club of New York. From 1990 to 1992 he was President of the New York Association for Business Economists. Mr. Moeller earned an M.B.A. in Finance from Fordham University, where he graduated in 1987. He holds a Bachelor of Arts in Economics from George Washington University.

More Economy in Brief