Global| Sep 07 2005

Global| Sep 07 2005Industrial Production Gains in Europe: Can That Pattern Be Sustained?

Summary

Industrial production in Europe appears to be holding up well, according to data for four countries reported today for July. Month-to-month movements are a bit erratic, but trends are distinctly upward, nonetheless. As Louise Curley [...]

Industrial production in Europe appears to be holding up well, according to data for four countries reported today for July. Month-to-month movements are a bit erratic, but trends are distinctly upward, nonetheless.

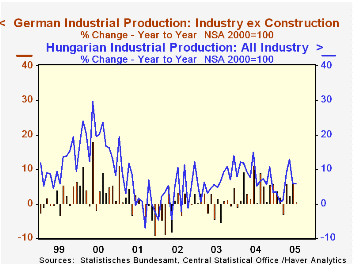

As Louise Curley explained here yesterday, Germany's manufacturing sector is growing, at least for the present. Her commentary on factory sales data cited their 3.8% gain in July. The production behind those sales was up 1.3%, with total industrial output (excluding construction) up 1.1%. This was the second marked increase in a row after a sluggish performance in the winter and spring. The July gains were widespread across individual industries, with only petroleum refining, machinery and electrical equipment experiencing declines; that in machinery followed spike in June.

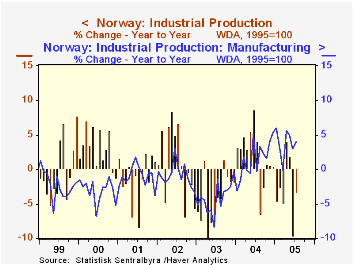

In Norway, total industrial production was up 1.1% in July after a drop of 6.2% in June. Oil and gas extraction dominates Norwegian industry; that sector rose after two sharp declines, and has been on an extended downtrend. By contrast, Norway's factories saw a small downtick in July, but prior increases have pushed their year-on-year performance to 4.0% growth, a pick-up after a small increase in 2004 and annual declines running all the way back through 1999.

In Hungary and Slovakia, modest increases in July followed declines in June, but year-on-year gains are substantial, at 5.8% and 4.7%, respectively. These countries' industrial sectors have been expanding vigorously for at least the last four years, and the gains in Hungary for one version of its index go back to 1993.

Thus, as we indicated at the beginning, European industry seems stronger than might have perhaps been expected, given the high level of the euro and the high level of energy prices. However, this latter factor in particular may yet become burdensome for these nations. Louise Curley also pointed out here yesterday that domestic new orders in Germany have already turned flat. So it remains to be seen how long the recent gains in European production can be sustained.

| Industrial Production* | July 2005 | June 2005 | Year/Year | 2004 | 2003 | 2002 |

|---|---|---|---|---|---|---|

| Germany | 1.1 | 1.4 | 0.6 | 3.0 | 0.4 | -1.0 |

| Norway | 1.1 | -6.2 | -3.4 | 2.0 | -4.1 | 0.9 |

| Oil & Gas Extraction | 1.2 | -9.5 | -5.7 | -1.5 | -1.7 | -1.5 |

| Manufacturing | -0.1 | 1.1 | 4.0 | 1.5 | -4.3 | -0.9 |

| Hungary | 1.2 | -1.6 | 5.8 | 8.4 | 6.6 | 3.3 |

| Slovakia | 0.2 | -0.5 | 4.7 | 4.2 | 5.0 | 6.4 |

Carol Stone, CBE

AuthorMore in Author Profile »Carol Stone, CBE came to Haver Analytics in 2003 following more than 35 years as a financial market economist at major Wall Street financial institutions, most especially Merrill Lynch and Nomura Securities. She had broad experience in analysis and forecasting of flow-of-funds accounts, the federal budget and Federal Reserve operations. At Nomura Securities, among other duties, she developed various indicator forecasting tools and edited a daily global publication produced in London and New York for readers in Tokyo. At Haver Analytics, Carol was a member of the Research Department, aiding database managers with research and documentation efforts, as well as posting commentary on select economic reports. In addition, she conducted Ways-of-the-World, a blog on economic issues for an Episcopal-Church-affiliated website, The Geranium Farm. During her career, Carol served as an officer of the Money Marketeers and the Downtown Economists Club. She had a PhD from NYU's Stern School of Business. She lived in Brooklyn, New York, and had a weekend home on Long Island.

More Economy in Brief