Global| Apr 09 2020

Global| Apr 09 2020German Trade Surplus Explodes and European Policy Implodes

Summary

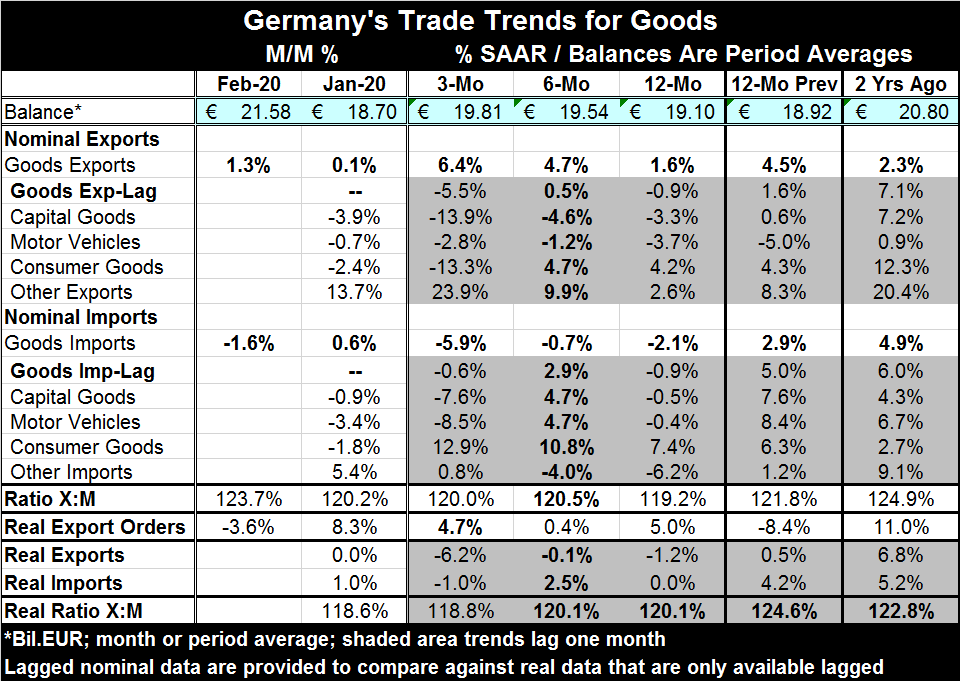

Germany logged its highest surplus since March 2018 when it was €21.68b. The surplus in February 2020 hit €21.58b. Powerful forces were at work on both sides of the trade balance in February with exports gaining 1.3% as imports fell [...]

Germany logged its highest surplus since March 2018 when it was €21.68b. The surplus in February 2020 hit €21.58b. Powerful forces were at work on both sides of the trade balance in February with exports gaining 1.3% as imports fell by 1.6%. August 2018 was the last time German imports fell by more than 1.6% (1.8%, August 2018). Exports were last stronger in September 2019 when they rose by 1.5%. But it was back in March 2016, nearly four years ago, that exports were last stronger at the same time that imports were weaker at that time the trade surplus stood at €22.43b.

Germany logged its highest surplus since March 2018 when it was €21.68b. The surplus in February 2020 hit €21.58b. Powerful forces were at work on both sides of the trade balance in February with exports gaining 1.3% as imports fell by 1.6%. August 2018 was the last time German imports fell by more than 1.6% (1.8%, August 2018). Exports were last stronger in September 2019 when they rose by 1.5%. But it was back in March 2016, nearly four years ago, that exports were last stronger at the same time that imports were weaker at that time the trade surplus stood at €22.43b.

The New Reality

As we know, February data are on the cusp of the new reality. It is hard to know which family of data this report really belongs to; is it still on a pre-corona trend or is there some post-corona trend? The export revival is suspicious and seems to belong nowhere. Since December 2018, any monthly German export gain of about 1% or more was adjacent to a month where there was a substantial decline of about 1%. So for the past two years, any monthly export bump-up like this was the result of volatility not of trend. With March data coming up next that seems a good bet to repeat. For imports, however, the 1.6% drop seems more real since it follows a gain of 0.6% that was preceded by two declines and a small gain before that...evidence of encroaching weakness.

Elusive Real Facts

The trend, in truth, is something hard to discern because of volatilities in the trade flows. Trade flow interpretation is made worse by a one-month lag in detailed data. The trends from one month ago have both exports and imports looking soft. All of the detailed export and import categories showed that flows fell last month except for the ‘other’ category that rose in both the case of exports and imports. The lagged vs. current sequential growth rates (three-months to six-months to 12-months) are like night day for both exports and imports. Lagged real exports and real imports are weaker for exports and about the same for imports. Real export orders fell in February but that as a stand-alone and is meaningless. In the January report, a massive surge of 8.3% in real export orders was logged. Real export orders over three months basically have the same growth rate as over 12 months. However, lagged real exports and imports each are weaker over three months than over 12 months.

Judgement Day

It is much more reassuring to draw conclusions and to judge data where trends are clear. But the more export trends we draw the clearer it is that clarity will not be a factor this month, Still, imports seem to be broadly trending weaker-setting the details aside. The jump in the trade surplus was outsized and is not likely a new trend unless imports collapse. Exports are unlikely to sustain strength given expectations for global demand and ongoing weak trade trends. In the wake of the coronavirus, severe import weakness is possible. On balance longer trends and context point to this report as an outlier. However, Germany already is talking of transitioning to some less restrictive behavior after Easter which is right on the door-step.

Summing up

As always, numbers only tell us so much. At any point in time, we always know somewhat more than what the numbers tell us because we live in ‘real time’ and the number necessarily lag. However, our knowledge is always incomplete. We, of course, never know about the rogue bit of data that we do not know about and do not discover for another month. So playing with numbers is like playing with fire. We also know that European cooperation as it works through the EU process is stuck and failing its mission. European stubbornness about liking their currencies their economies linked but not their public finances is an oxymoron they continue to refuse to come to grips with. This is an issue partly because Europeans are not one people. They have different cultures and priorities. So picking and choosing what to meld together makes sense…until it doesn’t anymore. In this crisis, it seems to make less sense, but the EU still cannot wrestle a deal to the table.

Addendum: Is Europe at it again?

Finland, for example, is willing to set up a domestic economy that delegates a greater role to its public sector. It controls the job market to a large extent, and depends on high marginal tax rates. The government’s role in the economy is large. Taxes are high. Finland is not ‘opposed’ to taxes. But Finland has consistently opposed any fiscal consolidation for the EU/EMU (that would require funding). This dichotomy in values points to something I have long maintained that economic systems are a function of culture more than a competition among systems themselves in any absolute sense. And European nations naturally consider themselves more attached their indigenous culture than they consider themselves European. They are French first, German first, or Greek first…then European. That shows in the economic system they have cobbled together. In contrast, Americans consider themselves Americans first, not Ohioans, or Michiganders or Texans...well Texans may be an exception! When a nation has a set of values, its economic system must be consistent with those values or it will fail. The Maastricht rules were written by hard money Germans, Austrians and Dutch to underpin the EU and EMU in the absence of a fiscal union. These rules have created the greatest pain for southern Europeans. That is hardly a surprise. And so it continues to go…even as southern Europe has finally put inflation back in the bottle; arguments over debt and the role of fiscal policy continue to rage in Europe and hamper a more cohesive policy even in times of great trial. Recall that the ECB went through a similar torturous vetting of its policies through the German legislature in the Great Recession. These deliberations hamstrung the ECB and prevented it from acting quickly condemning it to a policy response that was eventually allowed but was too little too late and ultimately less effective because of that. Is Europe at it again?

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief