Global| Apr 09 2008

Global| Apr 09 2008German Trade Picture Produces a Higher Surplus on Weak Imports

Summary

The German trade picture shows a month-to-month slowing imports and flat exports. The slowdown in both the flows may be just monthly volatility or something more ominous. So far Europeans have remained up beat on their economic [...]

The German trade picture shows a month-to-month slowing imports and flat exports. The slowdown in both the flows may be just monthly volatility or something more ominous. So far Europeans have remained up beat on their economic outlook even as the US economy has slipped. The OECD has held its forecast for 2008 growth for Germany above 2% while the fresh IMF forecast du jour (in fact, of today) cuts German growth by just 0.1% from the IMF’s last guess in January, bringing it to a pace of 1.4%.

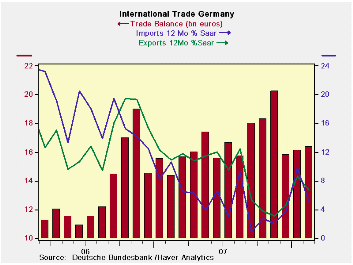

The growth rates for exports and imports may be a bit misleading in the table, due to recent volatility. As the chart shows, both exports and imports accelerated from a September low for imports and a November low for exports. Both series have since topped out and growth rates have declined. The trade surplus plunged in December from a high in November but has since begun to edge higher as the pace of both exports and imports has cooled.

In the recent three-month period German imports of capital goods have been surging while German capital goods exports have remained subdued. Capital goods have been the lifeblood of the German economy. Domestically, consumption has just not kicked up. Consumer goods imports are holding steady at around a 6% growth rate while exports of consumer goods have been 20% to 25% over the recent year to three months in terms of annualized rates of growth. For the moment German trade flows appear to be slowing.

| German Trade Trends for Goods | |||||

|---|---|---|---|---|---|

| m/m% | % Saar | ||||

| Feb-08 | Jan-08 | 3M | 6M | 12M | |

| Balance* | €€ 16.37 | €€ 16.10 | €€ 16.09 | €€ 17.48 | €€ 16.83 |

| EXPORTS | |||||

| All Exports | 0.0% | 3.6% | 9.3% | 6.6% | 6.7% |

| Capital Goods | -- | -0.3% | -0.6% | 3.0% | 4.6% |

| Motor Vehicles | -- | -0.3% | 0.8% | -1.0% | 4.2% |

| Consumer Goods | -- | 10.3% | 23.7% | 25.6% | 18.5% |

| IMPORTS | |||||

| All Imports | -0.4% | 4.0% | 41.9% | 6.1% | 5.1% |

| Capital Goods | -- | 5.7% | 11.4% | 13.5% | 7.1% |

| Motor Vehicles | -- | 12.0% | -6.3% | 18.3% | 6.0% |

| Consumer Goods | -- | 3.5% | 6.5% | 4.7% | 6.6% |

| *Bil.Euros; mo or period average; Shaded area trends lag one month | |||||

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief