Global| Nov 08 2019

Global| Nov 08 2019German Trade Flows Show Some Life...There May Be Life on Mars, Too

Summary

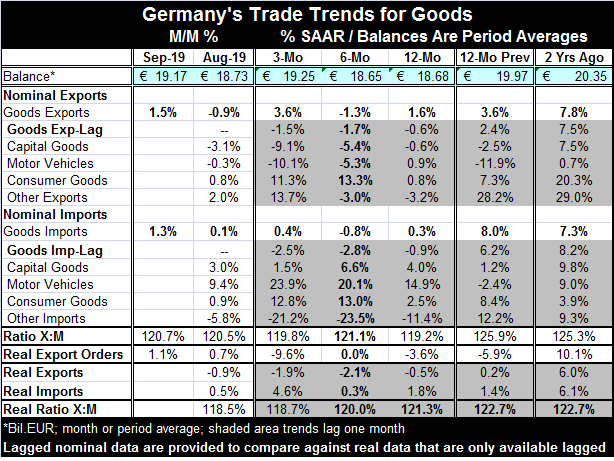

The trends The German trade surplus is waffling at a level lower than it was before July of last year (see Chart). Export and import growth rates have been declining as well. Import growth that has been stronger than export growth for [...]

The trends

The trends

The German trade surplus is waffling at a level lower than it was before July of last year (see Chart). Export and import growth rates have been declining as well. Import growth that has been stronger than export growth for most of that period has just switched to become weaker over the last few months. Year-on-year German export growth rates have declined moderately over the period while German import growth rates have declined at a more rapid pace. But now, both export and import growth rates have stopped declining and have experienced some degree of rebound and stabilization over the last three months. It is a clear enough signal but as it is only three-months old it is not a very reliable one.

The trade flows in context

More importantly, there are no changes in global events to give us confidence that there is anything fundamental driving the shift in German export and import growth rates. And since trade flows can be volatile, it is important to be sure that pertubations in the data are given time to even out or to develop into new trends before treating them as true signals. Real export orders are still declining and are declining faster than German real exports. As we saw yesterday, German industrial production continues to slow but it showed some tendency for the rate of decline to begin to abate. Other German surveys on activity, however, continue to be weak and declining. Away from the German situation, global manufacturing PMI data have continued to be weak and this is on data available into October as well. In any event, the trends show German imports barely growing year-on-year with exports posting a growth rate of 1.6%.

Real export and import trends

Real export and import data (data adjusted for the effects of inflation to mimic volume) show exports falling by 0.5% over 12 months and weakening to a pace of around -2% over six months and over three months. Import volume is up by 1.8% over 12 months, slows over six months and then expands at a 4.6% annual rate over three months. The volume data and trends are not as hospitable to the view of recovering export trends while imports are still showing some growth despite clear weakness in the German economy and faltering GDP. This suggests that there is still some growth in domestic demand in Germany and at the same time that German exports are facing difficult conditions abroad. The ratio of real exports to real imports has continued to fall.

Export and import product trends

Export and import trade flow details lag by one month. But on that basis, exports show declines in year-on-year capital goods with very modest (less than 1% gains) in consumer goods and motor vehicles. Imports over one year show gains in capital goods imports, consumer goods and motor vehicles offset by a decline in 'other.' Over 12 months on this lagged basis, both exports and imports are declining in nominal terms.

Summing up

On balance, the headlines and tends show some sense of bottoming. There is a similar hint for the German industrial production data for September and a very minor bounce in the Markit manufacturing survey for Germany. However, the September and October surveys from IFO, ZEW and on manufacturing from the EU Commission do not corroborate any sense of bottoming or rebounding. Globally, the factors causing uncertainty and impairing trade flows are still in play and geopolitical conditions are as worrisome and frazzled as ever. Not only is the sense of rebound in this month's data weak, it comes without any strong base of support from external real world developments: no clarity on Brexit; no U.S.-China trade deal; no U.S.-EU rapprochement on trade either. The EU Commission and the IMF have just cut their growth forecasts for Europe and for Germany. Trade data can be volatile and even in this report we see key differences in real and nominal data trends. We do not find corroboration of bottoming in related economic or industrial surveys. It's a good time to keep optimism at an arm's length and yet too soon to embrace pessimism.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief