Global| Feb 06 2017

Global| Feb 06 2017German Orders Surge in December

Summary

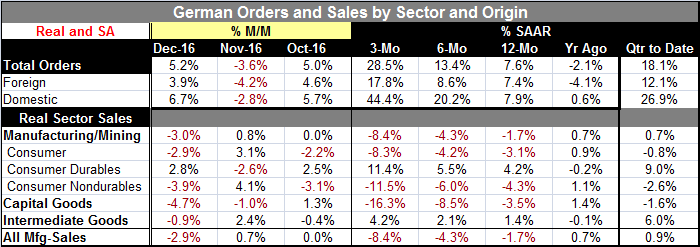

Germany's real order volume surged by 5.2% as German domestic orders spurted by 6.7% month-to-month and foreign orders rebounded to gain 3.9%. Orders have come to show huge changes in recent months as the 6.7% domestic gain in [...]

Germany's real order volume surged by 5.2% as German domestic orders spurted by 6.7% month-to-month and foreign orders rebounded to gain 3.9%. Orders have come to show huge changes in recent months as the 6.7% domestic gain in December compares to a 2.8% drop in November while the foreign order gain in December still falls short of the 4.2% foreign order drop in November. And October was a strong month for orders across the board.

Germany's real order volume surged by 5.2% as German domestic orders spurted by 6.7% month-to-month and foreign orders rebounded to gain 3.9%. Orders have come to show huge changes in recent months as the 6.7% domestic gain in December compares to a 2.8% drop in November while the foreign order gain in December still falls short of the 4.2% foreign order drop in November. And October was a strong month for orders across the board.

Foreign and domestic orders accelerate

Volatility and order expansion have picked up. Total orders are accelerating, growing at a 28.5% annualized pace over three months, a 13.4% annualized pace over six months, and at a 7.6% annualized pace over 12 months. Separately both foreign and domestic orders each are accelerating on that timeline as well with domestic orders the stronger series over six months and three months on an explosive three-month annualized pace of growth of 44.4%.

Manufacturing order strength is confined to Germany and other euro area members

The order bulge for Germany is either domestic or related to activities in the countries of fellow EMU members. Orders outside the euro area show no increase at all month-to-month while orders from countries inside the euro area saw manufacturing new orders rise by 10% in December alone. Year-over-year orders in the euro area are up by over 21% while orders from foreign countries outside the euro area are slightly lower over 12 months.

Other surveys show a pick up

Both the IFO and the Markit surveys have been showing some pick up in German activity but nothing as robust as this. The EMU region has been showing manufacturing progress as well. But these orders data are now quite strong (although since they tend to be volatile we should be careful in doling out final judgements).

Disconnect?

In fact, current activity, as represented by real sector sales in the same table, shows that sales are considerably weaker in real time compared to the prospective strength that orders imply. Sales are lower by 1.7% over 12 months and their growth rates are clearly decelerating. With orders up by 7.6% year-on-year, real sector sales still are lower by 1.7% year-on-year and their sequential trends are diverging as well.

Long-term trend compatibility

Since 2008, orders have explained about 80% of the variance in sales on a year-over-year basis, but they explain only 25% on a month-to-month basis. The divergence between month-to-month orders and sales is really not so unusual this month. But there is also a large divergence between the two series on a year-over-year basis and it is the ninth largest year-on-year divergence in the past 108 months - a divergence that has been greater less than 10% of the time. It is unclear why this divergence and the sequential trends are so different between sales and orders.

Is it volatility or acceleration?

The economic data have been jumping around to some extent. There are signs that activity is stirring. As it picks up, some irregularity is to be expected. When an economy changes gears, various sector metrics might divert from their long-term trends for a while before longer-run relationships are reestablished. There is some reason to be optimistic about the strength in German orders. And the lingering weakness in real sector sales may be just that: lingering weakness that is about to be expunged. But as always, it's good to keep an open mind and check on the data each month. However, it is reassuring to see a number of different surveys pointing to improved activity.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief