Global| Nov 06 2008

Global| Nov 06 2008Germany's Flirtation with Rebound Is Smashed by a Stunning September Order Drop

Summary

German officials have officially ended their excursion trip with optimism. During their journey through fantasy land, they did take their turns in showing how wrong they can be. From the start of the US slowing, they thought Europe [...]

German officials have officially ended their excursion trip

with optimism. During their journey through fantasy land, they did take

their turns in showing how wrong they can be. From the start of the US

slowing, they thought Europe had decoupled and that the euro could

continue to rise with little ill effect on the Zone. When the other

e-Zone countries were affected they said Germany was different. When

the banking crisis hit the US they said German banks were strong and

did not have these sorts of problems. Recently they had believed

Germany was going to be so much less affected by the growing recession

in Europe as policymakers announced that Germany was better prepared to

meet the crisis. And so it may be. And we shall find out because ready

or not here it comes.

The pop in orders in August may have errantly encouraged the

belief that Germany was wearing some sort of special recession-proof

vest. But now Super-Germany has met its Kryptonite. The Sept plunge in

orders of -8% is the largest drop since German unification and has

swept optimism aside. Germany is now, after all, just another European

country with an economy under pressure, not a special case

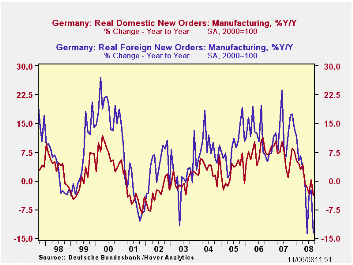

Moreover a perusal of the trends makes is crystal clear that

this downturn has been building for some time. Optimism in retrospect

looks a bit like whistling past the graveyard. August’s orders gain was

a rogue rise of 3.5% sandwiched in between drops of 1.7% in July and

now 8% in September. The sequential growth rates get progressively more

negative from -9% over 12 months to -12% over six months to -23% over

three months. Similarly the foreign and domestic orders show the same

progressions.

Germany is getting pulled down more by weakness from the

outside. So, in some sense, it is true that Germany has been faring

better. But in good times German export orders boomed beyond the reach

of domestic orders as well. Germany is simply a lower growth more

stable economy than the world in which it trades. Yet weakness abroad

will weigh on Germany just as a global boom will boost it. Because

Germany is plugged into that trading system, it shares the good and bad

times with the world it exports to. There is nothing unusual about that

or about the effect of that on Germany in this cycle.

The German industrial sales figures underline the issues.

German sales are showing the same sort of progressive declines. For a

while Germany was growing better than its trading partners because it

deals a lot in capital goods. One year ago German capital goods growth

rates rose 8% Yr/Yr while overall German sales rose by just 5.8%. But

in September German capital goods orders are being crushed. They are

falling by 5.2% in Sept alone. Their three-month pace of contraction is

-14.4% rivaling the 15.5% drop in the usually volatile sales of

consumer durable goods.

Germany has been caught in the same web of weakness that all

of Europe is in. Today’s industrial orders report combines with the

week’s earlier reports from the MFG and Services sector purchasers data

from Markit to show that weakness is spreading in Germany as well as

across the e-Zone.

Germany is in the soup along with the rest of Europe although

it may be submerging at a slightly slower rate. There can be little

doubt that Germany, like the rest of Europe is submerging. Down

periscope.

| German Orders and Sales By Sector and Origin | ||||||||

|---|---|---|---|---|---|---|---|---|

| Real and SA | % M/M | % Saar | ||||||

| Sep-08 | Aug-08 | Jul-08 | 3-Mo | 6-Mo | 12-Mo | Yr Ago | QTR-2-Date | |

| Total Orders | -8.0% | 3.5% | -1.7% | -23.0% | -12.2% | -9.0% | 6.4% | -14.7% |

| Foreign | -11.4% | 4.3% | -1.2% | -30.7% | -16.7% | -13.6% | 12.1% | -17.8% |

| Domestic | -4.3% | 2.8% | -2.1% | -14.2% | -7.4% | -3.9% | 0.8% | -11.4% |

| Real Sector Sales | ||||||||

| MFG/Mining | -4.0% | 4.5% | -2.4% | -8.2% | -4.2% | -1.9% | 5.8% | -5.0% |

| Consumer | -0.6% | 2.0% | -0.4% | 4.0% | 2.0% | -2.6% | 1.3% | -0.9% |

| Consumer Durables | -6.3% | 6.8% | -4.2% | -15.5% | -8.1% | -5.8% | 2.4% | -7.7% |

| Consumer Non-Durable | 0.6% | 1.2% | 0.3% | 8.5% | 4.2% | -1.9% | 1.0% | 0.6% |

| Capital Goods | -5.2% | 5.7% | -4.0% | -14.4% | -7.5% | -1.2% | 8.0% | -9.2% |

| Intermediate Goods | -4.3% | 4.2% | -1.7% | -7.5% | -3.8% | -2.6% | 6.0% | -2.5% |

| All MFG-Sales | -3.9% | 4.4% | -2.2% | -7.4% | -3.8% | -1.9% | 5.3% | -4.5% |

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief