Global| Oct 11 2019

Global| Oct 11 2019German Price Trends Are Affirmed at a Slow Steady Pace; Germany Policy Desires and Demands Remain Restrictive

Summary

Germany is renowned for its aversion to inflation. It suffered hyper-inflation in the 1920s and this experience made an indelible mark on the German psyche. That experience was extreme. And it has left Germany averse to even a whiff [...]

Germany is renowned for its aversion to inflation. It suffered hyper-inflation in the 1920s and this experience made an indelible mark on the German psyche. That experience was extreme. And it has left Germany averse to even a whiff of inflation. One account of German hyperinflation puts the cost of a loaf of bread at RM2million. One month later that cost went up to RM670million, then to RM3billion, and week later to RM100billion. No wonder the currency collapsed. At some point, the printing presses literally could not keep up. Some of the accounts of the period talk of workers getting paid at noon and running out to spend their money before it lost even more value. Clearly this was an extreme situation.

Germany is renowned for its aversion to inflation. It suffered hyper-inflation in the 1920s and this experience made an indelible mark on the German psyche. That experience was extreme. And it has left Germany averse to even a whiff of inflation. One account of German hyperinflation puts the cost of a loaf of bread at RM2million. One month later that cost went up to RM670million, then to RM3billion, and week later to RM100billion. No wonder the currency collapsed. At some point, the printing presses literally could not keep up. Some of the accounts of the period talk of workers getting paid at noon and running out to spend their money before it lost even more value. Clearly this was an extreme situation.

However, that experience was a long time ago, over 90 years ago. In this post Great Recession period, inflation has been persistently below the 2% target ceiling that has been adopted by the ECB, the bank that now serves Germany. With the minutes of the last ECB meeting just released, some of the discord that underlies the last policy decision is laid bare. However, the existence of discord is no surprise. A German member of the ECB executive board already has resigned, Sabine Lautenschläger. That resignation was a protest against the new stimulus measures that were adopted even though EMU-wide inflation continues to undershoot

The chart shows the EMU inflation situation which is the basis for EMU policy. Inflation continues to undershoot and the trend continues to point even lower. The ECB, like the Bundesbank which it was modeled upon, has only an inflation target to govern its behavior. Clearly, the ongoing target miss calls for more stimulative measures. And just as clearly, Ms. Lautenschläger was unwilling to continue to pursue policy based on inflation performance alone.

The chart shows the EMU inflation situation which is the basis for EMU policy. Inflation continues to undershoot and the trend continues to point even lower. The ECB, like the Bundesbank which it was modeled upon, has only an inflation target to govern its behavior. Clearly, the ongoing target miss calls for more stimulative measures. And just as clearly, Ms. Lautenschläger was unwilling to continue to pursue policy based on inflation performance alone.

If we index the HICP to December 2008 at the time of the Great Recession a time when the HICP's position gauged from its inception was running below its target, we find a get deal of price weakness was about to emerge. From that on-target position, the ECB then let the price level slip substantially below its targeted path on a persistent basis. And this is a central bank with only one target - inflation. In resetting the target base to December 2008, we find some early inflation undershoots and brief and a period with overshooting. Inflation ran too hot from December 2010 through January 2013. But from 2013 onward, the actual price level began to lag the target sometimes missing very badly and more than offsetting the overshoot. Currently, the shortfall tracking back to 2008 has grown to 8 percentage points. That means the price level would be eight percentage points higher than it is now had it run at a 2% pace since December 2008. That cumulative miss is roughly equivalent to having run inflation low and too cool by about 0.8 percentage points per year for a decade (roughly at a pace of 1.2% instead of just below 2%).

So the German angst over ECB policy is not about excessive inflation in the EMU where inflation is still below target. Nor is it about rising inflation in the EMU since that is not in train either. Instead, it is about the structural nature of policy, the continued existence of negative interest rates and the long period of running such an expansionary monetary policy. While all of these reasons may be rock-solid on paper, in the real world the ECB has undershot its target by a massive amount and there is no sense that the situation is being righted.

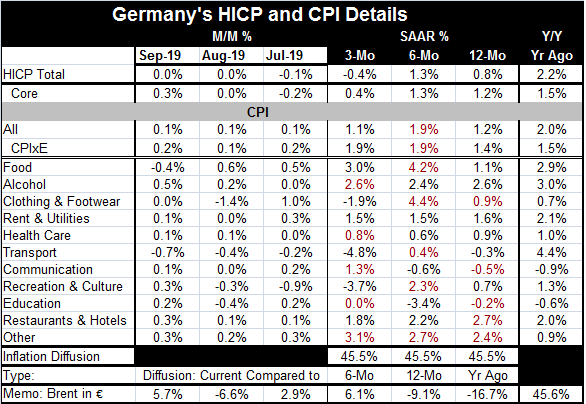

German inflation trends continue to move sideways in HICP terms, with the HICP in Germany up by just 0.8% and the core up by 1.2% over 12 months. Both measures show ongoing deceleration as well. However, the German CPI shows a headline at 1.2% and holding its pace from 12-months to three-months while the core at 1.4% over 12-months has accelerated to a 1.9% pace over three months and six months.

Of the 11 categories in the German CPI (see Table below), three-month inflation is accelerating in only five of them; the same is true for inflation over six months and over 12 months. While these comparisons ignore the importance of the various sectors, this sort of diffusion analysis is still valid suggesting that inflation is not taking root and spreading.

Not only does the historic price level targeting of the ECB show that monetary policy has been too tight, and not only do current trends show that German inflation is not percolating, but in addition, the German economy is weakening with very weak activity measures for manufacturing, orders and other metrics. Even the German services sector is weakening. It is difficult to know why Germany, apart from its past and its known aversion to inflation, is taking such a hard line when the economic macroeconomic facts are presented and are so clear and so unequivocal. As a policy Germany is even running a contractionary fiscal policy as inflation continues to undershoot. Germany has prioritized reducing its own debt relative to GDP.

This is nothing short of obsessive behavior. It unfortunately comes from Europe's largest economy and the one most able to engage economic stimulus at a time that stimulus is badly needed. But Germany is not a team player. Germany is a very rules oriented player. And regardless of the current circumstances, Germany is choosing to follow and obey all the rules and to make its macroeconomic debt and deficit positions even stronger. It is unfortunate for the rest of Europe that Germany cannot see its way clear to use some of its fiscal flexibility to help Europe with its clear shortfall of demand. That choice is even more peculiar since Germany runs an export-oriented economy that essentially ‘feeds off' the demand created in its trade partners. In short, German fiscal austerity really does not hold Germany back much since its producers and exporters tap demand sources beyond German borders.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief