Global| Jun 03 2016

Global| Jun 03 2016Global Services Show Softness

Summary

Globally the service sector remains weak and it is not stepping up to provide a counterbalance to ongoing and worsening manufacturing sector weakness. Six of 15 of these bellwether markets show a weaker services reading in May. Only [...]

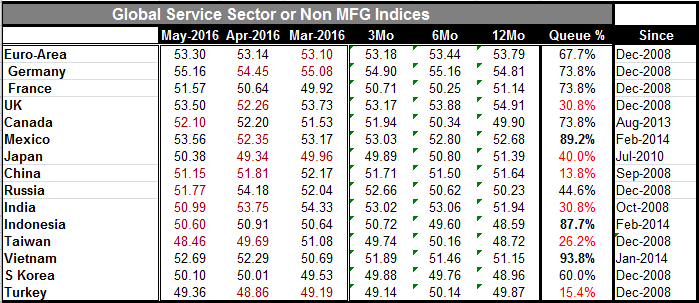

Globally the service sector remains weak and it is not stepping up to provide a counterbalance to ongoing and worsening manufacturing sector weakness. Six of 15 of these bellwether markets show a weaker services reading in May. Only Turkey shows a reading below 50. However, the service sector almost always grows. More significant is the run of weak queue standings (table: second column to the right). The queue standings position this month's diffusion index in its history of values back to 2008 or so. In this run of data there are six of 15 nations reporting severely weak sectors whose service sector readings are at or below the lower 40% of all their respective "historic" readings. There are only three really strong readings from Indonesia (87th percentile), Vietnam (93rd percentile) and Mexico (89th percentile). These, of course, are smaller economies that rely on export-led growth. Germany, France and Canada have readings that lie in their 70th percentile range (top 30%). The Euro Area and South Korea lie in their top 40th percentile. There is nothing here that is impressive from a global perspective.

Globally the service sector remains weak and it is not stepping up to provide a counterbalance to ongoing and worsening manufacturing sector weakness. Six of 15 of these bellwether markets show a weaker services reading in May. Only Turkey shows a reading below 50. However, the service sector almost always grows. More significant is the run of weak queue standings (table: second column to the right). The queue standings position this month's diffusion index in its history of values back to 2008 or so. In this run of data there are six of 15 nations reporting severely weak sectors whose service sector readings are at or below the lower 40% of all their respective "historic" readings. There are only three really strong readings from Indonesia (87th percentile), Vietnam (93rd percentile) and Mexico (89th percentile). These, of course, are smaller economies that rely on export-led growth. Germany, France and Canada have readings that lie in their 70th percentile range (top 30%). The Euro Area and South Korea lie in their top 40th percentile. There is nothing here that is impressive from a global perspective.

Remembering that the manufacturing sectors are outright weak... there is very little here to provide a backbone of support to counterbalance weakness in manufacturing.

With that as background, the weak US employment report for May could put the global markets in a severe state of shock. The US job weakness (albeit with the unemployment rate down to 4.7% - really!) is going to have profound global impact. The Fed has been assuming that growth is in train and that hiking rates was just a matter of time...sooner or later...and probably sooner. It also has simply assumed that the labor market would tighten and wages would rise, boosting inflation. Instead, the unemployment rate has dropped sharply and job growth has ground to a halt! Who saw that coming? Inflation which was rising early in the year has hit a plateau in the US. That goes for wage pressures too. Do we now know where we are in the business cycle or are we lost?

Other countries have been struggling to get growth over the hump to a point where it could sustain itself. But no other country has really had that success. And now the US central bank's "achievement" will be put under the microscope. Just this week OPEC met and really agreed to do nothing. But at that meeting the ministers saw the oil market rebalancing and the Qatar minister rather ominously concluded that "the worst is behind us". Well if the US economy is really downshifting he may want to rethink that comment.

We are back to a more topsy-turvy world in which there now is much less that we can take for granted and use as a base for analysis going forward. The week's data have not been kind to Europe. Just today e-Zone retail sales came up lame in April (dead-flat) one month after sales fell by 0.6%. EMU retail sales are slowing and decelerating over the last year and are contracting over the most recent three months. The global economy suddenly seems to be in a more precarious position. The OECD's call for countries to implement more stimulus seems more timely. And the break-up of the G7 meeting with no real call to action seems to be out of step with reality. On the other hand OPEC is making policy by wishing and hoping. Welcome to wonderland.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief