Global| Apr 13 2021

Global| Apr 13 2021Industrial Output in Italy and France and a Cursory ZEW Outlook

Summary

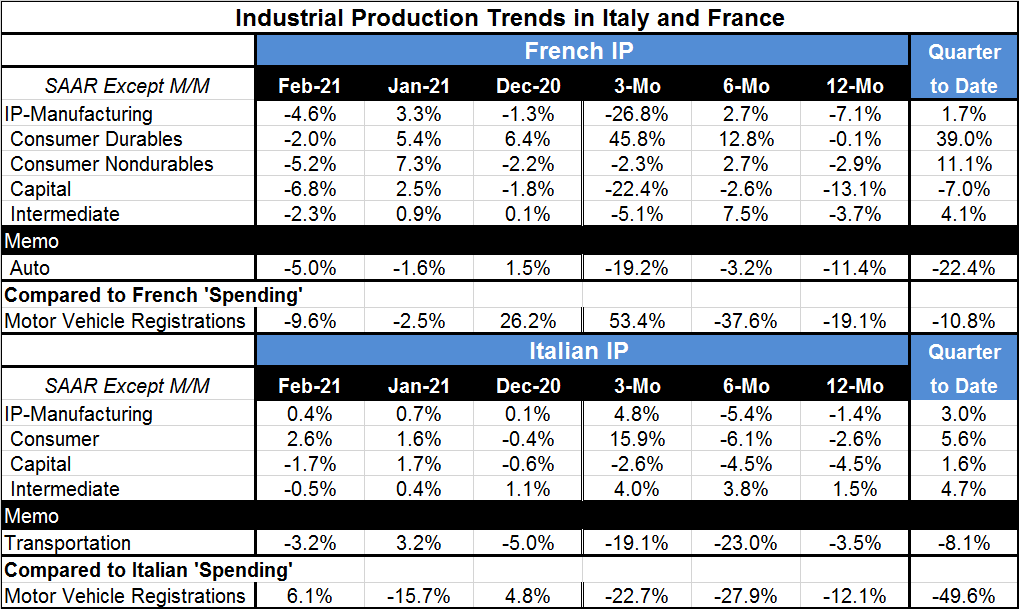

Italian Production Italian industrial output in manufacturing rose for the third month in a row. The three-month annualized gain at 4.8% is just about the mirror image of the six-month decline at 5.4%. Over 12 months, Italian IP is [...]

Italian Production

Italian Production

Italian industrial output in manufacturing rose for the third month in a row. The three-month annualized gain at 4.8% is just about the mirror image of the six-month decline at 5.4%. Over 12 months, Italian IP is lower by 1.4%.

Despite ongoing Covid-19 issues and the disruptions from forming a new government, Italy has managed to keep its industrial sector on an expansion path. Consumer goods output led manufacturing with an annualized rate rise of 15.9%. Capital goods output has fallen in two of the last three months and is falling at a 2.6% annualized pace over three months. Intermediate goods output fell in February but that was after four straight months of output increases; as a result of past strength intermediate goods output is rising over three months at a 4% annualized rate.

Among the three sectors only intermediate goods output is increasing on each of the three horizons in the table: 12-months, six-months and three-months. And that sector is even showing acceleration. In contrast, capital goods output declines on all three horizons though without any clear trend. Consumer goods output falls faster over six months than over 12 months then shows a strong gain over three months.

The transportation sector profile is ladened with negative numbers. The Italian manufacturing PMI has been making steady gains and has risen for three months running. The PMI shows manufacturing expanding (with values above 50%) for all months after June of last year.

On a quarter-to-date (QTD) basis, Italian IP shows all sectors expanding two months into Q1 2021. Output is led by the consumer sector with capital goods output as the laggard. Transportation sector output is still weak and declining.

French Production

While France and Italy are both Mediterranean countries, share geographical proximity and are the second and third largest countries in the euro area, respectively, they are riding out this coronavirus storm differently. The graph shows how similar IP growth was up to and during the Covid-19 crisis. But in the aftermath of the April Covid-19 disaster, Italian and French IP paths have diverged somewhat more.

