Global| Apr 29 2010

Global| Apr 29 2010Globally Money Growth Is Just Not Getting Into Gear. So Where’s The Real Risk?

Summary

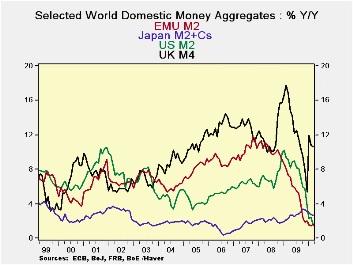

Money growth rates in Europe are starting to edge higher, but ever so slowly. At a 2.2% annual rate pace over three months compared to a 1.5% pace Yr/Yr is not much of an acceleration. Credit growth is however weaker over three months [...]

Money growth rates in Europe are starting to edge higher, but ever so slowly. At a 2.2% annual rate pace over three months compared to a 1.5% pace Yr/Yr is not much of an acceleration. Credit growth is however weaker over three months than over 12-months. In the US money growth is decelerating. In Japan it’s decelerating. In the UK, where inflation has started to flash some less than comfortable numbers, there is an issue. Money growth is in a major acceleration in the UK for M4 which is up at nearly a 40% annual rate pace over three months.

While the growth rates are different, the main themes remain in tact when we look at the growth rates of real money balances - money growth deflated by inflation.

Basically money is not much of a stimulant anywhere except in the UK.

Still we have great concerns among some economists that the fiscal spending and coming monetary excesses (paradoxically, fiscal issues already are taking what must be regarded as a deflationary toll in Europe) will result in a bout of inflation. For the most part, market pricing does not see that risk. Some of the hardest-money economists still are very worried. Some worry that the economy will recover and banks will begin to loan and this excess of reserves at the Fed will be unleashed into something that can become a torrent of inflation.

Then, others among us worry about getting hit by meteors from outer space.

While a cyclical pick up in lending is something we do expect in every business cycle, right now bankers are hunkered down. It is very hard to see how they are going to turn the lending spigot from a slow drip to full throttle in some quick fashion. Bank lending committees are notoriously slow in shifting their policy stance. The US economy and the European economies have a huge amount of slack. Conservative hard-money economists also point out that a lot of capacity was destroyed in the economic downturn. They warn that capital may appear to be less utilized than it really is. While that is a good point it is largely academic. The amount of slack in the economy is so great it’s like warning that the other rim of the Grand Canyon might be five feet closer than we thought so be careful about what might want to ‘fit inside of it.’

There will come a time to worry about these things. But unemployment in Europe is high. In the US 8.5 million people net were taken off the job rolls. In addition, many first-time job seekers were not able to find work. There is a great deal of slack. Money supply growth is slow. Europe’s fiscal situation has deteriorated making it a drag on the outlook despite some recent upbeat reports on growth. The question of the role of the deterioration in confidence in the e-Zone will play out over months not over hours. The US has its own fiscal challenge which will make public policy more contractionary ahead. Why all the worry about excess stimulus and inflation?

For the time being, despite high oil prices and some pressures on commodity prices, we have to signal the ‘all clear’ on the inflation front. Not enough growth remains as the near term clear and present danger. Inflation always lurks but it is, for the moment, unarmed and not very dangerous. Inflation is more lost in the woods and confused than it is dangerously lurking in some dark alley-way to mug an unsuspecting policymaker.

| Look at Global and Euro Liquidity Trends | |||||||

|---|---|---|---|---|---|---|---|

| Saar-all | Euro Measures (E13): Money & Credit | G-10 Major Markets: Money | Memo | ||||

| €-Supply M2 | Credit:Resid | Loans | $US M2 | £UK M4 | ¥Jpn M2+Cds | OIL:WTI | |

| 3-MO | 2.2% | -0.6% | 0.8% | -1.5% | 39.5% | 1.8% | 38.3% |

| 6-MO | 0.9% | -0.7% | 0.1% | 1.4% | 19.5% | 2.1% | 35.8% |

| 12-MO | 1.6% | -0.1% | -0.5% | 1.5% | 10.6% | 2.6% | 70.1% |

| 2Yr | 4.5% | 2.5% | 1.5% | 5.3% | 13.7% | 2.4% | -12.2% |

| 3Yr | 6.4% | 5.9% | 4.6% | 5.9% | 13.0% | 2.4% | 10.1% |

| Real Balances: deflated by Own CPI. Oil deflated by US CPI | |||||||

| 3-MO | 0.3% | -2.5% | -1.1% | -2.4% | 32.8% | 0.6% | 37.0% |

| 6-MO | -1.4% | -2.9% | -2.1% | -0.3% | 14.7% | 1.9% | 33.6% |

| 12-MO | 0.2% | -1.6% | -1.9% | -0.9% | 7.0% | 3.7% | 66.1% |

| 2Yr | 3.4% | 1.5% | 0.5% | 4.2% | 10.2% | 3.1% | -13.1% |

| 3Yr | 4.5% | 4.0% | 2.6% | 3.9% | 9.8% | 2.4% | 8.0% |

| Japan's March CPI is estimated to complete this table; The February value is used | |||||||

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief