Global| Aug 19 2016

Global| Aug 19 2016German PPI Posts Third Consecutive Monthly Rise

Summary

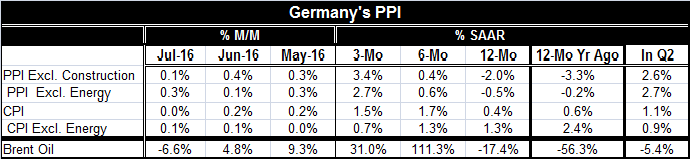

Trends The German PPI index rose for the third month in a row, sending the three-month rate of change into a strong upward trajectory as oil producers once again ponder supply restrictions to boost prices. In the table below, we [...]

Trends

Trends

The German PPI index rose for the third month in a row, sending the three-month rate of change into a strong upward trajectory as oil producers once again ponder supply restrictions to boost prices. In the table below, we chronicle the PPI and ex-energy PPI, the German CPI and ex-energy CPI plus Brent crude prices. There you see that Brent crude prices fell in July as the PPI and its core pushed higher on the month. The PPI's 3.4% compounded gain has the three-month pace accelerating strongly while prices barely edge higher over six months and are still lower on balance year-over-year.

Not off to the races

Inflation is not yet off to the races and Brent prices should yet pull the PPI gains back to earth. Oil is still in excess supply and it's anybody's guess when the Saudis will shift strategies and think that they can regain control of prices. Certainly some marginal suppliers have been driven out of the market, but as oil approaches $50/bl the prospect of further prices increases beckons to some of the shuttered oil producers to unpack and produce again. Output restriction has a dark side for producers too. The `free rider' problem has continued to dog the Saudis especially because they are loath to let their own output sacrifice benefit their arch-enemy, Iran, as it would.

PPI vs. CPI

Both the German PPI and the ex-energy PPI are showing sharp profiles of pressure as of July. PPI prices in Q3 (early in Q3) are up at about a 2.5% annual rate. CPI prices lag the PPI, however, in terms of three-month pressures and the CPI (HICP) is the standard for the inflation-targeting scheme of the ECB.

CPI trends remain muted

CPI trends remain muted

The German CPI does not even show price acceleration in gear as its headline rate and ex-energy rate are both slowing over three months compared to six months. In the third quarter-to-date, the headline and ex-energy CPI each are rising in the neighborhood of a 1% annualized pace. Brent prices are falling at a 5.4% annualized pace in the third quarter-to-date.

The longer view is still tranquil

The second chart is the PPI and CPI ex-energy view of inflation on a year-over-year basis. Here the PPI year-over-year trend is still lower and only hints at its coming upward reversal. Year-on-year ex-energy PPI prices continue to fall as they have nearly universally since mid-2013. The CPI ex-energy trend shows little variation at all. This is a very tranquil view of the policy setting path of the German CPI. The chart also highlights the extent to which PPI prices are so much more volatile than CPI prices. PPI prices will turn up much more virulently and time will pass before these gains are reflected in consumer prices. Consumer prices give energy a much lower weight.

PPI spurt: signal or false alarm?

It is not perfectly clear that the PPI is putting us on notice for a change in the path of inflation. Despite the pressurized three-month PPI gain, the key ingredients have not yet clearly come together to put inflation on an accelerating path for good. For one, oil prices are not yet decisively on a firm level or on an upward path. It is unclear whether oil producers are prepared to take the steps to achieve that -and in the process to give over gains to those who are not participants in an output restricting deal (like Iran and the U.S. oil industry). The weak global demand background with weak growth in Europe, Asia, and developing economies is not yet solid enough to be a sure base that can underpin prices and driven them higher. Conditions in Asia seem to be particularly touch and go in terms of growth. Japan has no inflation momentum at all. Even in the better-performing U.S. economy, inflation has flared then has backtracked. Not all sparks light fires.

The fly on the oil-slick

The PPI may be the canary in the coal mine for inflation signaling. But sometimes there are false signals and sometimes signals will ebb and flow. We see this as an ebb and flow moment. We do not see inflation clearly mounting from here on out. The turn in oil prices has accentuated the PPI rebound. And we do not yet know if oil prices are done turning or not. Clearly the oil price trend is one important event that will help sort out where inflation is going and that remains up in the air.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief