Global| Apr 24 2015

Global| Apr 24 2015Germany's Ifo Plows Ahead to Moderate 10-Month High; Is Germany's Sluggishness a Barometer for the World?

Summary

Germany's Ifo climate gauge is on a 6-month string of increases that has taken that gauge to a 10-month high. At its current position the gauge stands in the 80.5 percentile of its historic queue of values, roughly in the top 20% of [...]

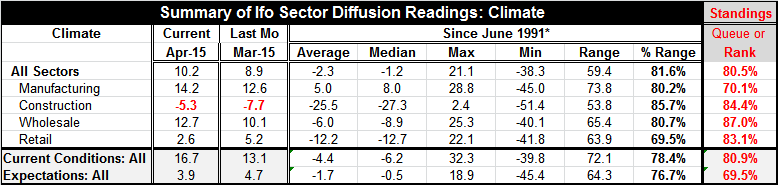

Germany's Ifo climate gauge is on a 6-month string of increases that has taken that gauge to a 10-month high. At its current position the gauge stands in the 80.5 percentile of its historic queue of values, roughly in the top 20% of all historic readings of this measure. That is a reasonably strong reading and one that would be the envy of any other EMU economy.

Germany's Ifo climate gauge is on a 6-month string of increases that has taken that gauge to a 10-month high. At its current position the gauge stands in the 80.5 percentile of its historic queue of values, roughly in the top 20% of all historic readings of this measure. That is a reasonably strong reading and one that would be the envy of any other EMU economy.

Is there a broader message here about global weakness?

As we saw in the earlier release of the Markit PMI data, the manufacturing sector in Germany is lagging, being led by all other service sub-sectors. This is despite an ongoing drop in the euro exchange rate that is boosting German competitiveness enormously in world markets and should be lighting a fire under its manufacturing sector. Perhaps we should take this lack of get-up-and-go as some barometer of the state of global demand? We have seen recent weakness in China's manufacturing sector as well as in the United States. U.S. reports on industrial production, durable goods orders and a spate of regional manufacturing surveys, as up to date as April, are showing weakness in the U.S. manufacturing sector too. Perhaps Germany's inability to turn its enormous advantage in competitiveness on the back of a very weak euro is a signal we should pay attention to more broadly?

Germany's manufacturing sector stands only in the 70th percentile of its historic queue of data, wholesaling stands in the 87th, construction in the 84th, and retailing in the 83rd percentiles of their respective historic queues. Despite its negative overall value, the construction sector is doing as well as it has in some time. All sectors improved in April except retailing which took a substantial drop.

The current conditions index rose strongly to 16.7 in April from 13.1 in March. It now stands in the 80th percentile of its historic queue of data. But expectations were actually set back this month. That gauge fell to 3.9 from March's 4.7 and stands in the 69th percentile of its historic queue.

Is there a broader message here about Greek fallout?

It is somewhat surprising that with the euro still very weak the German economy is not better jump started than this and that expectations are so muted and backtracking. One possible reason is that that ongoing angst over Greece is haunting the German economy, consumer and businessman's outlook. Greece continues to look for ways to worm out from under the austerity program it has been on. Each time Greece seeks some sidetrack or opportunity to pause, fellow EU members have pushed Greece back to the steep grade. Greece is running out of money and the endgame is getting precarious. Each side keeps hoping that the other will blink. I think there is some danger that Greece misunderstands the resolve of the EU.

Perhaps one additional way to read the weaker-than-expected German data is to say that the potential for fallout over Greece is still not fully priced into markets. While some blithely assert that that a Grexit would have little impact on markets, the truth is almost certainly that there would be substantial fallout despite the fact that Greek debt is now held in public - not private- hands. The real world is much more complicated than that.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief