Global| Aug 20 2015

Global| Aug 20 2015German PPIs Get Up and Go, Got Up and Went; German PPI Remains Weak

Summary

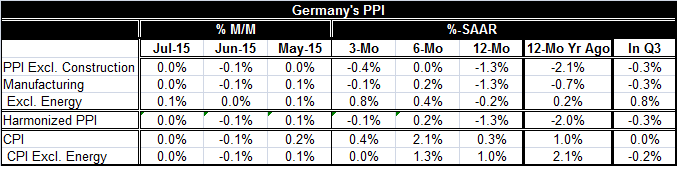

The German PPI has reversed its course to higher rates of expansion to go dead flat in July. Manufacturing producer prices are flat. Ex-energy the manufacturing PPI is up by 0.1%. Indeed, over three months, the PPI is falling and [...]

The German PPI has reversed its course to higher rates of expansion to go dead flat in July. Manufacturing producer prices are flat. Ex-energy the manufacturing PPI is up by 0.1%. Indeed, over three months, the PPI is falling and manufacturing prices are ticking lower. But manufacturing ex-energy prices are moving higher and actually accelerating from the 12-month pace to the six-month to the three-month. They are the lone ray of hope for higher inflation.

The German PPI has reversed its course to higher rates of expansion to go dead flat in July. Manufacturing producer prices are flat. Ex-energy the manufacturing PPI is up by 0.1%. Indeed, over three months, the PPI is falling and manufacturing prices are ticking lower. But manufacturing ex-energy prices are moving higher and actually accelerating from the 12-month pace to the six-month to the three-month. They are the lone ray of hope for higher inflation.

Of course, consumer prices are watched by the European Central Bank for the EMU region as a whole. The German CPI shows German inflation is sliding back to weakness. The CPI is at 0.4% over three months, a lesser gain than over six months and hardly stronger than the 0.3% 12-month pace.

Like the Fed in the U.S., the ECB has been trying to get inflation going. Both the Fed and the ECB have inflation objectives and for both the key number is about 2%. Year-over-year inflation in the EMU is even weaker than it is in the U.S. The German CPI is up by just 0.3% over 12 months and this is from the strongest most `over-heating' EMU economy. Obviously, inflation is going to take some time to develop in the EMU.

The German PPI does not offer a view of inflation headed back to normal. And to retell this old story by now, the global economy is still weak. Global oil prices are falling. Global commodity prices are falling. China is weak, depreciating its currency; that is causing a number of its competitors to depreciate along with it step-by-step. All of this means that Asia is trying to get an even bigger share of the domestic demand in other countries while not taking steps to provide more itself. China's currency drop trick is in train precisely because China has given up on trying to provide enough domestic demand through stepped up domestic schemes at home. It dropped the yuan and is trying to open the flood gates for its exports, except global demand is still too weak for that to work.

Germany is just one of the countries caught in this policy madness. Of course, the euro has been falling vs. the dollar for some time because of the poor economic conditions in Europe. The perception that the Fed would raise rates long before the ECB also fueled that currency move. But yesterday the Fed seemed a bit less gung-ho on the rate hike front. If the Fed pays attention to its own guidelines for hiking rates, it is not going to be doing it soon, despite what it says. All this has thrown markets into another tizzy.

Greece got a tranche of money under the new European scheme and has been able to repay the ECB. The EMU's lending to Greece gives the term `recycling' a whole new meaning. Of course, the Germans had to approve money for Greece. It has nothing to do with what was right or who deserved. It had to do with getting the ECB paid. So Europe's charade surrounding Greece goes on.

Is it surprising to anyone that inflation can't take hold in this environment? There is simply not enough demand and too much austerity. Asia has taken too much of the world's growth and has responded by keeping its savings rate low and damping the global growth multiplier. That has interacted with globally weak population growth and population aging. Meanwhile, technology has added in labor-labor saving inventions in this environment that needed no such cherry on top. So growth remains weak and inflation can't get a hand-hold, foot-hold or even toe-hold. Get used to it. If inflation can't find traction in Germany, it won't find it anyplace else.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief