Global| Mar 11 2016

Global| Mar 11 2016Germany's Inflation Stays Low; Trends Work Lower Or Deflation Speeds Up

Summary

Deflation and monetary policy All eyes have been on the ECB and its next move which it executed just yesterday. The ECB rate cut was modest and the step up in asset purchases was a bit more. Broadening its programs and the asset [...]

Deflation and monetary policy

Deflation and monetary policy

All eyes have been on the ECB and its next move which it executed just yesterday. The ECB rate cut was modest and the step up in asset purchases was a bit more. Broadening its programs and the asset classes for participation are taken by some as a sign of being more aggressive. Some think this approach will be effective. Still, in these actions and in the ECB's own statement, there is the hint that interest rates may not go lower again. The ECB has palpable fear of deflation and when we look at German inflation trends we see why.

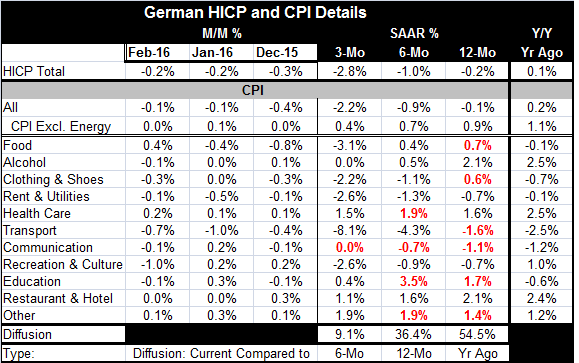

Tight German labor market; still no inflation

Germany has the tightest labor market in Europe, but when we look at German inflation over three months, inflation is higher compared to its six-month pace in only one line item (communication, where it is flat instead of falling). Six months compared to year-over-year, the line items in the CPI show acceleration in only four sectors marking inflation diffusion at only 36%. Inflation continues low in Germany, prices are declining broadly year-over-year as diffusion is low and the overarching trend is for inflation to continue to work lower. Even in Germany with a tight labor market- the lowest rate of unemployment since German reunification - there is still no trace of inflation in Germany. No wonder the ECB is running scared.

Limits to monetary stimulus

It looks as though monetary policy is bumping against limits. The BIS already has warned on negative rates and the ECB seems to be taking that warning to heart. There is, beyond that, the issue of how effective QE can be at an interest rate level that already is so low that its further impact will be to push securities yields farther into negative territory. Some are still upbeat on the ECB's moves. Draghi says that, so far, negative rates have worked well. But broadening the asset classes of purchases will not stimulate demand in the EMU region. And a shortfall in demand is the biggest problem, along with lingering concerns about banks. Europe does not seem to be beset by the same sort of ills as the U.S. economy in the pit of its recession and financial crisis. It is unclear to me how these bond purchases are going to heal Europe's economy or if the impact on rates is enough. The QE seems to be a measure poorly aimed at the real problem.

German inflation trends

Turning back to the German inflation data, we see that in February HICP prices fell month-to-month and year-over-year. The German domestic CPI fell by a tick less both month-to-month and year-over-year. The domestic CPI less energy was flat on the month and rose by 0.9% year-over-year. But both the domestic and the HICP headlines show inflation is still on a decelerating trend from 12-month to six-month to three-month. The domestic CPI, excluding energy, shows positive inflation, but its sequential rates of change are decaying steadily in magnitude. Inflation in Germany -anyway you measure it- is moving into or toward deflation.

Germany is unique

Germany is a unique low-inflation country. It operates well in a low inflation environment. It is no longer the clear lowest inflation country in the EMU since the financial crisis and the ongoing more strict implementation of Maastricht. In fact, one reason German inflation has not risen is that Germany has been on a program of sustained fiscal contraction. It was on its way to run a budget surplus this year until the financial requirements of housing migrants hit hard. However, Germany still has a fiscal offset to forces that might otherwise give rise to inflation. As a result, Germany continues to flirt with deflation. Germany has the room and the financial ability to use fiscal stimulus but has no need for it, or a desire to implement any stimulus.

Low inflation across EMU

Of the nine original EMU members that are early reporters of inflation data, seven show price levels declining month-to-month. The exceptions are Greece and the Netherlands. Prices last declined on a broad front like this in September and October of last year and from December 2014 to March 2015.

Deflation risks grow

Clearly Mario Draghi is getting more concerned about the risk of deflation as well as the damage from sustained low growth with high rates of unemployment; he has said as much. Global growth remains lax and China continues to underperform. The February readings on manufacturing and service sector PMIs show that manufacturing globally is mostly contracting and services are slowing. These are not the circumstances to raise inflation rates.

Inflation expectations drop and undercut policy effectiveness

Today in a quarterly Bank of England survey, Britons registered the lowest expected rate of inflation in the last 16 years. While market derived measures in the U.S. have also showed low readings, the Fed has continued to point to problems in using market measures to gauge inflation expectations. But St. Louis Fed President Jim Bullard holds that these measures are not so flawed and has his own worries about dropping inflation expectations in the U.S. If market expectations for inflation drop, they can hinder the central bank's ability to reflate the economy using its monetary policy tools. Is that now a new impediment to policy effectiveness?

Germany is on the deflation frontier

We see in German inflation trends more- not less- reason for the ECB to be worried. Ironically, it has persistently been Germany that has been opposed to a more activist ECB. And now Germany is skidding toward the abys of deflation and it seems unconcerned.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief