Global| Sep 01 2016

Global| Sep 01 2016Globally Mfg PMIs Remain Weak; That Is Just the Symptom, Not Even the Problem

Summary

The global manufacturing scene remains weak in August with low valued PMI gauges across the spectrum. The environment for trade and commerce has deteriorated sharply and the risks to growth have become more palpable. At the IMF, [...]

The global manufacturing scene remains weak in August with low valued PMI gauges across the spectrum. The environment for trade and commerce has deteriorated sharply and the risks to growth have become more palpable. At the IMF, Christine Lagarde is talking about cutting growth projections again. The recent filing for receivership by the South Korean Hanjin shipping line is simply another manifestation of how much global trade has fallen from its expected path. The view of the Fed in the U.S. is that world has been `made safer' for a U.S. rate hike. It is laughably out of step with reality. The global environment is hostile and this month the U.S. manufacturing ISM is back below 50. Time for a rate hike? Really?

The global manufacturing scene remains weak in August with low valued PMI gauges across the spectrum. The environment for trade and commerce has deteriorated sharply and the risks to growth have become more palpable. At the IMF, Christine Lagarde is talking about cutting growth projections again. The recent filing for receivership by the South Korean Hanjin shipping line is simply another manifestation of how much global trade has fallen from its expected path. The view of the Fed in the U.S. is that world has been `made safer' for a U.S. rate hike. It is laughably out of step with reality. The global environment is hostile and this month the U.S. manufacturing ISM is back below 50. Time for a rate hike? Really?

The metric round-up

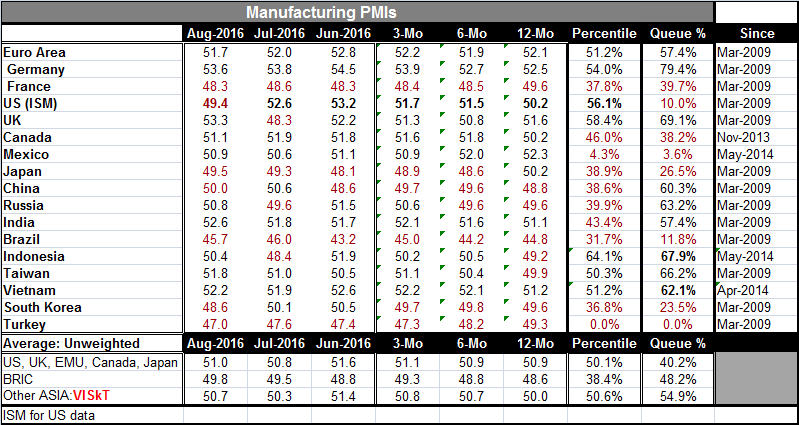

The proportion of manufacturing gauges weakening further in August is not particularly large (at 9 out of 17), but the proportion is far from negligible. There are seven PMI gauges that are at or below 50. The levels of the PMI gauges are uniformly low. At a reading of 53.6 in August, Germany has the strongest PMI in the table. The best monthly gain is from the U.K. where manufacturing has sprung back in the wake of the Brexit vote and is buoyed by the weaker value of the pound sterling plus by prompt easing action by the Bank of England.

The EMU gauge weakened month-to-month. Japan's manufacturing gauge was up but still below 50 showing contraction. China slipped back to a reading of 50. In the EMU, France continues to turn out a never ending string of PMI values below 50 as its manufacturing sector continues to struggle. In August, the U.S. manufacturing sector, joining France, is shrinking.

When the PMI gauges are viewed as percentile standings in their queues of data since early-2009, Germany's 79th percentile standing is tops in the table, followed by the U.K. at its 69th percentile, Indonesia at its 67th percentile, and Taiwan at its 66th percentile. These, of course, are not impressive standings: firm, yes, but strong, no!

There is also a low-end that is more impressive in a negative way, of course. Turkey has its lowest reading of the period. Mexico has been weaker only 3.6% of the time. The U.S. has been weaker only 10% of the time. Brazil has been weaker about 11% of the time. South Korea has been weaker about 23% of the time.

Turkey is extremely weak in the wake of its political unrest there. South Korea is newly back into the ranks of those with its PMI gauge showing declines in output.

The Global Pressure Cooker

The global economy is simply still weak. And pressures are beginning to take their toll as the U.S. and Europe seem to be on the verge of scraping their talks to further reduce barriers to trade and investment. Europe's aggressive attack on Apple's taxes, and thinly veiled threats from the EU that Apple is just the start, could raise transatlantic tensions even further before it's all over. Apple CEO Tim Cook has called the tax ruling `total political crap.' The U.S. has made it known that it has a provision its tax code to retaliate against Europe if it feels U.S. firms are being discriminated against. Star Wars has nothing on Trade Wars if it comes to that.

