Global| May 19 2017

Global| May 19 2017German PPI Continues to Gain

Summary

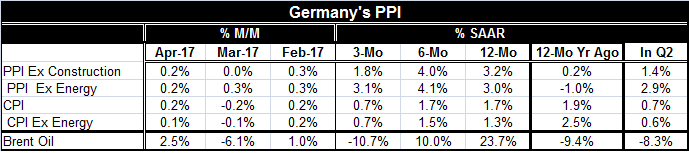

The German PPI excluding construction (hereafter just PPI or headline PPI) rose by 0.2% in April, the same rate as the PPI excluding energy. But the three-month pace of the PPI gain and the core gain each slowed from their respective [...]

The German PPI excluding construction (hereafter just PPI or headline PPI) rose by 0.2% in April, the same rate as the PPI excluding energy. But the three-month pace of the PPI gain and the core gain each slowed from their respective six-month pace. The headline pace over three months is below the 12-month pace. The ex-energy three-month pace is just a tick stronger than the 12-month pace. Much (most and maybe even all) of the PPI gain is attributable to rising oil prices. Brent is up by 23.7% over 12 months but falling at a 10.7% pace over three months and rising at a 10% pace over six months. In broad terms, as oil goes so goes the PPI.

Of course, we are always concerned about inflation. But for policy, we are most concerned about the CPI (or HIPC specifically in the EMU and, of course, it is the EMU index that matters for policy). Two charts above document that the PPI price pressures already are rolling over as the peak impact of the oil price bulge appears to have played out (at least for now). The chart on the right shows how the PPI has swung widely in recent years without much impact on the German consumer prices. The point is that throughout the EMU, PPI prices are harder hit, but that does not always result in a stronger CPI (HICP).

Interestingly though, if we map the R-squared impact from oil prices to the German PPI and to the German CPI separately, the correlation to the CPI produces an R-squared of 0.43. The correlation to the PPI produces a lower R-Square of 0.27. So there is overall a more predictable relationship of oil to the consumer prices; yet, the impact of oil prices on the PPI, which is less consistent, produces much more variation in the headline PPI (see the Brent and PPI price level chart). The CPI has less variation overall, but proportionally more of it is explained by oil.

Interestingly though, if we map the R-squared impact from oil prices to the German PPI and to the German CPI separately, the correlation to the CPI produces an R-squared of 0.43. The correlation to the PPI produces a lower R-Square of 0.27. So there is overall a more predictable relationship of oil to the consumer prices; yet, the impact of oil prices on the PPI, which is less consistent, produces much more variation in the headline PPI (see the Brent and PPI price level chart). The CPI has less variation overall, but proportionally more of it is explained by oil.

The price level plot of Brent vs. the PPI shows the clear tendency of Brent to move ahead of the PPI and reveals the clear sense we get that the PPI dances to the tune of oil.

Of course, this also means that's what's next for the PPI and to a lesser extent the CPI also depends on what's next for oil. The latest oil market 'spin' from the IEA is that OPEC's extending the current quotas is not going to be enough to tighten up the oil market although until recently the Saudis have treated the just-agreed to quota extensions as the holy grail. So much for letting 'spin' be your policy guide.

It is clear that global growth has not been up to par and yet oil supply even at these price levels has been coming on stream with upside surprises. Canadian output is one place where there has been some surprising supply increases. Of course, if there is more quota-cutting to be done, this could place a strain on Saudi-Russian ties and the Saudis already were trying to keep from being critical of Russia's lagging participation in the quota program.

A few days ago Russia's claiming it was on board for the new quota extensions and on board to extend these quotas through Q1 2018 was taken as a strong commitment by Russia when it simply may have been the reality that fit best into the coming Russian election cycle. The admission now that mere quota extensions might not be enough puts everyone back at square one. Will the Russians be 'on board' for more cuts?

Oil will be the key in the short-run to what inflation does. If growth has a surprising pick up, OPEC could be bailed out of its policy dilemma. Short of that, the 'cartel and friends' will be more severely tested in the coming months.

For now the ECB's steady as she goes policy path seems not to be jeopardy. There is not much inflation push outside of oil, and for the purposes of policy, central bank head Mario Draghi has essentially redlined inflation created by oil alone. He is looking at core inflation, but with enough oil-based inflation at some point the core will probably respond to some extent as well. When that happens, the ECB will have to change its tune.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief