Global| May 08 2019

Global| May 08 2019Germany: False Hopes from IP? Or a Turnaround in Progress?

Summary

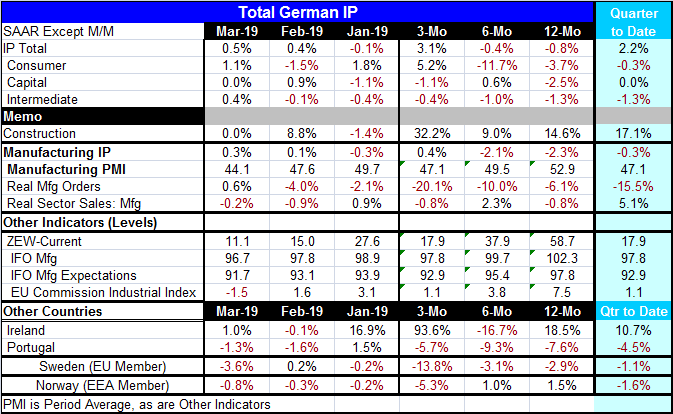

Germany's industrial production has sprung into action with a strong March reading but without much in the way of support from other industrial indicators. The weight of evidence from German manufacturing and industrial indicators is [...]

Germany's industrial production has sprung into action with a strong March reading but without much in the way of support from other industrial indicators. The weight of evidence from German manufacturing and industrial indicators is that conditions continue to deteriorate. IP optimism is on its own and bound to get lonely.

Germany's industrial production has sprung into action with a strong March reading but without much in the way of support from other industrial indicators. The weight of evidence from German manufacturing and industrial indicators is that conditions continue to deteriorate. IP optimism is on its own and bound to get lonely.

Strength; a one trick pony?

Much of the strength in industrial production comes from outside manufacturing; the manufacturing IP index rose by just 0.3% in March after a 0.1% increase in February. That is considerable less buoyant than for the IP headline. In the quarter-to-date, overall IP is rising at a 2.2% annual rate - that figure is now for completed quarter of Q1 2019. Compare it to manufacturing where the first quarter growth rate falls at a 0.3% pace. These are very different results

Moderate and mixed momentum heading into Q2

Inherited growth, which is a concept that checks the growth going into to Q2 is at a 5.5% annualized rate for overall IP but only at 2.7% for manufacturing. This measure is the IP measure for March divided by the Q1 average and compounded. It measures IP momentum in March heading into Q2 using the Q1 base for the assessment, the same base that will be used to calculate Q2 growth. On balance, inherited growth shows some momentum in place for Q2, but the result for manufacturing is not modest while the headline shows strength. These calculations can be fickle and, of course, are at risk to revision.

Message of pick-up is not supported

The table does not show any turnaround in the sequential growth rates of overall IP or its components. Construction IP is up strongly over three months but slowed over six months. Manufacturing, however, does show a slow turn to better growth rates for 12-month to six-month to three-month. But that sense of ‘progression' is small and slow-taking.

Manufacturing orders and sales slip

Still, manufacturing orders and real sector sales do not tell a strongly supporting story for the future or current situations. Real sector sales in manufacturing are lower in March and in February and decline on balance over three months. That is not a view of improving current conditions. Meanwhile, the look-ahead orders series shows accelerating contraction in progress.

Other indicators weaken

Other indicators from the overarching ZEW to the industrially targeted IFO and EU Commission reports show clear deceleration is still in gear. IFO manufacturing and expectations readings eased from January to February, as they did from March to February. And their averages also weaken on a sequential basis from 12-month to six-month to three-month. The EU Commission industrial index metric does the same.

Meanwhile in Europe…not much evidence of revival

Meanwhile, there are few other Europeans reporting with IP results in March. Ireland is (and has often been) a rogue reading. It is at it again with a sharp gain in output in March and a huge pick up reported over three months. Setting Ireland aside, we have two readings from the North of Europe and one from the Mediterranean; all three of these readings show output declines in March, two of three also show declines in February and in January. All three three-month growth rates are negative and two of three growth rates are also negative over six months and 12 months. Two of three of them show sequentially deteriorating growth rate trends as well.

A false spring in March (fake news!)

On balance, the IP result for March sticks out like a sore thumb. It does not find much support for a view of optimism. Most manufacturing or industrial reports for the current period or looking ahead are weak and in a weakening profile. For Germany itself, manufacturing alone is weaker than the IP headline and even construction output went flat in March. Taking all the data into account, the idea of a manufacturing rebound in March is on thin ice. Maybe this report will become revised or maybe it is just a simple misstep as those do occur. Output does not move in a simple knowable linear path. There are bumps in the road. Don't take this bump, which is a positive motivator, as evidence of a take-off.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief