Global| Jun 20 2008

Global| Jun 20 2008Higher U.S. Gasoline Prices Crimp Miles Driven, and Economic Growth

by:Tom Moeller

|in:Economy in Brief

Summary

Do higher prices for something modify behavior? Probably. Do higher relative prices affect demand for something, maybe by a lot? Yes indeed. Consumers will buy less of the affected item or service whose price is rising more than the [...]

Do higher prices for something modify behavior? Probably. Do higher relative prices affect demand for something, maybe by a lot? Yes indeed. Consumers will buy less of the affected item or service whose price is rising more than the prices for other goods or services.

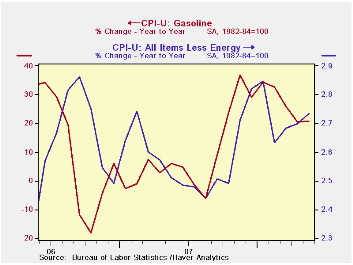

Through this past May, retail gasoline prices over the prior twelve months rose 21%. For all other goods and services, prices rose 2.7%. That left the relative price of gasoline up a very significant 17.5%. The increase was especially notable since it followed a year-on-year gain through the twelve months ended last November of 33.3%. That's when retail prices first moved above $3.00 per gallon.

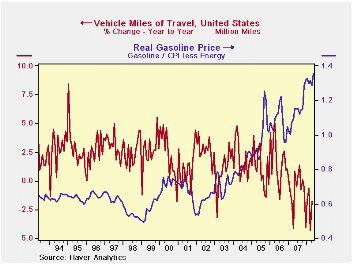

This rise in gasoline prices, along with slower jobs growth, dropped demand growth (the rise in vehicle miles driven) to -1.8% y/y after -0.8% growth last year. Those declines are versus positive growth rates between 1% and 3% during each year back to 1993.The figures on miles driven are available in Haver's USECON database.

By state the results are very diversified. Large year-to-year declines on the order of -3.0% have been logged in California, Florida, Virginia, Michigan, Wisconsin and South Carolina. Still growing were miles driven in Ohio, New Hampshire, New Jersey, Pennsylvania and New York. About unchanged were miles driven in Texas, Colorado, Connecticut, Delaware and Massachusetts. The figures on miles driven by state are available in Haver's REGIONAL database.

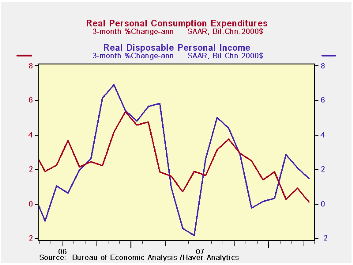

Ok, so what is it that consumers shifted their spending to? Here's the rub. It's not clear they could shift anything. Overall consumer spending growth through April, adjusted for inflation, fell to 1.6% y/y after 3.0% growth during the prior several years. And during the last three months the level of real spending was unchanged.

Consumers only can shift their spending pattern if they have money to shift. But there's been not as much of it. During the last year nominal disposable income growth moved lower to a 5.0% rate from roughly 6.0% during 2006 and 2007. Annualized three-month growth through April downshifted even further to 4.3%.

In real terms, disposable income during the last three months ran at a 1.5% annualized rate, half the growth during the prior several years. Much of the that slowdown is due to slower jobs growth. Respectable gains in nominal average hourly earnings helped this growth remain positive, but here again the news is bad. Nominal earnings rose at a 0.9% rate during the last three months and they were down during the last two.

How will all this finally shake out? In a bona fide economic recession. That is the conclusion of many and that certainly is the buzz in the popular press. But so far the Consensus opinion is that a recession will be skirted, but just barely. Positive real GDP growth, of just 0.7% during the last two quarters, generally is expected to extend through yearend '08 at a 1.5% rate according to a Consensus of roughly forty economists (in the Forecasters Club of New York). The range of expectations is, however, wide with roughly -2% as the minimum and +4% as the maximum.

Further increases in energy prices could easily tip that Consensus into negative territory, but so far...

Crude Awakening: Behind the Surge in Oil Prices from the Federal Reserve Bank of Dallas can be found here.

© 2008 HAVER ANALYTICS. All rights reserved.by Robert Brusca Italian and French Orders Give MIXED Signals June 20, 2008

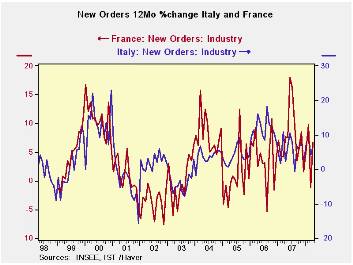

Italian orders rose by 1.2% in April after falling in March. France has experienced the same sort of orders volatility recently but with more extreme movements. Foreign trends are gradually slipping for Italy while French foreign orders are holding fairly strong. French domestic order weakness is dragging down its overall trends while for Italy domestic orders are strong.

The chart above shows that over longer periods French and Italian orders march to the same tune. Currently French and Italian total orders are on the same growth track year-over-year despite compositional differences is the source of the orders. Growth rates (Yr/Yr) seem to be cycling lower but not very dramatically and sequential growth rates do not tell a clear story about developing trends.

| Saar exept m/m | Apr-08 | Mar-08 | Feb-08 | 3-mo | 6-mo | 12-mo |

| Total | 1.2% | -0.5% | 2.2% | 12.3% | 6.0% | 6.5% |

| Foreign | -1.6% | -0.8% | 1.5% | -3.7% | -1.1% | 4.3% |

| Domestic | 2.6% | -0.2% | 2.5% | 21.8% | 10.0% | 7.8% |

| Memo | ||||||

| Sales | 2.2% | -1.5% | 0.9% | 6.5% | 8.1% | 6.9% |

| French Orders | ||||||

| Saar exept m/m | Apr-08 | Mar-08 | Feb-08 | 3-mo | 6-mo | 12-mo |

| Total | 5.2% | -6.4% | 1.6% | 0.3% | 2.8% | 6.6% |

| Foreign | 4.4% | -4.7% | 2.7% | 8.6% | 12.1% | 8.5% |

Tom Moeller

AuthorMore in Author Profile »Prior to joining Haver Analytics in 2000, Mr. Moeller worked as the Economist at Chancellor Capital Management from 1985 to 1999. There, he developed comprehensive economic forecasts and interpreted economic data for equity and fixed income portfolio managers. Also at Chancellor, Mr. Moeller worked as an equity analyst and was responsible for researching and rating companies in the economically sensitive automobile and housing industries for investment in Chancellor’s equity portfolio. Prior to joining Chancellor, Mr. Moeller was an Economist at Citibank from 1979 to 1984. He also analyzed pricing behavior in the metals industry for the Council on Wage and Price Stability in Washington, D.C. In 1999, Mr. Moeller received the award for most accurate forecast from the Forecasters' Club of New York. From 1990 to 1992 he was President of the New York Association for Business Economists. Mr. Moeller earned an M.B.A. in Finance from Fordham University, where he graduated in 1987. He holds a Bachelor of Arts in Economics from George Washington University.

More Economy in Brief