Global| Nov 17 2006

Global| Nov 17 2006Housing Starts Plumb Six Year Low

by:Tom Moeller

|in:Economy in Brief

Summary

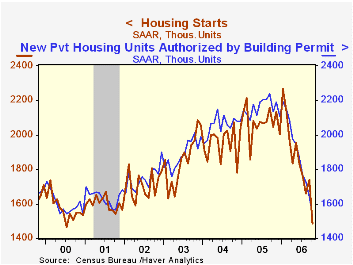

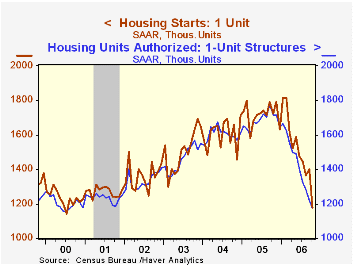

In October, housing starts more than retraced the downwardly revised 4.9% September gain and fell 14.6% to the lowest level since July 2000. The latest result fell well short of Consensus expectations for 1.68M starts. At 1.486M [...]

In October, housing starts more than retraced the downwardly revised 4.9% September gain and fell 14.6% to the lowest level since July 2000. The latest result fell well short of Consensus expectations for 1.68M starts.

At 1.486M units, the October figure pulled the year-to-date average to 1.863 starts and 10.2% below the first ten months of 2005.

Single-family starts in October fell 15.9% to 1.177M, also the lowest level since July 2000. The year-to-date average level of single family starts fell 11.5% from 2005. Multi family starts in addition were down by 9.1% m/m.

By region, single family housing starts were weakest down South and fell 24.8% (-32.4% y/y). Starts also fell 9.1% (-32.9% y/y) out West, were 7.3% (-33.1% y/y) lower in the Midwest but in the Northeast single family starts rose 10.9% (-22.2% y/y).

Building permits fell 6.3% after a revised 5.2% September drop. The ninth monthly decline this year was to the lowest level since 1997. Permits to start single family homes fell 3.8% (-31.7% y/y), the lowest since 2000.

What Do Financial Asset Prices Say About the Housing Market? from the Board of Governors of the Federal Reserve System can be found here.

| Housing Starts (000s, AR) | October | September | Y/Y | 2005 | 2004 | 2003 |

|---|---|---|---|---|---|---|

| Total | 1,486 | 1,740 | -27.4% | 2,073 | 1,950 | 1,854 |

| Single-family | 1,177 | 1,400 | -31.8% | 1,719 | 1,604 | 1,505 |

| Multi-family | 309 | 340 | -3.4% | 354 | 345 | 349 |

| Building Permits | 1,535 | 1,638 | -28.0% | 2,159 | 2,058 | 1,888 |

by Carol Stone November 17, 2006

Mexico's GDP is enjoying its best run of growth since before dot.com bust in 2001. In Q3, the year-on-year gain was 4.6%, following 5.5% and 4.7% in Q1 and Q2, respectively. The quarterly growth in Q3 was 1.0% from Q2, led by construction and transportation. Manufacturing edged up a mere 0.1% and didn't grow at all in Q2, but it had surged 2.9% in Q1 and is ahead 5.1% year-on-year. These data were reported yesterday afternoon, November 16, by INEGI, the Mexican government statistics institute.

Government officials, speaking prior to the G-20 Conference in Melbourne, Australia, indicated that this pattern was in line with their hopes. Their aim is to diminish the Mexican economy's dependency on demand from the US. So they are emphasizing local construction and services industries. The financial sector and other business services are up 4.6% year-on-year for Q3, the same as total GDP, but they have been expanding more rapidly than the total for most of the last five years. Finance Minister Gil Diaz highlighted the growth in construction, fueled in part by expansion of mortgage lending. Indeed, during the first half of this year, mortgage lending at banks was running more than 40% ahead of last year. Gross value added in construction is up 7.7% in Q3 from a year ago and 2.6% Q3/Q2 alone. Another strong sector is transportation, storage and communication, up 9.4% year-on-year. Mexico's output of oil is slowing, but its production of natural gas is growing rapidly, and we would surmise that pipeline usage is one part of the gain in the transportation sector.

| Mexico | Bil. New 1993 Pesos | Q3 2006 | Q2 2006 | Q1 2006 | Year Ago | 2005 | 2004 | 2003 |

|---|---|---|---|---|---|---|---|---|

| Real GDP | 1854.1 | 0.9 | 0.8 | 1.9 | 4.6 | 3.0 | 4.2 | 1.3 |

| Manufacturing | 330.0 | 0.1 | -0.0 | 2.9 | 5.1 | 1.2 | 4.0 | -1.3 |

| Construction | 73.8 | 2.6 | -0.1 | 2.1 | 7.7 | 3.3 | 6.1 | 3.3 |

| Transportation, Etc. | 236.4 | 1.8 | 1.5 | 4.1 | 9.4 | 7.1 | 9.2 | 5.0 |

| Finance, Other Business Services | 301.3 | 0.5 | 1.4 | 1.2 | 4.6 | 5.8 | 3.9 | 3.9 |

Tom Moeller

AuthorMore in Author Profile »Prior to joining Haver Analytics in 2000, Mr. Moeller worked as the Economist at Chancellor Capital Management from 1985 to 1999. There, he developed comprehensive economic forecasts and interpreted economic data for equity and fixed income portfolio managers. Also at Chancellor, Mr. Moeller worked as an equity analyst and was responsible for researching and rating companies in the economically sensitive automobile and housing industries for investment in Chancellor’s equity portfolio. Prior to joining Chancellor, Mr. Moeller was an Economist at Citibank from 1979 to 1984. He also analyzed pricing behavior in the metals industry for the Council on Wage and Price Stability in Washington, D.C. In 1999, Mr. Moeller received the award for most accurate forecast from the Forecasters' Club of New York. From 1990 to 1992 he was President of the New York Association for Business Economists. Mr. Moeller earned an M.B.A. in Finance from Fordham University, where he graduated in 1987. He holds a Bachelor of Arts in Economics from George Washington University.

More Economy in Brief