These kinds of tension and this level of acrimony is exactly what you expect to see in a period of economic stagnation. In such period, the economic pie is not growing fast enough. Trade begins to look like a zero-sum game (your gain is my loss). And both Trump and Clinton are pulling back from historic U.S. advocacy positions on more trade. Both Clinton and Trump oppose the TPP. Trump has been outspoken about renegotiating NAFTA. There are `rumors' that Hillary may have her own plans for some sort of NAFTA re-do.

Pressure in the U.S.

The bottom line for the U.S. is that jobs are not being created the way they used to be. We may still be churning out what looks like 200K or so jobs per month, but they are service sector jobs and wages as well as wage gains remain modest. Incomes in the U.S. have simply not been advancing. The Democrats' agenda to hike the minimum wage is a response to this lethargy although no one has explained how making firms pay workers more will make them more competitive.

What has happened?

The last U.S. current account surplus was in the early 1980s a pathetic admission. Since then, international trade has exploded and along with it so has the U.S. trade deficit. The U.S. worker is well aware that during this `highly dynamic global trade growth period' manufacturing jobs in the U.S. have been evaporating. You do not need a Ph.D. in economics to understand it. In fact, a Ph.D. in economics might be a hindrance since so many economists still push the line that more trade is better. It may be better globally, but trade is not being conducted on a fair basis, the rules of Free-Trade are not being followed and as a result the U.S. has not gotten its share of the trade pie. U.S. workers are being priced out of the global labor market. U.S. firms are moving to cheaper wage venues. The notion of comparative advantage is nowhere to be seen. Or to put it another way, the U.S. comparative advantage is so small and in so few industries that the U.S. seems to gain only one job for every four it losses. With this sort of job loss in train, U.S. workers have wound up out of their high-paying jobs and unwilling to work for much lower service sector wages. Many have opted to leave the labor force ratcheting up the burden on the U.S. budget and its social services network.

Europe

Europe has lost its patience in negotiating a trade deal with the U.S. (TTIP). A new study today hints that Europe is behind the times and needs $800 billion in new digital infrastructure investment to catch up with the U.S. and China. The lesson that U.S. workers have learned - even if U.S. officials have not - is that opening up to more trade when you are not competitive is a painful experience. Europe may be figuring this out for itself. And Europe's more open hostility to the U.S. may also have to do with the coming exclusion of the U.K. from the EU. The U.S. and U.K. have always been much more on the same page of freer trade. The rest of Europe has been far more obstructionist. With the U.K. out of the EU, this tendency is now showing through.

Exchange rates fail to do their job

There is no agency to police exchange rates and they are supposed to be the trade equalizers (re-equilibrators) in this hypothetically `floating exchange rate system' we have in the world today. It is clear that nations manipulate their exchange rates for results. And as the center or reserve unit, the U.S. is left with the residual - the other side - of whatever value our trade partners choose for their currencies. That residual has been a dollar with massive purchasing power, but one that leaves the U.S. worker on the outside looking in unable to get work in the modern global marketplace.

Backlash

The U.K. rebelled against the unwanted influx of foreign workers it could not control as an EU member. In the U.S., it is backlash against unfair and unfree trade and the result it has thrust upon the U.S. economy. Europe still has a very uneven playing field with Germany as its most competitive nation and other members sharing that same currency and struggling to compete inside their own home marketplace let alone in the world. Tensions are everywhere. Bureaucrats in Europe may feel they need to `feed something' to the public since the U.K. Brexit vote exposed how little the people of Europe really want to follow where there politicians lead. The U.K.

China's role

China simply expanded too fast and dislocated too many workers in other countries too quickly and the backlash is upon us. Still, China feels the pain too, since it still wants to grow faster to move more workers out of agriculture. But China's expansion has been too rapid and the excesses are clearly visible at home as well. It has spent funds unwisely and built up a huge stock of debt operating with too much cronyism and left a legacy of pollution. It has failed to be a good global citizen by polluting the environment, playing unfairly, on trade, not being responsible even when it got what it wanted like having the yuan inserted in the SDR basket. Moreover, it expropriated seas it had no right to and shuns international opinion contrary to its own selfish iconoclastic desires. China is now a big piece of global trade and it trades and operates unfairly.

Globalism loses its luster

Is it a surprising that the global trade mechanism is finally slowing down? Despite boiler plate about how we must avoid protectionism, what we are seeing is various forms of backsliding. Europe's attack on Apple is only the most aggressive new move. Do not expect this to end well. I'm wondering when the stock market will take notice. Oh yes negative interest rates (a sure-thing loss) may make a speculative gain look better. But at some point that tradeoff will wear thin.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief