Global| Aug 09 2016

Global| Aug 09 2016German Trade Flows Languish

Summary

The German trade surpluses remain large. While Germany's surplus ticked lower in June, the last four months show surpluses much higher than over the previous seven months. Goods export did tick higher month-to-month in June as imports [...]

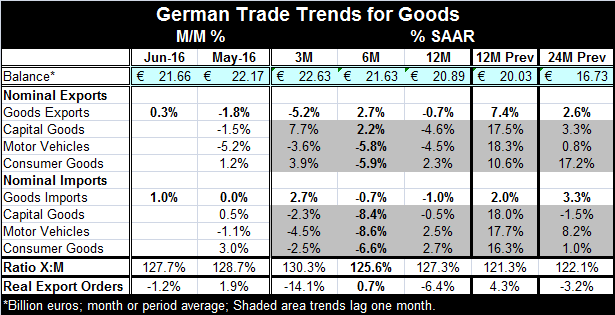

The German trade surpluses remain large. While Germany's surplus ticked lower in June, the last four months show surpluses much higher than over the previous seven months. Goods export did tick higher month-to-month in June as imports rose by 1%. But over three months exports are falling at a 5.2% pace and over 12 months they are falling at a 0.7% annual rate.

The German trade surpluses remain large. While Germany's surplus ticked lower in June, the last four months show surpluses much higher than over the previous seven months. Goods export did tick higher month-to-month in June as imports rose by 1%. But over three months exports are falling at a 5.2% pace and over 12 months they are falling at a 0.7% annual rate.

Imports in comparison showed some life in June, but not much life as they rose for only one month in a row but did make a gain of 1%. Imports are up at a tepid 2.7% annual rate over three months but are net lower over both six months and 12 months.

There is not much here on which to build an optimistic outlook either for German domestic demand or for German exports and the prospects for demand overseas. Real export orders fell in June and are falling at a 14.1% annualized rate over three months as well as falling by 6.4% over 12 months.

More detailed data show that German exports are up by 2.3% over 12 months to EU members but only by 0.1% to EMU members. German exports to EU members (a group that has an important contribution from the U.K. where future flows may be challenged) are up by a strong 6%. German exports to countries outside the EU area fell by 0.4%. Germany's exports are strongest where they are apt to encounter the biggest challenge in the next 12 months as the Brexit reset could alter trade dynamics between the U.K. and EU/EMU members. On top of that, the pound sterling has been declining sharply and that will alter the German-U.K. competiveness balance. At the same time, German imports from EMU nations are up by 3.0% over 12 months, a bit weaker than the 3.9% for non-EMU members of the EU. Imports from outside the EU are off by 5.4%. That reflects weaker oil import prices to some degree.

These trade data are consistent with the weak picture that continues to emerge from the global PMI indices that are now up-to-date through July. Global weakness remains in force and export and import flows continue to show the effect of that ongoing weakness. In July, weakness in emerging markets let up just a bit, but the overall conditions of weakness lingers.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief