Global| Jan 03 2014

Global| Jan 03 2014Global Money Growth Stabilizes But EMU Credit Growth Lags

Summary

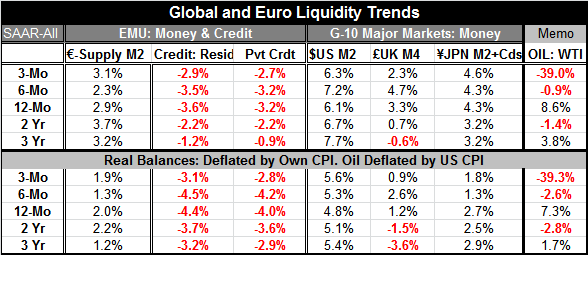

Money supply growth in EMU, the US, Japan and the UK has mostly stabilized. Year-over-year money growth ranges from 2.9% in EMU to 6.1% in the US. Over three months, money growth rates are generally little changed or higher than their [...]

Money supply growth in EMU, the US, Japan and the UK has mostly stabilized. Year-over-year money growth ranges from 2.9% in EMU to 6.1% in the US. Over three months, money growth rates are generally little changed or higher than their respective year-over-year pace in these countries. The UK has a drop off by 1% point in its three month pace compared to its year-over-year pace, but the economy in the UK has been growing strongly, particularly the manufacturing sector. Money growth does not seem to be a problem in the UK.

The growth in real money balances has turned modestly lower except in the US. Real money balances are experiencing positive growth in each of these major monetary centers. The UK at 0.9% sports the slowest growth in real money balances, followed by the euro zone at 1.9% and Japan at 1.8%.

While the money growth picture is relatively positive, the situation with credit growth in EMU is still an issue. The chart on the right shows money supply growth vs. private sector loan growth in EMU. While the EMU year-over-year money growth rate is little changed from the three-month pace, the interim EMU money growth had gone up and has since come down. After seeing EMU credit growth pick up from a low in 2009 to a high in 2011, credit growth in EMU has turned negative and its rate of decline has been steadily increasing. Over the past two months, the rate of credit growth deterioration has slowed and may have stabilized.

Since 2009 there has been a dramatic parting of the way between EMU money and credit growth rates. Now it looks as though weak credit growth is dragging down money growth. I have no cause-and-effect statistics at hand, but the chart is highly suggestive.

Meanwhile, the EMU economy is still showing signs of making progress, as manufacturing is doing particularly well and consumer confidence measures are improving. Nominal money growth of 3.1% is not going to support a very robust economy without velocity shifts. And with loan demand so weak, a shift in velocity does not seem to be very likely. So while EMU is giving us some real sector reasons to be more positive, the money and credit side of things is a bit more circumspect in EMU.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.