French growth rates by sector are exaggerated compared to Italy's with IP in manufacturing falling over three months at a 26.8% annual rate in France compared to a solid rise in Italy's IP. While capital goods output in Italy is moving lower at a pace of 2.6% annualized over three months, France's capital goods sector is imploding at a 22.4% annual rate. Also, Italy's 4.0% gain in intermediate goods is contrasted with a 5.1% drop for IP annualized for France over three months.

In the quarter-to-date, conditions are a bit more similar with French output up at a 1.7% annual rate and intermediate goods output rising at a 4.1% pace, close to the pace of expansion in Italy. France, like Italy, has capital goods as the weakest sector in the QTD period, but for France that means the sector is contracting unlike for Italy.

Motor vehicle registrations in both Italy and France are falling in the quarter-to-date, but they are actually falling much faster in Italy than in France.

The year-on-year trends also tend to show more overall capital goods and intermediate goods weakness in France than in Italy.

The virus

The virus continues to be a factor in France and probably will be for much longer than anyone would like. The infection rate swept higher to a second peak in early-April but has since begun to recede. France's death rate curve has nudged higher but not by much. In Italy, the infection rate from the virus peaked in early-March but its run-off is slow. The death rate in Italy did rise but has been receding although doing so erratically. In Italy, some of the lockdown measures are being eased. In France, the IP weakness it encountered in February was unexpected and was a result of coronavirus lockdowns. France is still taking actions to try to protect itself. In view of the virulent outbreak in Brazil, France has suspended all flights from Brazil.

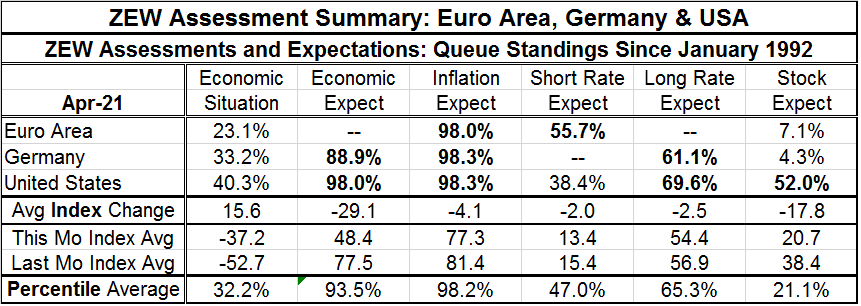

The outlook through the eyes of the ZEW experts

The virus continues to call the tune on output and to define how the economy is doing and how well it can do. Yet, everyone is optimistic on turning the corner, but we have not done that yet anywhere. The recently released and abridged ZEW survey presents the following picture.

ZEW only presents data for three areas: the euro area, Germany (the largest euro area economy) and the United States. We average the three or the relevant two (where applicable) to create some summary statistics in the table above. The current situation for April improves in the euro area, Germany and the U.S. The U.S. made a sharp improvement moving up from a -27.4 reading in March to +2.8 in April. The month-to-month U.S. change in current conditions is the largest monthly change and rise on data back to 2000. Germany made a strong gain too that is its 15th largest on that same timeline. However, with conditions on the ground improving expectations were set back on the month. The slippages were significantly large as well. Inflation expectations are still high-ranking, but they generally receded a bit on the month…as did expectations for short rates, long rates and stock markets. Economic expectations and inflation expectations are still very high-valued; long-term rate expectations have risen above their median (above a ranking of 50%); short-rate expectations are near their medians. The economic situation and stock market expectations are below their respective medians. The ZEW data speak of current improvement. Expectations are harder to read because as current conditions improve, expectations almost naturally are lowered especially when they start out as a very high readings near to the maximum possible. ZEW respondents are worried about inflation although those fears did not ratchet up this month. They are looking for more of a long-term rate response and they are not very bullish on stocks. There are some positive things here but also an abundance of caution and clearly some worry.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief