Global| Jan 27 2020

Global| Jan 27 2020IFO Expectations Are Set Back in January

Summary

IFO expectations fell to -5.2 in January from -3.1 in December when presented in its diffusion format. The expectations diffusion reading has an 11.6 percentile standing on data back to 1991 and has an ‘equally weak’ 10.2 percentile [...]

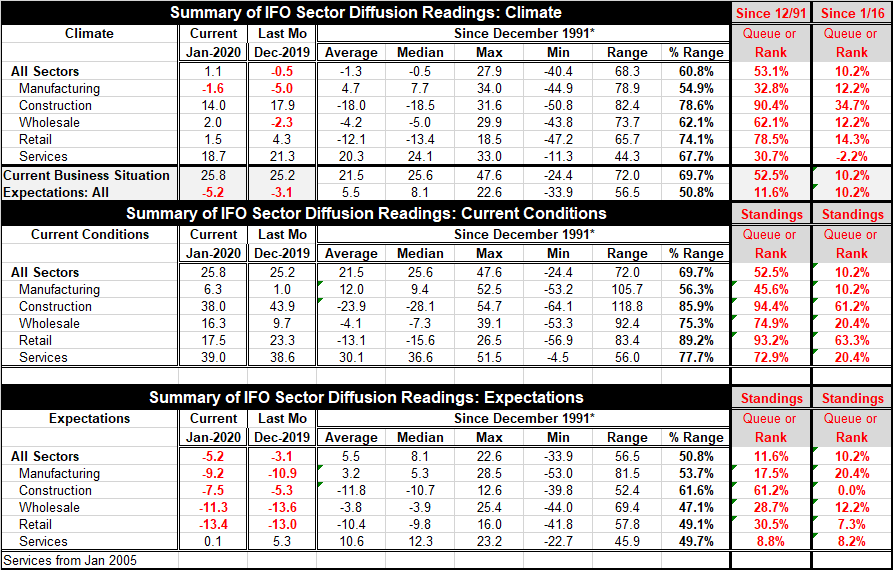

IFO expectations fell to -5.2 in January from -3.1 in December when presented in its diffusion format. The expectations diffusion reading has an 11.6 percentile standing on data back to 1991 and has an ‘equally weak’ 10.2 percentile standing on data back to January 2016. On both those timelines, German firms have had weaker expectations only about 10% of the time. That is not a positive development. German firms are entering 2020 with some skepticism about the outlook.

IFO expectations fell to -5.2 in January from -3.1 in December when presented in its diffusion format. The expectations diffusion reading has an 11.6 percentile standing on data back to 1991 and has an ‘equally weak’ 10.2 percentile standing on data back to January 2016. On both those timelines, German firms have had weaker expectations only about 10% of the time. That is not a positive development. German firms are entering 2020 with some skepticism about the outlook.

Current conditions, however, ticked higher in January with the all-sector index rising to 25.8 from December’s 25.2. That index has a Jekyll and Hyde standing of 52.5% (above its historic median) on data back to 1991 vs. a 10.2 percentile standing on data back to January 2016. The all-sector current reading is very weak by recent standards, but on a broader historic timeline the current standing is more or less ‘normal.’ The reading on climate gained to 1.1 in January on an all-sector basis from -0.5 in December. It also has a spit personality with a 53.1 percentile standing on data back to 1991 vs. a 10.2 percentile standing when compared to readings since January 2016.

The overview of the economy from the IFO respondents is that expectations are being held back and truly weak by both current and historic standards, while the actual performance of industries in ‘real time’ is on a shallow gradient three-month improving trend it is still weaker on balance over six months and 12 months despite the jump in manufacturing conditions in January. The report overall is the classic example of one-step forward two-steps back as sectors remain out of sync.

Current conditions by sector

Dissecting the report by sector, the drag is clearly emitted by one-sector, manufacturing. The manufacturing reading, which improved month-to-month in January, rose to 6.3 from December’s 1.0, a considerable rise. Still, on the long view, the manufacturing standing is below its median at its 45.6 percentile and is at a weak 10.2 percentile standing since 2016. In contrast, construction and retailing still have standings in their 90th percentiles on data back to 1991- and both also have lower but above-median standings in their 60th percentile range since 2016. Wholesaling and services each have current standings in their 70th percentile ranges over a long comparison compared to standings in their respective 20th percentile ranges since 2016. Current conditions set up manufacturing as the weak sector, services and wholesaling as moderate with retail and construction as strong. However, on the month the two strong sectors of retailing and construction each have taken a sizeable step backward while manufacturing and wholesaling each have taken a big step up along with some improvement in services. Out of sync remains the name of the game here.

Expectations by sector

Expectations show negative readings for four of five sectors as well as overall. In that sense, there is more uniformity among expectations than for current conditions. Services, the exception sector with a positive reading, barely goes over that bridge as its positive reading in January is only 0.1, as small as it can be and still be positive. Moreover, there is month-to-month weakness in all but two sectors: manufacturing and wholesaling, both of which made some exceptional improvement in January compared to December. Retailing erodes slightly on the month with larger deterioration reported by services and construction, especially services. The all-sector ranking for expectations is similar in both the long and short periods, but there are some considerable differences for some sectors. Construction has a 61.2 percentile (above median) standing over the long period compared to a zero percentile standing, the weakest of the lot, since January 2016. Wholesaling and retailing have expectations ranking around their respective 30th percentiles on the longer period that contrasts with a 12th percentile standing for wholesaling and a 7th percentile standing for retailing since 2016. However, services and manufacturing have very similar and weak readings on both long- and short-term metrics. Still, the month-to-month changes show no uniformity across sectors.

The bottom line

IFO survey participants show variation by sector. The results do not suggest that there is an economy-wide shifting of gears rather that sectors are still sorting things out or being sorted out by events. The weakness in expectations fell especially hard in January on services which might make it look like manufacturing weakness is spreading except that there was some significant manufacturing sector improvement in its current reading to balance that setback. Expectations in construction have seen a steady menu of setbacks over the last four months. The services sector is simply in flux as its monthly setback in expectations is an unexplained unwinding of an isolated jump in the index from one month ago. Current performance is moderate and mostly okay-to-strong across sectors with manufacturing as the outlier. Manufacturing is an outlier that showed sharp improvement in January for current conditions along with wholesaling. Naturally retailing and construction showed sharp backtracking in their current assessments to counterbalance those improvements. The bottom line is that the year is young. There are a lot of unexpected events. Sorting out continues in expectations as well as for current trends.

Beyond the bottom line

Sectors are still sorting out their trends. With the Coronavirus impact still having an unclear impact on the global economy, all bets are off on surveys conducted before participants knew of this latest risk. Concern over the virus spreading has hit oil, other commodity prices, and stocks hard; it has boosted bond prices, dropping yields back down after a period of yield escalation. So let’s be humble about extracting information from a survey whose participants may have a wholly different outlook on things one month from now. If they were cautious coming into the New Year, we can only wonder what the news of a virus spreading out of China will do their concerns next month.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief