Global| Oct 10 2019

Global| Oct 10 2019German Trade Flows Continue to Wind Down

Summary

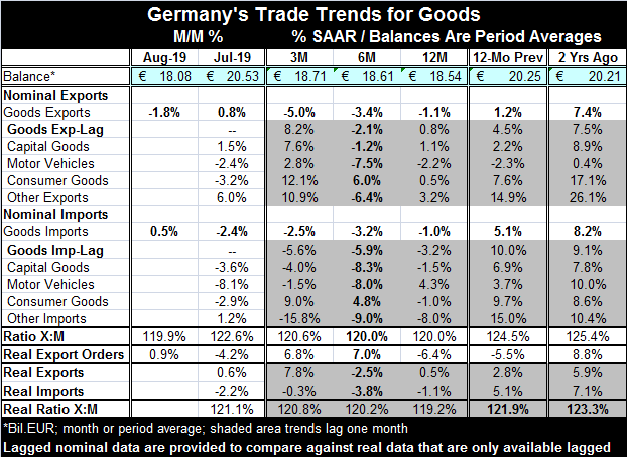

In today's trade report, Germany logged a drop in exports of 1.8% month-to-month and of -1.1% year-on-year for August. German imports edged higher by 0.5% month-to-month while falling by 1% year-on-year. Germany's trade deficit fell [...]

In today's trade report, Germany logged a drop in exports of 1.8% month-to-month and of -1.1% year-on-year for August. German imports edged higher by 0.5% month-to-month while falling by 1% year-on-year. Germany's trade deficit fell month-to-month to 18.1 billion euros in August from 20.5 billion euros in July and skimmed slightly below its average over the past 12-months (18.5 billion euros).

In today's trade report, Germany logged a drop in exports of 1.8% month-to-month and of -1.1% year-on-year for August. German imports edged higher by 0.5% month-to-month while falling by 1% year-on-year. Germany's trade deficit fell month-to-month to 18.1 billion euros in August from 20.5 billion euros in July and skimmed slightly below its average over the past 12-months (18.5 billion euros).

There continues to be a drum beat of weak economic data that sweeps across Europe and washes over global economic releases. Trade flows are slowing globally. Economic forecasts are being cut. Central banks are providing stimulus in heretofore unknown quantities and yet economic weakness of various sorts appears to be still encroaching. Trade is thought to be the ‘carrier of this dread slowdown disease. Even as the United States and China sit down to talk turkey about trade, the impact of their trade war is felt around the world. Can China and the U.S. make enough progress on trade to provide a tangible signal that these talks can continue and can produce progress? This is the question that markets are hoping to get an answer to and they further hope that the answer is ‘yes.'

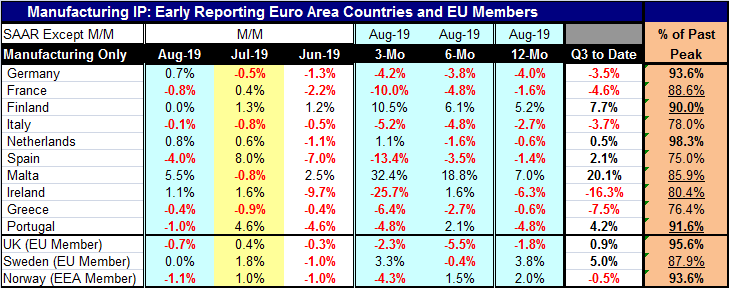

The table below shows the impact of the trade wars and generalized economic slowing on the manufacturing sectors of early-reporting European economies. The whole of the EMU area has yet to report. Of the 13 countries in the table, eight show that IP is declining year-over-year as well as over six months. Nine show manufacturing production lower on balance over three months. Over three months, there are three double-digit rate of declines and another three at or close to (round down to) a five percentage point annual rate drop. There are also two small economics, Malta and Finland, with double-digit growth over three months. Monthly data show the breadth of decline at its worst in June when 11 of 13 countries saw manufacturing output fall. But output returned to growth the next month for all but three of those countries. In August output is declining month-to-month in about half of the reporting countries in the table with the simple average month's percent change for this group at zero.

Unemployment rates remain low. The OECD has been reporting lows in its inflation environment among member countries as well. The far right had column in the IP table shows that six countries have output still within 10% of their past cycle peak despite the slowing and pullback.

European industrial production is under pressure

German trade data illustrate the pressures as German goods exports decline and decline progressively faster over 12 months, six months and three months. German imports decline on all three horizons as well but their decline is not at pace that is accelerating. Export and import volume trends (that lag one month) flip that trend with import volume weaker than export volume as exports actually show some life over three months even as import volumes contract.

Germany is highly trade dependent, but its circumstance is complicated since it also sells a lot of its goods without any exchange rate consequence within the euro area's single currency borders.

Germany's trade surplus is modestly weaker in 2019 than it was for most of 2018; there is still a lot of volatility in that trade-balance gauge. And despite somewhat uneven export performance, German real export orders are rising briskly over three months and over six months despite their year-over-year decline.

The specifics on trade remain in flux and individual export and import flows are volatile. But Germany's year-on-year export and import trends (see the graph) clearly point to an ongoing slowdown. Year-over-year export orders, real imports, nominal exports and nominal imports all are declining. Export volumes are higher but only by 0.5%- that's not much of an exception.

In addition to the U.S.-China trade war, there is also risk from the ongoing Brexit negotiations, but these now seem destined to go unresolved by their Halloween deadline. Despite threats to the contrary, the deadline seems likely to be pushed into the future again to avoid what would otherwise be a disruptive Hard Brexit solution. The only hard Brexit on Halloween will be the No-Hard Brexit pill that Boris Johnson will have to swallow.

Still...do not fail to read the tea leaves. There is a great deal of weakness. Each of the big four EMU economies (Germany, France, Italy and Spain) have manufacturing IP falling over 12 months, six months and three months. Three of the four of them show output trends getting progressively weaker. And while Germany is an exception to this deceleration trend, it is an exception in only technical terms. The IP trends align with other surveys from the EU Commission, from Markit and from various national sources. The weakness across Europe is palpable. But there is still hope for some kind of a trade deal as the clock is ticking. It is just not clear that even if there is a ‘late inning' trade deal that there is enough time to avert a global recession. That probably depends on exactly what it is and how much of the uncertainty it sweeps away and how much China and the U.S. might be willing to buy into trusting the ‘other guy.' Frankly, the prospect for that kind of result seems very remote.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief