Global| Dec 09 2019

Global| Dec 09 2019German Trade Data Tell a Tale of Two Germanys

Summary

Germany's October trade report is better than expected. The surplus is up on the month, above its 12-month average and above its year-ago value. Exports are rising for the second month in a row and for the fifth time in six months. [...]

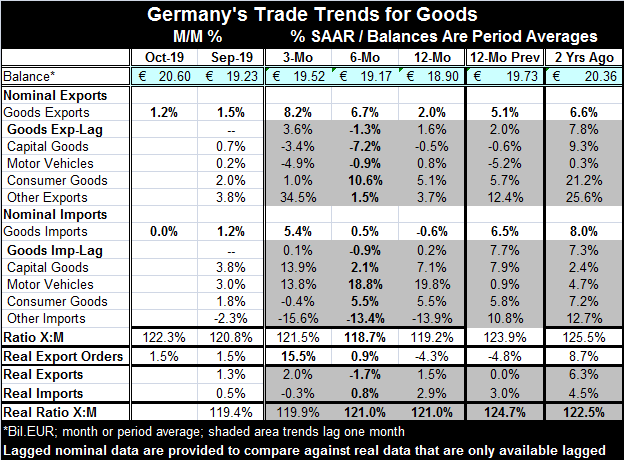

Germany's October trade report is better than expected. The surplus is up on the month, above its 12-month average and above its year-ago value. Exports are rising for the second month in a row and for the fifth time in six months. Imports are flat in October after rising in September. Sequential growth rates from 12-months to six-months to three-months show both exports and imports are accelerating.

Germany's October trade report is better than expected. The surplus is up on the month, above its 12-month average and above its year-ago value. Exports are rising for the second month in a row and for the fifth time in six months. Imports are flat in October after rising in September. Sequential growth rates from 12-months to six-months to three-months show both exports and imports are accelerating.

But in real terms, these trends do not stand up. 'Real,' otherwise known as inflation-adjusted data, lag the more topical nominal data by one-month. And lagged one month the nominal trends do not show these patterns either. In fact, real import data show import growth to be deteriorating on the timeline. Real export growth shows real exports to be waffling and contained in a growth range of -1.7% to +2.0%.

The chart, plotting year-on-year trends, shows some modest export revival and import sluggishness in nominal terms.

Real export orders, up-to-date through October, show revival and acceleration in orders. Still, real export orders are falling by 4.3% over 12 months.

The political conditions in Germany have turned much more difficult for Angela Merkel and her coalition government. Economic performance is struggling. The Bundesbank expects struggling to continue for a few more quarters.

The ZEW experts on the other hand have suddenly brightened their outlook. While German expectations have been higher about 70% of the time, the November reading improved from an October reading that has been better about 88% of the time. The net impact is clearly improved; still, it remains as a negative outlook but with a shift to the positive.

In fact, with expectations high for a U.S.-China trade deal, the negative ZEW readings for the euro area (implied), Germany, the U.S., Japan, the U.K., France and Italy shifted up sharply in November. The monthly shifts across these regions were so large that when ranked as monthly improvements have been greater only 2% to 4% of the time among these countries on data back to 1992. However, in absolute terms, ZEW expectations are still negative on balance for all these countries and despite the large improvement in the outlook, the outlook itself ranks no higher than that the 27th percentile and as low as the 14th percentile for individual countries. You could call it a shift from abject pessimism to negativism.

German nominal sector data for exports also lag. Three-month trends show the best export growth for the category 'other exports' with still sharp declines over three months for motor vehicles and capital goods. Year-on-year there is nominal growth in consumer goods and 'other exports' with capital goods exports lower on balance.

Lagged German nominal import trends over three months show strong gains in capital goods and motor vehicles with weakness in 'other' imports. Over 12 months most flows expand, motor vehicle imports are strong, but 'other' imports are weak holding the overall lagged import rise to only +0.2%.

On balance, there are mixed trends for German imports and exports. There is a background of weak industrial reports which contrasts with sharply improved although still negative expectations. All of this makes for a somewhat confusing environment. But there are a lot of hopes pinned on some sort of U.S.-China trade deal coming on line and delivering a boost to growth or at least reducing the drag on the outlook significantly.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief