Global| Mar 05 2010

Global| Mar 05 2010Has Germany Found The Missing Link?

Summary

After dropping in December and raising eyebrows German orders have raised their game in January jumping by 4.3% month-to-month. Total orders are now accelerating steadily from twelve-months to six-months and from six-months to three- [...]

After dropping in December and raising eyebrows German orders have raised their game in January jumping by 4.3% month-to-month. Total orders are now accelerating steadily from twelve-months to six-months and from six-months to three-months.

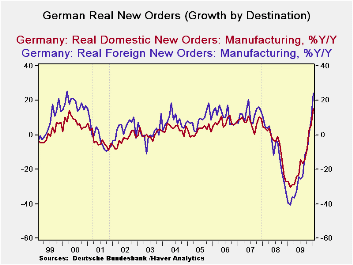

Foreign orders rose by 1.9% month to month just offsetting the drop of 1.7% in December. But domestic orders surged by 7.1% a rise substantially more than offsetting the 1.3% drop in December. Does this means that the German domestic economy is now awakened and back in the game? A weak domestic economy has been the missing link to German improvement and to sustained EMU growth, which so far has been export led and therefore a bit uncertain. The German domestic economy still lags the foreign sector in terms of Yr/Yr order growth but it has now begun to surpass it over terms of 3-months and 6- months.

Real sector sales trends still show consumer demand dropping but that is all due to nondurables weakness. In January as consumer durables sales jumped by 3.5% that spurt added to growth in sales from capital goods at 2.3%, intermediate goods at 2.2%, and mining/MFG at 1.1%.

Getting Germany on a stronger growth track particularly because its domestic economy is heating up would be a very positive development for the Euro-Area where growth has been sputtering and problems on the financial side have been plaguing the outlook. One good German number does not seal the deal for a better outlook but it is a big step in the right direction and one that has been long in coming. This is not the first spurt in domestic orders we have seen in this cycle. In July of 2009 they surged by 9.3% only to fall and sputter over the next three months. It may be that the domestic order series is just lumpy, so we should hold our praise. But this is a good a sign and we should watch to see if the trend has legs.

| German Orders and Sales By Sector and Origin | ||||||||

|---|---|---|---|---|---|---|---|---|

| Real and SA | % M/M | % Saar | ||||||

| Jan-10 | Dec-09 | Nov-09 | 3-MO | 6-Mo | 12-Mo | YrAgo | QTR-2-Date | |

| Total Orders | 4.3% | -1.6% | 2.7% | 23.7% | 11.2% | 19.7% | -34.0% | 8.7% |

| Foreign | 1.9% | -1.7% | 3.6% | 16.2% | 7.8% | 24.2% | -39.6% | 2.1% |

| Domestic | 7.1% | -1.3% | 1.6% | 33.2% | 15.4% | 15.2% | -27.2% | 17.5% |

| Real Sector Sales | ||||||||

| MFG/Mining | 1.1% | -0.9% | 0.1% | 0.8% | 0.4% | 2.6% | -20.1% | -2.3% |

| Consumer | -4.6% | 2.1% | 1.8% | -3.4% | -1.7% | -3.0% | -9.9% | 4.0% |

| Cons Durables | 3.5% | -1.4% | 2.3% | 18.4% | 8.8% | -0.8% | -15.9% | 12.6% |

| Cons Non-Durable | -5.8% | 2.6% | 1.8% | -6.6% | -3.3% | -3.4% | -8.9% | 2.7% |

| Captial Gds | 2.4% | -1.3% | 0.4% | 6.2% | 3.0% | 3.0% | -25.4% | -4.5% |

| Intermediate Gds | 2.2% | -2.0% | -0.5% | -1.2% | -0.6% | 8.3% | -21.4% | -1.0% |

| All MFG-Sales | 1.0% | -0.8% | 0.1% | 0.8% | 0.4% | 2.6% | -20.3% | -2.1% |

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief